Interview

Editor’s note: The Q & A below is an interview conducted by Fintrust Director of Marketing and Client Engagement Paige Siniard, with Allen Gillespie, CFA®, President, Managing Partner Investments.

November 2019

Q3 2019 The Caddyshack Market

Q: Allen, you recently called this the “Caddyshack Market,” can you explain?

A: Sure. Caddyshack was a 1980s comedy movie which starred Bill Murray, Chevy Chase, and Rodney Dangerfield. The movie is set at the upscale Bushwood Country Club. It has the expected mix of old money, nouveau rich and poor working kid storylines, plus a man versus nature, or should I say, groundskeeper v. gopher plotline.

There is one scene, however, that helped cement Bill Murray’s reputation as a comedic actor. The club members and their families are enjoying the club’s swimming pool when a little girl yells “doodie in the pool.” Well, of course, everyone starting scrambling for cover. Calm is restored when the groundskeeper, Bill Murray, picks up the “doodie,” realizes it is a Snickers bar, and proceeds to eat it.

Q: And you think this scene is reflective of the current stock market, why?

A: Well, in our market there is an exclusive “venture capital” club in Silicon Valley. As a result of “TINA” (see Q1 Wealth Management Quarterly), there are a lot of nouveau rich companies like UBER, AirBnB, Jule, Peloton, Beyond Meat, and WeWork that trade at extreme valuations. As financial conditions have become tighter, due to last year’s Federal Reserve interest rate hikes, these companies have been racing to tap the public equity markets at high valuations.

When WeWork tried to go public, people looked at all the red-flags in their regulatory filing (S-1) and screamed “doodie in the pool.” Now, there is a scrambling going on, and the valuations for many high flying technology businesses are starting fall. Many banks were expecting their loans to be repaid from the IPO proceeds, so they are panicking a little. WeWork has over $50 billion in office lease obligations, so landlords are concerned. This failed IPO has created a growth to value rotation in the market. The period reminds me of what happened when the technology bubble burst in 2000.

EXECUTIVE SUMMARY

FinTrust Investment Review Team:

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis, CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

- Monetary Policy: Accommodative. In the fastest reversal in Federal Reserve policy on record the Federal Reserve has now cut rates 3 times in 2019 after having announced its intention to increase rates as recently as December 2018.

- Fiscal Policy: Neutral, checks and balances. Historically, the stock market begins to discount the economic impacts of elections and policy changes in first quarter of the election year. Stay posted for more information.

- Yield Curve Watch: After the Federal Reserve cut interest rates in October, the yield curve has regained a flat v. inverted shape, indicating the bond market has already priced in a global slowdown for 2020 and a recovery starting in 2021. Meanwhile, it appears more economically sensitive equities and inflation sensitive assets are attempting to trough. Economic inflection points can lead to increased market volatility.

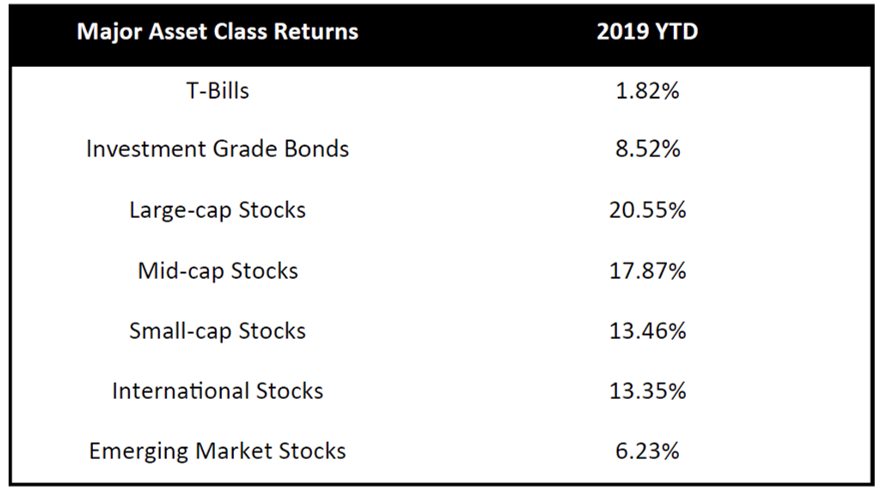

Source: Bloomberg as of 9/30/19

Q: Remind us what happened when the 2000 technology bubble burst. I remember it was pretty bad, right?

