Interview

Editor’s note: The Q & A below is an interview conducted by Fintrust Director of Marketing and Client Engagement Paige Siniard, with Allen Gillespie, CFA®, President, Managing Partner Investments.

July 2020

Q3 2020: Temporal Markers & Masks

Q: Allen, for the last two quarters you have been talking about toilet paper markets, the virus, war, and hyperinflation. Where do we stand now?

While I was on my walk last night, it dawned on me how much has happened in the first half of 2020. Yet, at the same time, for me at least, time feels a little suspended. I think this is because none of us are sure what the long-term changes to our lives might be from the Covid-19 virus. Do we return to old routines or will there be entirely new patterns? As a result, I think the virus, war, hyperinflation, and masks are creating a societal temporal marker.

Q: What is a temporal marker?

Temporal markers, mark time, through association with key events in our lives. Think of a temporal marker like this—where were you when X happened, or your life before X and your life after X.

Temporal markers occur in our individual lives, but they can also occur at a societal level. There are various categories of temporal markers like historical or cultural, but these frequently relate to one another.

Q: Can you give us examples of individual temporal markers?

Sure. A simple example might be the difference between your life before children, and your life after children. Another would be your life when you lived in city X and your life when you lived in city Y, particularly if you also changed careers at the time.

Q: I get that, then what are societal temporal markers?

Societal temporal markers, on the other hand, mark events that everyone can remember and use as a time reference. The biggest societal temporal markets, however, are not just collectively “remembered”, they are collectively “experienced.”

In the first category of societal temporal markers, we have events like 9/11 and the Vietnam War. These events are collectively remembered, but they were not necessarily collectively experienced. People of the Vietnam generation know their draft number and whether or not it was called—collectively remembered not collectively experienced.

EXECUTIVE SUMMARY

FinTrust Investment Review Team:

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis, CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

- Monetary Policy: Accommodative. The Federal Reserve has massively expanded its balance sheet and has started buying corporate bonds and ETFs directly.

- Fiscal Policy: Accommodative, but about to stall. Many of the Covid-19 stimulus measures end at the end of July. Fiscal policy then is likely to be in a holding pattern until after the Presidential election.

- Temporal Markers mark a change in the speculative mood.

- Yield Curve Watch: The yield curve has regained its slope flowing the $2 Trillion Stimulus Bill, and is now pointing toward a weak economic recovery. Corporate credit curves still indicate high levels of financial stress.

Similarly, the terror attack of 9/11 and War on Terror are collectively remembered, but they have not been collectively experienced. I was living in New York in 2001, so I vividly remember the day. I also remember, however, how 9/11 altered life and moods for people in the city. After 9/11, when we first began to return to the bars and restaurants, it felt wrong to be there. In contrast, if you did not live in New York, your life returned to normal relatively quickly. As a result, the event did not linger in the collective consciousness as long.

More important than my experience with 9/11, was our government’s response: launching the “War on Terror.” The “War on Terror” has had a very large impact on military spending and military families over the last 19 years. The “War on Terror, which as we sit here in 2020 has been never ending, has taken a heavy mental toll on our military.

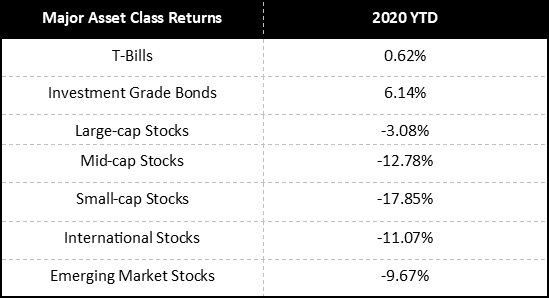

Source: Morningstar Direct, As of 06/30/2020

This sadly shows up in the suicide statistics for our soldiers with PTSD. As a result, 9/11 and the “War on Terror” have had a very long tails, but their impact has not being collectively shared. The 9/11 terror attack and response, therefore, is a societal temporal marker, but one with more individualized impacts — both experienced and remembered.

This brings me back to the simple economic point we discussed in our last Wealth Management Quarterly. The Trump Administration has openly asked these questions: “If over the last 19 years, we had spent $6 Trillion at home, rather than in the War on Terror, how different would our world look?” and “if we hadn’t financed that spending through the issuance of bonds largely held by overseas investors, where the interest was used to build competing factories—how different would our country be?” Since the War on Covid-19 started in March, we have already spent nearly $4 trillion on stimulus, so I think we are about to find out the answer to that question.

Q: Is it possible to have temporal markers that are collectively shared?

Yes. The largest societal temporal markers are those that are both “felt” and “shared.” Think of historical events like World War II. Economic data series are frequently broken around these types of societal temporal markers. For example, in the US we have pre/post World War II datasets. The pre-WWII period was more agricultural, so we had periods of both inflation and deflation. Since World War II and mass industrialization, we have had consistent and persistent inflation, so the nature of the data series changed. In Germany, economic statistics are broken into the pre and post hyperinflationary periods. In fact, there are few good records of the hyperinflationary period, because things were changing so rapidly.

