A New Dutch East India Company or Bernanke’s Mississippi Bubble Stock? Part III

FinTrust Brokerage Services Equity Research

July 30, 2019

*Please see important certification and disclosure information at the bottom of this page.

Industry: Wholesale Distribution

GICS Sector/ Sub code: Electrical Apparatus and Equipment / 5063

Company Summary: Founded in 1994, Amazon.com opened its virtual doors on the World Wide Web in July 1995. Fortunately for earthlings, Amazon seeks to be “Earth’s most customer-centric company (Source AMZN 10-k),” however, this leaves the rest of the universe open to competition and non-earthlings subject to non-customer-centric predators. Amazon.com clearly faces competition in the “Middle Kingdom” of China from Alibaba, and we sincerely look forward to the space race between Jeff Bezos’s Blue Origin, Richard Branson’s Virgin Galactic, Elon Musk’s SpaceX, and Paul Allen’s Vulcan Aerospace. We believe it will capture the public’s attention in the 21st century in a manner similar to the early automobile and airplane industry races of the early 20th century. In addition to its investments in drone technology, Amazon.com operates across five segments: consumers, sellers, developers, enterprises, and content creators and provides advertising services and co-branded credit cards. Conventionally, or terrestrially, the company can be said to operate across retail, logistics, consumer technology, cloud computing, media and entertainment, and increasingly, artificial intelligence.

Analyst Notes:

Analysis by Allen Gillespie, CFA®, (917) 679-6335 and (864) 288-2849

- We are issuing this special report due to the following factors: 1) The continued moral bankruptcy of Central Bankers around the globe. 2) The fact that we continue to receive questions regarding AMZN’s stock price and our divergent recommendations. 3) Our continuing need to educate investors regarding the importance of our Bitcoin Gold Dow Theory in this age of Monetary Disorder 4) Natural adjustments to price and valuation targets in light Amazon’s operations and Central Banker largesse since our last report.

- In order to properly understand our recommendation, one must understand our Bitcoin Gold Dow Theory analysis framework, which is an effort to understand the differences between nominal and real prices in the modern economy. This framework holds that the modern analyst should measure prices in relation to gold for tangible assets and measure the market value of intangibles in relation to bitcoin to derive real prices and real estimates of economic activity and values.

- Under our Bitcoin Gold Dow Theory analysis framework, there are three ways overvalued stock prices can return to fair value. 1) Share prices can fall 2) Share prices can remain the same while the companies increase their underlying value (value and price converge in the future) 3) The value of money falls (this could result in an increase in nominal share prices but a decline in the real purchasing power of the shares).

- Since the time of our previous report, the price of money (as measure by gold and BTC) has declined and Amazon has increased its underlying value. Since our Sept 4, 2018 Sell recommendation, AMZN’s share price has declined 4.98% in nominal prices and declined 27.99% relative to BTC and declined 19.83% relative to gold.

- Since the time of our initial July 24, 2017 Sell recommendation, AMZN’s share price has risen 86.46%, while BTC has risen 241.88% and Gold has risen 12.76%. Thus, in real prices as measured by BTC, AMZN’s share price has declined by 45.46% since our initial Sell recommendation while our USD price recommendation has been incorrect. Using GLD against AMZN’s tangible book value and BTC against the difference between AMZN’s market value and book value, AMZN’s share price has fallen 39.9% close to our original estimate of a 37% overvaluation..

Fintrust Recommendation

Fintrust Rating: HOLD

Target Price: $1,611.27

Current Share Price $1,912.45

Expected Return -15.7%

52 Week Price Range $1,307 – $2,050.50

Fintrust Brokerage Services, LLC rates companies a BUY, HOLD, SELL, or SHORT.

- A BUY rating is given when the security is expected to outperform the broad equity market as measured by the S&P 500 on a risk adjusted basis over the next year.

- A HOLD rating is given when the security is expected to perform in line with the broad equity market as measured by the S&P 500 on a risk adjusted basis over the next year.