A: Yes and no. During the 2000-2002 period, the market averages declined but more stocks went up than went down. Initially, this might appear counterintuitive but it is easily explained. Due to the economic slowdown in Asia in 1997-1998, people had crowded into a handful of large cap growth stocks and fast growing technology stocks. They were looking for investments that were viewed as not being economically sensitive. But, as the cycle turned, money began to flow out of the market, which was dominated by the 4 horsemen of the Nasdaq (Cisco, Microsoft, Dell, and Intel) and other technology companies, and into small-cap value stocks and bonds.

Think of it this way. Apple today has over a $1 trillion market cap. If just that one stock were to sell-off 10%, but that money flowed into 100, $1 billion market cap size companies, well, they would double. At the same time, this would lead to no change in the index.

The 2000-2002 period is a great example of the importance both asset allocation (money from stocks into bonds) and strategy diversification (money from growth stocks into value stocks).

Q: Should investors be reallocating from stocks to bonds now?

A: While we are seeing a rotation similar to the 2000-2002 period, it is not as extreme because bond yields are very low. People are less willing to sell stocks than to buy bonds. In fact, there are many value areas of the global markets where dividends yields are over 100% higher than bond yields. You also have the Federal Reserve aggressively lowering interest rates in order to further reduce the attractiveness of bonds. Back in 2000, bond yields were nearly 4% greater than dividend yields – so strong asset allocation changes were appropriate.

Q: You mentioned strategy diversification. Should investors consider a strong strategy shift, like growth to value stocks?

A: Currently, we think slight strategy tilt towards value makes some sense. While the rotation is similar, like the stock v. bond equation, the growth v. value difference is not as large as during the 2000-2002 period. For example, the valuations of large cap growth stocks like FANG (Facebook, Amazon, Netflix, and Google) are high, but they are more reasonable than the valuations of the 4 Horsemen of the Nasdaq during the 2000-2002 period.

Another important difference between the two periods, I think, is the fact that the highest valuation “unicorn” companies are still largely owned by venture capital and private equity funds. As a result, the valuation compression of earlier stage growth companies is having less of an impact on the public markets.

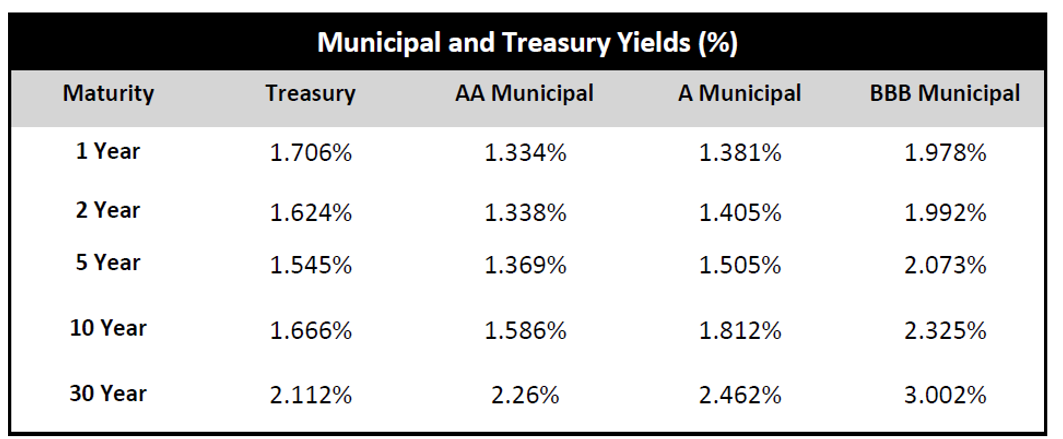

Source: Bloomberg as of 9/30/19

Q: Given the rotation, what should investors do?