Q: You mentioned cultural temporal markers earlier. Can you give us example of that concept?

Cultural temporal markers, are frequently marked by the ascension or death of something—a cultural figure or trend that defines the era. Our western calendar, for example, divides time into time being either B.C.E or A.D. Other examples would be the Kennedy assassination, the death of disco, and the launch of MTV. When disco died, 50,000 people showed up at a Chicago White Sox games to smash their disco records. MTV launched with “Video Killed the Radio Star” at 12:01am on Aug. 1, 1981. Steve Jobs and Apple smashed Big Blue in a 1984 Super Bowl Commercial.

Q: How do temporal markers relate to markets?

Temporal markers generally mark a change in the speculative mood or direction of the markets. An interesting temporal marker that one Wall Street writer pointed out at the time, was that during the Internet Bubble runup of 1999 and early 2000, the number one show on tv was Who Wants to Be A Millionaire.

Just after the peak of the bubble, however, Who Wants to Be A Millionaire was knocked from the top spot by Survivor. Subconsciously, people were moving from greed to fear and survival. 9/11 marked the low for that bear market, and it ended a 12 year decline in defense spending that had started after the fall of the Berlin Wall.

Q: Anything interesting in the top shows now?

Yes, actually. According to Variety, the top spot belongs to Sunday Night Football, but if you kick that out because we are not currently playing sports, well the top spot goes to The Masked Singer. I have never watched that show. I just find the “mask” reference interesting and revealing as to where we are culturally.

Q: Does this change in pop culture mean anything for markets and investors?

After watching Who Wants to be a Millionaire yield to Survivor as the technology bubble of the early 2000s popped, I find cultural parallels to the markets interesting. Since The Masked Singer has dethroned, the now non-existent, Sunday Night Football, I think it signals that we are in a highly volatile, harsh investing environment.

Q: How do you draw that conclusion?

When I lived in New York, I covered the gaming sector. I can assure you that sports betting, or “punting” as the British like to call it, is a huge business. Punters like action, and they have high risk tolerances. They’re going double or nothing on the next roll or game.

In March, casinos closed, and sports stopped. Then, stimulus checks were issued. As a result, a lot of millennial punters started playing the stock market which was still open. This can easily be seen in the data from Robinhood, the investing platformed favored by millennials.

Source: Bloomberg as of 06/30/20

To a gambler, volatility and movement would be positives, not negatives. This mindset contrasts sharply with the typical investor’s. Investors do not enjoy high volatility. In sports gambling, the games are relatively short – a pro football game last about 3 1/2 hours. In that regard, punters are more interested in short-term moves than long-term business fundamentals.

Viewers could also just be looking to replace the excitement of live sports. A quick google search will yield a multitude of “The Masked Singer” betting options. You can place a bet on anything from the celebrity identities to the winners and losers each week. In many ways, a competition show like “The Masked Singer” or the stock market is an obvious choice to sate our nation’s sports habit. I also can’t help but become fixated on the correlation between watching masked competitors, while many of us are donning masks for the first time in our everyday lives.

Masks are typically worn as protection in harsh settings like hospitals, deserts, mines, and that type of thing. So, the harsh investing environment and shutdown of sports is encouraging speculation in stocks that “move.”

Q: If you think we are a harsh, war like environment, why are markets bouncing back so strongly?

Fear, money and now greed. Initially, when war breaks out there is fear. Governments always respond to the outbreak of war with the printing of money. The increase in money then leads to increased profiteering. The old Wall Street maxim handed down from the Rothchilds was to “buy when there is blood in the streets.” It’s a callous saying but it generally works on Wall Street. In that regard, the punters are today’s war profiteers.

Q: You said fear, money, and greed. Are we already at the greed stage?

Yes, I think we are. We may still be early in that stage, but there is no question that I am seeing things in the market that I haven’t seen since 1999.

Q: Can you expand on that?

Back then, the “Asian Financial Crisis” of 1998 cut global growth, oil prices crashed, and governments printed money because they were worried about the Y2K computer virus crashing markets. Today, we have Covid-19 shutdowns, oil prices crashed to a negative $38, and investors are concerned about a real virus crashing the economy. Back then the House impeached Clinton, in January the House impeached Trump. Back then, there was a mad rush to get on the internet, so everyone signed up for AOL—today, we are all jumping on Zoom calls, despite the fact that we have had Facetime and Skype on our phones for years.

Back then, the bars in New York found customers wanted to watch CNBC at happy hour instead of Yankees games because people didn’t have cellphones to check their portfolios. In 1999, people were excited about the internet and the mapping of the human genome, so genomics stocks and internet stocks were speculative favorites. Today, cloud computing stocks and virus related biotechnology stocks are the speculative favorites.

Back then, people started day trading through TD Ameritrade and Schwab. Today, millennial Robinhood traders are moving 50 times the volume of Schwab and TD Ameritrade customers.

I could go on, but you get the idea.

Q: Any final thoughts for our clients and investors?