- A SELL rating is given when the security is expected to perform below the broad equity market as measured by the S&P 500 on a risk adjusted basis over the next year.

- A SELL SHORT is given when the security is expected to decline in value over the next year.

The distribution of ratings across Fintrust’s entire company universe is 64.3% Buy, 28.6% Hold, 7.1%Sell, and 0% Short

Key Figures

Key figures pricing data reflects previous trading day’s closing price. Other applicable data are trailing 12-months unless otherwise specified.

- ROE 27.5% ROA 7.4%

- ROIC 13.0%

- Debt / Assets 30.3%

- Payout Ratio 0%

- Revenue (bil) $252.1

- Net Income (bil) $12.1 Outstanding (mi) 503.0

- Market Capitalization ($ bil) $946

- Beta 1.24x

- Adj. EPS (17A) $6.15

- Adj. EPS (18A) $20.14

- Adj. EPS (19E) $24.59

- P/E (17) 197x

- P/E (18) 359x

- P/E (19) 56x

- Est. 2017-2019 EPS Growth Rate 44.2%

Analyst’s Notes….Continued

- At the time of our initial report (July 24, 2017), Amazon was valued at $1,025.67 while BTC traded at $2,779 or a ratio of .369. We had a price target of .04 BTC, $640, or .11 gold oz which implied a BTC price of $16,000, a gold price of $5,800, or a decline in Amazon’s share price in USD. We point this out given that our initial BTC target was surpassed in December 2017. Based on today’s level of monetary insanity we have a BTC target of $20,568 and a gold price target of $6,652. At today’s BTC price of $9,500.71 the ratio of Amazon’s share price to BTC is .201 and while Amazon’s share price to gold ratio is roughly 1.42.

- Fintrust Brokerage Services is raising our Sell rating to Hold, and we are raising our nominal price target price from $1,111 current USD to $1,611 on the basis of our dividend discount model and current interest rates. Our target prices relative to BTC is .078 and our gold relative target is .24 gold ounces in our real purchasing power price estimates. This represents 15.7% nominal downside from today’s price of $1,911.

- As repeatedly stated in our reports, our estimates are naturally wide given we are in the midst of the largest money debasement in a “Western” country, since John Law in 1720 or the German hyperinflation of 1914-1923. Our valuation calculations under various scenarios range from a low of $1,170 to a high $2,550 per share in current USD. The wide range of estimates is the natural outgrowth the company’s high growth rates and historically low interest rates. Discounted cash flow models for high growth companies in a negative to near zero interest rate environment return nearly infinite prices for the value of an equity that invests cash today and promises cash tomorrow because cash today has nearly no value, while cash later, if it materializes, has potentially large value.

- Using Valueline, we calculate that Amazon has realized a 10-year historical growth rate in equity of 28%. In addition to our own analysis, we used Valueline’s 2020 earnings estimate of $35.60 and projected cashflows forward for 20 years and then discount those earnings back at 6% and added this sum to Valueline’s estimated 2019 book value estimate ($131.55) to derive a fair value estimate of $2,011. At the current $1,911 per share price, we estimate that the market is discounting Amazon’s like a 20-year monopoly that will sustain a 16% growth rate.

- While we understand the market’s pricing for AMZN, we continue to note that one of history’s other great trading, logistics and information monopolies, the Dutch East India company, realized returns of 18% for 200 years, after being granted a 21-year monopoly, but its earnings and dividends were irregular in amount and form. In addition, we note that the company’s stock price reached a record low dividend yield of 3.5% and record stock price high of just over $1100 per share, during the period that coincided with the peak insanity of John Law’s monetary system in 1720. Using Valueline’s 2020, $70.25 per share cashflow estimate for each Amazon.com share and dividing by 3.5% we derive a $2007 price. Importantly for price targets, Amazon.com retains its earnings, whereas the Dutch East India Company distributed its earnings (source: globalfinancialdata.com), as a result, the share price, book value, and our estimates of fair value would

be expected to continue to increase over time.

