Interview

Editor’s note: The Q & A below is an interview conducted by Fintrust Director of Marketing and Client Engagement Paige Siniard, with Allen Gillespie, CFA®, President, Managing Partner Investments.

November 2020

Q4 2020: The Curse of Tippecanoe

Q: Allen, last quarter you discussed temporal markers, what are you thinking about now?

The Curse of Tippecanoe. I started thinking about it during the Vice-Presidential debate, given the ages of Trump and Biden.

Q: Tell me about this curse.

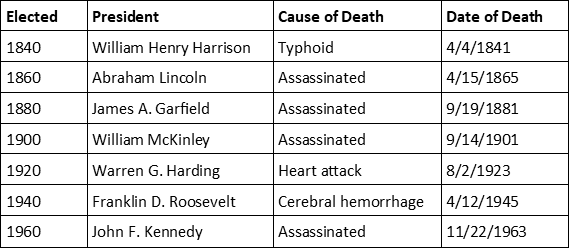

Prior to Reagan, every president elected in a year ending in zero since William Henry Harrison had died in office. President Reagan was elected in 1980, and after he took office in 1981 he was shot by John Hinckley. Reagan survived, so he became the first president elected in a year ending in a zero, in seven generations, to survive the curse.

The story goes like this. Before he became President, Harrison had been Governor of the frontier Indiana Territories. In this role, on November 7, 1811 Harrison led forces into battle against the Shawnee leader Tecumseh at Tippecanoe. In defeat, Tecumseh supposedly cursed Harrison and the United States’ leaders for supporting Western Expansion. Harrison’s fame helped him win the presidency, but it was a short one. After an inauguration held outside in the winter elements, Harrison got sick and died a month later from illness. He thereby holds the record for the shortest presidency—one month. Here is the full list.

Q: Beyond Presidential succession, are there other reasons the Curse of Tippecanoe is on your mind?

Absolutely. First, the Curse of Tippecanoe reminds us that this is not the first time our country has faced political uncertainty. That 1811 battle at Tippecanoe leads the country directly into the War of 1812— which has been called America’s Second War of Independence. The War of 1812, in turn, casts an extremely long tail over American political history, which lasts even to this day.

EXECUTIVE SUMMARY

FinTrust Investment Review Team:

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis, CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

- Monetary Policy: Accommodative. The Federal Reserve has massively expanded its balance sheet and has started buying corporate bonds and ETFs directly.

- Fiscal Policy: Accommodative, but the next stimulus bill and infrastructure bills are currently stalled in Congress. Many of the Covid-19 stimulus measures ended at the end of July. Fiscal policy then is likely to be in a holding pattern until after the Presidential election.

- The Curse of Tippecanoe: is the story about Presidential succession for reasons other than an election.

- Yield Curve Watch: The yield curve has regained its slope flowing the $2 Trillion Stimulus Bill, and is now pointing toward a weak economic recovery. Corporate credit curves still indicate high levels of financial stress.

Q: Can you give examples of that long tail?

This is more of a political than economic example, but Francis Scott Key penned his poem “The Defence of Fort M’Henry” after watching the British bombard the Maryland fort during the war. People later set his poem to music and adopted it as the national anthem in 1931. Today, we know his poem as the words to the Star-Spangled Banner.

The war also made the Tecumseh name famous. We all know General Sherman, but the origin of his full name is less common knowledge. William Tecumseh Sherman was named after the Shawnee Confederacy leader. After the Civil War, Sherman becomes commander of the Missouri district and later general commander of the United States Army. In these roles, Sherman directs US policy toward the Plains Indians and commands that any Indian not on a Reservation be considered hostile. Sherman tolerates and encourages economic warfare to force the relocation, through the systematic destruction of the Plains Indian’s buffalo food source. Thus, if you ever visit out West you should think about the War of 1812 and Tecumseh.

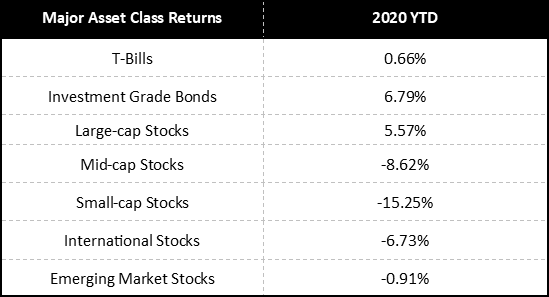

Source: Morningstar Direct, As of 09/30/2020

Q: Are there any economic lessons from the War of 1812?

I think the big lesson for investors to learn from the war is that even the bleakest political and economic cycles do turn. The War of 1812 reminds us that foreign interference in domestic affairs is not new. This election cycle, we have heard a lot about the foreign intelligence efforts of Russia and China, particularly regarding social media and cyberspace. Cybersecurity and social media, much like the West of 1811, are the new frontiers of our society, so they naturally become battlefields.