A: We may see some global growth surprises to the upside, and we think a slight tilt toward that possibility makes some sense here. If there is one place where we strongly differ from most investors, it is that we are becoming much more positive on international markets for several reasons.

First, there is sentiment. International markets have largely underperformed for a decade. The headlines look terrible. The poor performance of international markets has improved valuations. In fact, most international markets now offer positive carry or greater cashflows when Compared to domestic markets. It is also normal for the headlines to look bad at inflection points, and the international markets have plenty of negative headlines.

Q: Can you give us some examples of the negative headlines?

A: Let’s start with Brexit and the potential break-up of the European Union. The headlines would tell you this is a horrible thing and the British cannot even agree to hold an election. If you look back at your history books, however, you will see that the British were the first to leave the Gold Standard in 1931. As a result, they were the first to recover from the Great Depression. It took the U.S. until 1933 to leave the Gold Standard. Eventually, over 27 countries left the Gold Standard— this is why Europe is making it so difficult for the British to leave. If they were smart, they would recognize this is actually in everybody’s interest.

Next, let’s look at the Japanese market. It is about to hit a new high for the first time in 30 years. If you bought the U.S. market under those conditions you would have been buying in the early 1950s and 1982, both really good times to buy. Due to the population decline in Japan and their long history of negative interest rates, we believe Japan might lead the robotic and cryptocurrency revolutions.

Q: What about China?

A: From a purely economic standpoint, we have to recognize, that China is a large enough economy to be self-sustaining without the U.S. Economically, we think the U.S./China trade war is more like the 1980’s Cola wars between Coke and Pepsi. They’re both good investments.

Because we are considering two countries, and not two cola companies, politically and militarily the trade war is a very different animal. There are many things that concern us about China’s human rights policies. This is playing out in certain “strategically important” industries like energy, aerospace, telecommunications and semiconductors. We are seeing supply chains remade and redesigned due to strategic considerations.

Q: What impact is this having in the markets?

A: I think the best example of the impact of the trade war is in the 5G telecommunications space. Before the trade war, many telecommunications companies were sourcing equipment from the Chinese company Huawei. By some estimates, Huawei accounted for nearly 26% of the industry. When the U.S. cut that supplier out, telecommunications companies had to find new suppliers. This naturally caused demand to fall, which slowed economic statistics. We have been seeing the bond market prices impacted in this slowdown.

Because of the unique circumstances outlined above, we believe that the fall in demand is only temporary as telecommunications companies scramble to sure up their supply chains. There is still an appetite for 5G, and this differential view is supported by several historic instances of short-lived decreases in demand. During the 2000-2002 period, following the Y2K rollout, demand fell off a cliff, and in the 2008 recession, demand also collapsed due to the housing crisis. We see current conditions more as a “demand delayed” than “demand is gone” slowdown.

Q: Any final thoughts from the team?

A: There is a difficult set of choices right now. Long-term, relative to cash and bonds – stocks look attractive, but against their own history, stocks are not cheap. We think it is really important to maintain a methodical and disciplined process in both evaluating asset allocation and strategy diversification. Given our view, we also think systematic rebalancing, less correlated strategies, and less correlated assets should be used to diversify traditional stock and bond portfolios.

ECONOMIC OUTLOOK

MONETARY POLICY

This year has been almost an exact reversal of last year. The Federal Reserve has cut interest rates three times. This 30% decline in interest rates has led to an almost equivalent increase in equity prices. In our estimation, the Federal Reserve has shifted from “neutral” to “accommodative” with its latest interest rate cut. We believe the Federal Reserve would prefer to be “neutral,” but the trade war dynamics are forcing a more accommodative stance. Historically, equities are positive in the year following multiple rate cuts.

FISCAL POLICY

We are actually big fans of split government, particularly during times when the rhetoric is high. Equities have historically been flat in the year following the loss of the House by a Republican president. As a result, we believe fiscal policy will shift back to neutral as the stimulus from the tax cuts runs off. This neutral state should continue until after the election.