Conclusion, Recommendation & Risk

Our conclusion, recommendation and risk assessment remain the same as in our previous reports.

As recorded by Washington Irving, John Law’s “System” eventually collapsed as “capitalist gradually awoke from their bewilderment” in the system which was designed to “depreciate the value of gold and increase the illusive credit of paper.” As a result of this awakening, Law was forced to reduce the value of the bank’s notes by one-half and the shares of CDO fell from 9000 to 5000 livres. While the bank notes were restored to their full value, Irving reports that “government itself had lost all public confidence equally with the bank.” (any chance of a collapse in political confidence or confidence in the central banks?)

In turn, this failing of confidence in government, led to a massive hyperinflation as paper money was refused. Irving reports that jewels, precious stones, plate, porcelain, trinkets of gold and silver, all commanded any price, in paper while land was bought at fifty years’ purchase …Monopolies now became the rage among the noble holders of paper” (got your FANG stocks?) Law was forced to flee France and Irving quotes Voltaire as saying, “He was a quack to whom the state was given to be cured, but who poisoned it with his drugs, and who poisoned himself.”

We can name a few bankers worthy of such modern praise. Should they be so bold as to read this report, we would encourage them to read The Great Disorder by Feldman and to remember that economist used to also be moral philosophers. When you devalue money and remove its ability to act as a store of value – you devalue the man who prudently saved and you steal from him the excess of his labors – as periods of hyperinflation have repeatedly shown, once a man has been devalued economically, it is a short step to his devaluation physically. It is not the moral obligation of the central bank to finance every bad political idea. The proper moral role of the central bank is to lend against good collateral at high rates of interest during times of economic stress, not finance anything, anywhere, at any time at low rates of interest. If central bankers no longer hold themselves accountable, our analysis of history suggests that they might eventually and rightfully be driven from the country under the threat of tar and feathers.

Recommendation:

Our $1,611 price target reflects Amazon.com potential growth rate, strong balance sheet and ability to internally finance acquisitions, historic generation of steady gross margins and other financial metrics. Given its modestly unattractive valuation, we believe that AMZN is appropriate at lower valuations for a long term holding for risk-tolerant investors. Acqusitions, if chosen correctly and integrated successfully, add scale and scope in an industry that rewards both attributes, and could potentially drive share value higher than our estimate, whereas competition could compress margins. Given our review of the company’s historic operating and financial results, we rate management as highly capable, and focused.

Risk to our recommendation:

Risk include, but are not limited to, greater competition for AWS from other technology companies, anti-trust, political and business uncertainty, F/X fluctuations, the failure to successfully integrate acquisitions, and increased operating cost for a larger proportion of sales. Finally, we believe the stock market as a whole and the value of nominal price generally could be volatile as the system of quantitative easing collapses.