In 1811, US citizens were concerned about their actual security because the British were arming various frontier tribes, including the Shawnee Confederacy. Then things went from bad to worse. During the War of 1812, the British themselves burned Washington, bombarded Baltimore, and attacked New Orleans. Can you imagine investing in America then?

Q: Wasn’t the Battle of New Orleans fought after the war had ended?

Yes, and I think that is another great lesson for investors to consider this election cycle. News did not travel particularly quickly in the early 1800s. As a result, the Battle of New Orleans was fought from Jan. 8, 1815 to Jan. 26, 1815 even though the Treaty of Ghent had been signed on December 24, 1814. Similarly, this year, we may continue to see fighting long after election day, but financial markets will be looking ahead.

Q: If markets are looking ahead, what do you think they will see?

Following the War of 1812, the economic recovery and Western Expansion created a period we now call the Era of Good Feeling. Following this year’s massive stimulus and political controversy, I think markets would like to discount such an Era of Good Feeling now. While I do think a strong recovery and expansion are coming, I think we also need to be realistic regarding time horizons, given the economic impacts of the Covid-19 shutdowns. It took five years to get from the Battle of Tippecanoe to the Era of Good Feeling. A three to five year recovery from this year’s shutdown seems about right considering the economic estimates and demographic curves we have studied.

Q: What else do you think markets see as they look ahead?

Opportunity. I keep thinking of The War of 1812 because it truly forges the American identity. It places into the collective American mind the idea of Western Expansion. The Western frontier today would include frontier growth industries like cloud computing, electric cars, space travel, cybersecurity, green energy, artificial intelligence, internet retail, esports, and 5G to name a few.

Q: All that sounds great, but are there any downsides to all this growth?

Yes, unfortunately, growth also causes economic displacements. Just as the Western Expansion of our nation enabled it to grow, it also set the United States on a course of increasing conflict with the Native American populations. The Western Expansion also raised the issue as to whether new states would be slave states or free states. These issues manifested more fully decades later in the Civil War and settlement of the West in the mid to late 1800s. I think Langston Hughes’s 1935 Depression Era poem “Let America be America Again” beautifully captures the tension of America’s history after 1812.

Like the Western Expansion before, today’s industries, companies, and government policies create economic disparity and displacements for people. Prior to Covid-19, the shift of manufacturing to China displaced many industrial jobs from American cities. Covid-19 further exacerbated many of the economic disparity issues we face, as the government chose to shut various “nonessential” businesses, while allowing others to stay open. These types of policies have led to massive shifts in economic well-being. The disruption resulting from these policies has created a war like atmosphere.

Q: What are the economic policies that might ease these dislocations?

In a well-functioning economy, mobility, education, and financing policies all play critical roles in addressing the economic stresses created by growth. Despite the political noise, I do think Covid-19 forced our politicians to work better on a bipartisan basis on certain legislation. I think the bipartisan Cares Act was a strong bill. The Cares Act contains a tremendous amount of money for rural and urban broadband expansion and telemedicine.

Q: That is a surprising statement. Can you expand on that?

Economic mobility is key, as it enables people to find new opportunities. Candidly, I think the extra unemployment benefits have given people the capital they need to move forward more quickly, rather than wait around for old jobs to come back. Statistically, we are seeing hundreds of thousands of people move out of the major metropolitan areas like New York and San Francisco. I just read an article that stated there have been over 200,000 permanent address record changes away from New York alone since the Covid-19 shutdowns. In that sense, the lasting impact of Covid-19 might be a better distribution of economic gains going forward.

Q: What about in education?

Education also plays a critical role in easing economic transitions, as it enables people to learn the new necessary skills demanded by the growth industries. Remote learning may not be ideal for younger students, but it can work well for younger adults.

We are hearing antidotal evidence of college kids telling their parents that they can learn more at home than at college. If true, remote learning might free up tremendous economic resources and encourage younger people to try their hands at entrepreneurship with those savings. Remote education also empowers some who otherwise may not be able to participate in the new economy.

Q: What are you seeing in money and banking?

On the financing side, I really thought the Small Business Administration’s payroll protection program (PPP) was smartly done. This SBA program equaled about 10 years of normal SBA lending, so it was a massive effort. I think the program establishes a model that will likely be used going forward to support small business for the following reasons.

- Small businesses which grow are the primary job creators in our economy. Yet, small businesses are very tough for traditional banks to underwrite. Banks struggle with small business because there are limited “secondary sources of repayment” in short, small businesses frequently lack collateral.

- In uncertain economic times, banks don’t do much lending to small business. During recessions, small businesses default at roughly a 9% rate. For a bank leveraged 10 to 1, this type of default rate puts them out of business.