This fourth of July, I reread the Declaration of Independence. We all probably remember some of the lines from our elementary school days, but rarely do we recall the list of complaints against the King. It makes for interesting reading because many of the issues with which the colonist were struggling are the same issues we are struggling with today—I think if we the people wrote a list of complaints today it would run against both of our current political parties. Let me give you a sample.

“He has endeavoured to prevent the population of these States; for that purpose obstructing the Laws for Naturalization of Foreigners; refusing to pass others to encourage their migrations hither”

“For cutting off our Trade with all parts of the world.”

“For imposing Taxes on us without our Consent.”

“He has plundered our seas, ravaged our Coasts, burnt our towns, and destroyed the lives of our people.”

“He has excited domestic insurrections amongst us, and has endeavoured to bring on the inhabitants of our frontiers,…, whose known rule of warfare, is an undistinguished destruction of all ages, sexes and conditions. “

The hopeful takeaway from rereading the Declaration of Independence is that while times seem a little wild, and volatility is high, our political system is specially made to deal with these issues.

In fact, when we looked through the various stimulus packages, there was a lot of good bi-partisan stuff in the CARES Act like more money for 5G. This will support remote learning, telehealth, automated cars, and the buildout of the future infrastructure the country will need to compete with China’s Made in China 2025 plan.

QUICK TAKE: MAJOR ASSET CLASSES

Cash and Cash Equivalents

Cash rates now sit near zero, and futures markets are projecting that we will see negative interest rates in the Unites States by September. As a result, we believe alternative currencies like, gold, and cryptocurrency offer positive carry against cash.

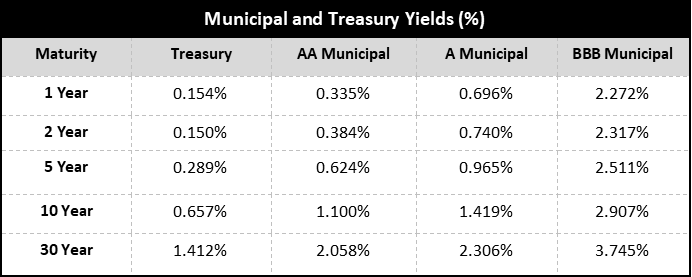

Investment Grade Fixed Income

Investment grade credit spreads widened materially during the 1st quarter, but narrowed to more normal recessionary levels after the Federal Reserve began buying corporate bonds and bond exchange traded funds. While attractive on a spread basis, the low level of interest rates, generally makes investment grade bonds a challenging asset class. We think investment grade bonds still have a defensive roll to play, but we would not expect capital appreciation from bonds going forward.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given the stresses in credit, we continue to favor arbitrage related strategies, as we do not yet believe high yield credit fully reflects the economic challenges ahead.

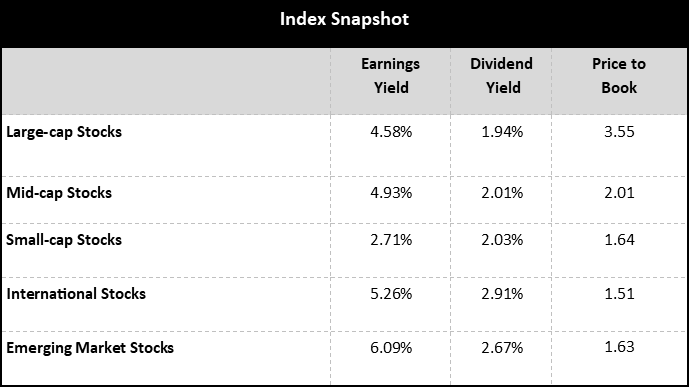

Core Equities

Since our last report, equity prices have appreciated materially. As a result, we believe equities are slightly overvalued relative to historical valuations. As a result, we are modestly constructive on equities, but we believe individual security selection rather than asset allocation will be increasingly important going forward. Given the high levels of volatility, we would not overweight equities beyond investor risk determined allocations.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward trade-offs. Tactical equity strategies, like long/short equity, option based strategies and market neutral strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low interest rates and the likely structural changes to the economy.

Source: Bloomberg as of 06/30/20

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. We are concerned that recent events will accelerate trends towards online purchasing and remote work, which will increasingly pressure certain real estate sectors. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

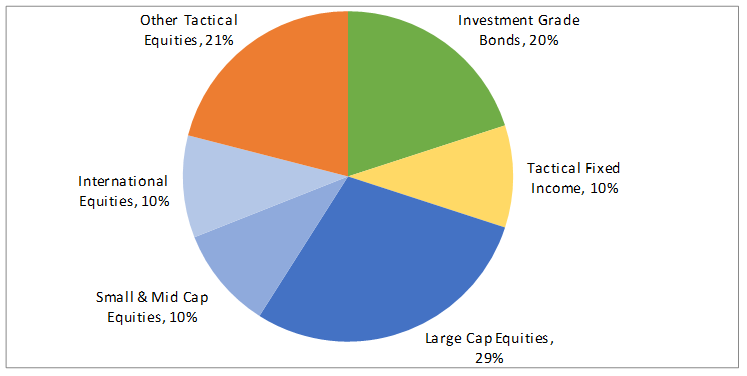

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 6/30/2020. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research