Price Chart

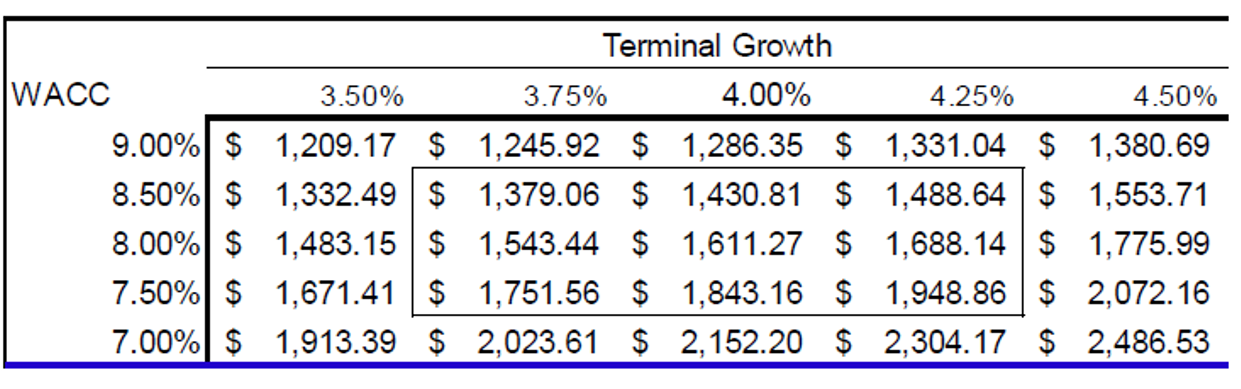

We performed a DCF evaluation of AMZN based on our 10-year forward earnings forecast, which is summarized in the preceding table. Our key assumptions are that (1) AMZN’s Cost of Capital is 8.0% and that (2) the Company’s discounted Terminal Value is driven by an assumption of 23.0% ongoing revenue growth. Our model indicates that the shares’ target price is $1,611 or % downside. As the following Share Price Matrix illustrates, the target price is sensitive to very modest changes in WACC or perpetual unlevered free cash flow growth rate assumptions.

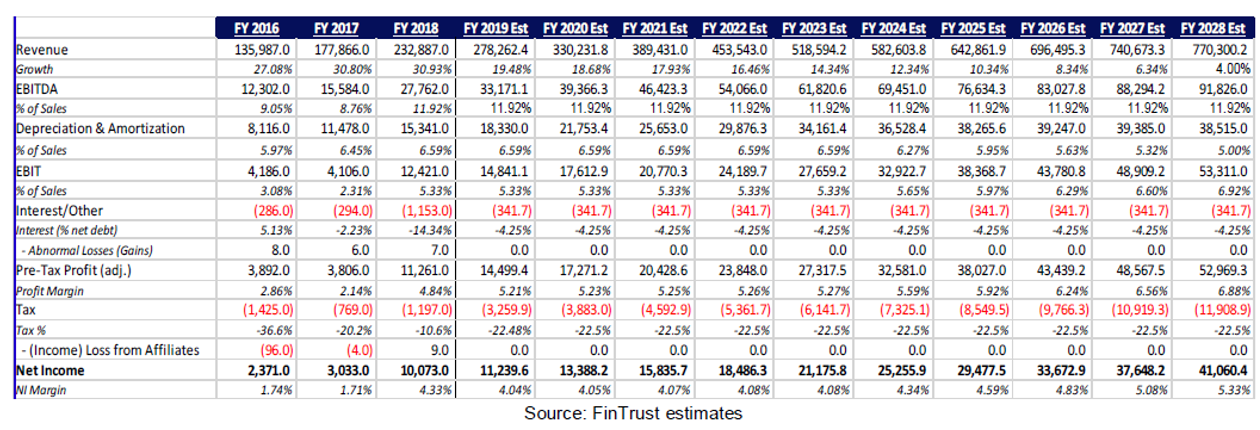

Financial Review: AMZN

Source: FinTrust estimates

*Important Disclosures:

Analyst Certification: We hereby certify that the views expressed in this research report accurately reflect our personal views about the subject company and its securities. We also certify that we have not, will not, nor are presently receiving direct and/or indirect compensation in exchange for any specific recommendation in this report. In addition, said analysts have not received compensation from any subject company in the last 12 months.

Ownership and Material Conflicts of Interest:

An analyst or a member of his household may not purchase the securities of a subject company 30 days before or 5 days after the issuance of the research analyst’s report or a change in ratings or price targets, trade inconsistent with the views expressed by the research analyst, and all transactions in the subject company (ies) securities for the research analyst’s personal trading account must be approved.

The research analyst nor a member of his household own any of the securities of the subject company including any options, rights, warrants, futures or long or short positions. Neither the research analyst nor a member of his household own 1% or more of any of the securities of the subject company based upon the same standards used to compute beneficial ownership for the purpose of reporting requirements under 13(d) of the Securities Act of 1934, as amended.