The PPP loan program solved these issues. First, the federal government took the credit risk, so every small business received the same interest rate (4%) regardless of their credit worthiness. While a 9% default rate is a disaster for a bank, in the aggregate, at a 4% rate, the federal government will earn its money back in just over 2 years. In short, the federal government really did solve a problem the private sector could not solve given its structure.

Going forward, it would not surprise me to see the SBA programs become as critical to our economy as the mortgage programs run by the federal government.

Q: Any final thoughts for our investors?

While the United States won the War of 1812, it was a financial catastrophe for the country. At the time, the country financed itself through various taxes on trade. The war caused an interruption of commerce, and trade taxes fell by over 50%. Financial practices of the early 1800s required that borrowing be repaid in gold or silver. The US could not do this, and as a result US dollars fell in value relative to gold and silver. The US essentially defaulted on its obligations to pay off the debt in 1814. In total the country borrowed $127 million to finance the war, and it took until 1837 to pay off the debt.

There is an old saying on Wall Street—don’t fight the Fed. Historically, this meant don’t sell stocks when the Federal Reserve prints money. Covid-19 once again has proven that this is sage trading advice. At the same time, however, people seem to be ignoring the inflationary impulses of our monetary and fiscal policies due to the Covid-19 slowdown, particularly regarding their bond holdings. We suspect the country will be paying the bill for a long time. Finally, we also suspect the value of the money with which bondholders are repaid down the road might not be equal to the value of the money they invested.

QUICK TAKE: MAJOR ASSET CLASSES

Cash and Cash Equivalents

Cash rates now sit near zero, and future’s markets are projecting negative short-term interest rates in the Unites States. As a result, we believe alternative currencies like gold and cryptocurrency offer positive carry against cash.

Investment Grade Fixed Income

Investment grade credit spreads widened materially during the 1st quarter, but then they narrowed to more normal recessionary levels after the Federal Reserve began buying corporate bonds and bond exchange traded funds. While attractive on a spread basis, the low level of interest rates, generally makes investment grade bonds a challenging asset class. We think investment grade bonds still have a defensive roll to play, but we would not expect capital appreciation from bonds going forward.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given the stresses in credit, we continue to favor equity arbitrage related strategies, like market neutral equities, as we do not yet believe high yield credit fully reflects the economic challenges ahead.

Core Equities

Since our last report, equity prices have appreciated materially while earnings have declined. As a result, even after adjusting for recessionary recovery, we believe equities are slightly overvalued relative to historical valuations. As a result, we are modestly constructive on equities, but we believe individual security selection rather than asset allocation will be increasingly important going forward. Given the high levels of volatility, we would not overweight equities beyond investor risk determined allocations.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low interest rates and the likely structural changes to the economy.

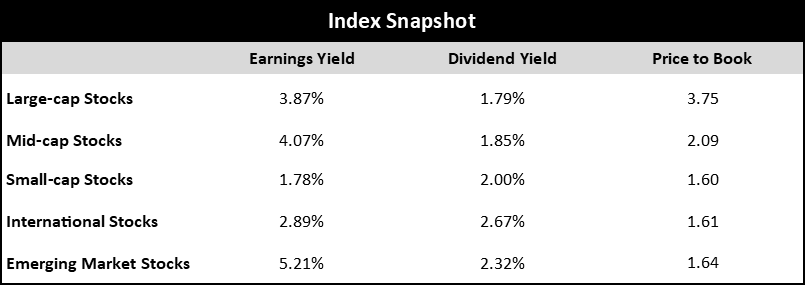

Source: Bloomberg as of 09/30/20

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. We are concerned that recent events will accelerate trends towards online purchasing and remote work, which will increasingly pressure certain real estate sectors. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

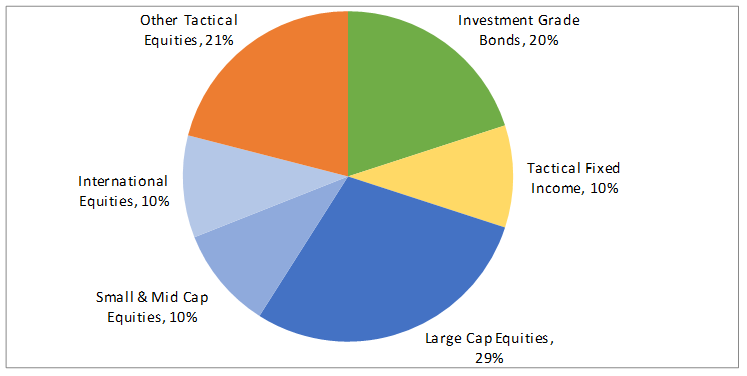

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 6/30/2020. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research