The research analyst or household member is not an officer, director, or advisory board member of the subject company.

The research analyst has not made a public appearance in front of more than 15 person to discuss the subject company and does not know or have reason to know at the time of this publication of any other material conflict of interest.

The firm has no knowledge of any material conflict of interest involving the company mentioned in this report.

At the time of this report, Mr. Gillespie owns bitcoins, ether, and other cryptocoins, Alphabet shares, and has exposure to various gold and silver related investments including gold mining shares, metals, long volatility, and international equity related mutual funds and ETFs.

Receipt of Compensation:

The firm does not engage in investment banking activities.

The subject company (ies) has not been a client in the past 12 months preceding the date of distribution of this research report and is not currently a client. The firm has not received non-investment banking compensation for products or services or other non-securities services from the subject company or any affiliated company.

The research analysts at the firm do not receive any compensation based on investment banking revenues and may be paid a bonus based upon the overall profitability of the firm.

Investment Banking Relationships:

The firm has not managed or co-managed a public offering or received investment banking compensation in the past 12 months regarding the subject company (ies).

The firm does not expect to receive or intend to seek investment banking compensation in the next 3 months from the subject company (ies).

Additional Important Disclosures…

Securities offered through Fintrust Brokerage Services, LLC (Member FINRA and SIPC) and Investment Advisory Services offered through Fintrust Investment Advisory Services, LLC. Any views expressed in this message are those of the individual sender, except where the message states otherwise and the sender is authorized to state them to be the views of any such entity. Trade instructions may not be accepted via email. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such in the text of the email. Past performance is not necessarily indicative of future returns. Performance numbers have not necessarily been independently reviewed or audited and therefore we make no representation as to its accuracy. Any reference to the terms of any contracts should be treated as preliminary only and subject to our formal written confirmation.

This report is prepared for general circulation. This report is not produced based on any individual persons or entities investment objectives or financial situation and opinions expressed by the analyst are subject to change without notice. This report is not provided to any particular individual with a view toward their individual circumstances. Investors should consider this report as only a single factor in making an investment decision. Securities prices fluctuate and investors may receive back less than originally invested and are not guaranteed.

This information should not be construed as legal, regulatory, tax, or accounting advice. Any reference to the terms of any contracts should be treated as preliminary only and subject to our formal written confirmation This message (and any attached materials) is for the sole use of the intended recipient(s) and may contain information that is privileged, confidential and exempt from disclosure under applicable law. Any review, dissemination, distribution or duplication of this communication is strictly prohibited. If you are not the intended recipient, please contact the sender immediately by reply e-mail and destroy all copies of the original message.

No part of this document may be copied, photocopied, or duplicated in any form or other means redistributed or quote without the prior written consent of the firm. This report and its contents are the property of Fintrust Brokerage Services, LLC and are protected by applicable copyright, trade secret or other intellectual property laws. United States law, 17 U.S.C. Sec.501 et seq, provides for civil and criminal penalties for copyright infringement.

The firm does not make market in securities.

The firm does not buy or sell the subject company (ies) securities for its own account.

The firm does not buy or sell subject company (ies) securities on a principal basis with customers. The firm’s employees, or customers, may buy or sell the subject company (ies) securities.

Although the statements of fact in this report have been obtained from and are based upon outside sources that the firm believes to be reliable, the firm does not guarantee the accuracy or completeness of material contained in this report. Any such estimates or forecasts contained in this report may not be met. Past performance is not an indication of future results. Calculations of price targets are based on a combination of one or more methodologies generally accept among financial analysts, including but not limited to, analysis of multiples and/or discounted cash flows (whether in whole or in part), or any other method which may be applied. Rating, target price and price history information on the subject company (ies) in this report is available upon request.

To receive any additional information upon which this report is based please contact (864) 288-2849, or write to:

Fintrust Brokerage Services, LLC

attn: Research Department

124 Verdae Blvd, Ste. 504

Greenville, SC 29607

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research