THE DATA

The yield curve is beginning to regain its shape after having been inverted. The yield curve is a leading indicator, and we believe it has now fully priced in an economic slowdown for 2020. We believe the yield curve is now starting the process of pricing in any subsequent economic upturn.

The equity market downturns of both 2001-2002 and 2008 occurred after the yield curve had steepened following a long period of being inverted. In considering other time periods, however, we find that equities could potentially rally following a yield curve inversion if they are cheap, and investors begin to anticipate an upturn in earnings.

Cash and Cash Equivalents

The trade war creates a new and interesting wildcard. President Trump is pushing the Federal Reserve to lower rates to zero to match Europe and Japan and to offset the currency depreciation of the Chinese Yuan. After nearly a decade of being below the inflation rate, cash and cash equivalents once again offer investors roughly the equivalent compensation as inflation. If Trump’s argument wins, then we believe it would cause a blow-off (huge upside) move in equities and gold, as it would force money out of bonds and cash.

Investment Grade Fixed Income

The bond market is currently pointing toward deteriorating conditions, but interest rates continue to be very low by historical standards. As a result, we think investment grade bonds still have a defensive roll to play, but do not offer much in the long run.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Over the last few years, when cash rates were very low, these strategies were not as attractive as some more traditional credit and interest rate carry strategies. Now, however, given the low level of long-term interest rates and the associated interest rate risk, we believe event, fixed income, and equity arbitrage related strategies offer a compelling risk return opportunity. We believe the return profile is reasonable, and the risk profile is better than either duration or credit.

Core Equities

Last December, the Dow Theory gave a sell signal. After the third Federal Reserve interest rate cut in October, Dow Theory moved into a confirmed uptrend. As previously mentioned, it is not uncommon to see large secondary moves after the change in primary trend. We are modestly constructive on equities, but we do not believe investors should chase the market as during the Quantitative Easing (QE) period that ran from 2009-2018. We also believe the low interest rate outlook in the U.S. will lead investors to seek returns in international markets given their higher yields.

Tactical Equities

While nearly every strategy and asset class has underperformed domestic U.S. equities, we do see some evidence of money returning home to international markets on a country by country basis. Other tactical equity strategies, like long/short equity, have historically performed better when short-term interest rates are higher. The duration of long only equities has been estimated to be 30-50 years, so given the potential for interest rates to rise, we believe tactical equity strategies are becoming increasingly attractive on a relative value basis.

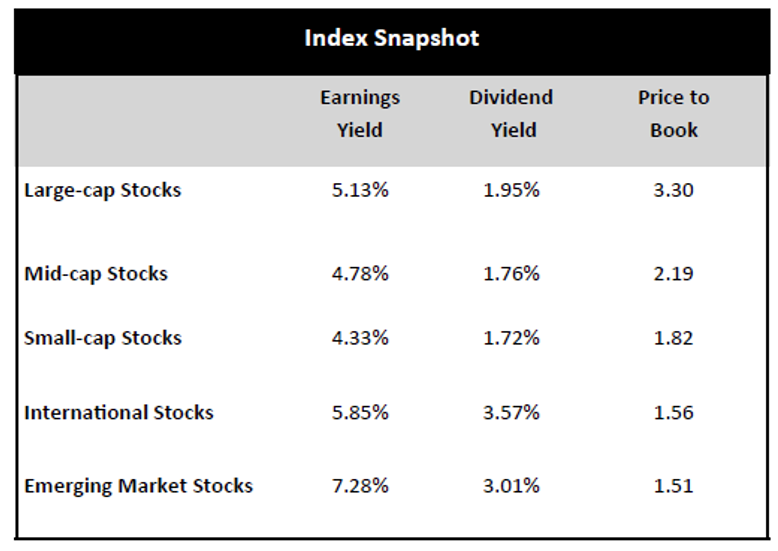

Source: Bloomberg as of 9/30/19

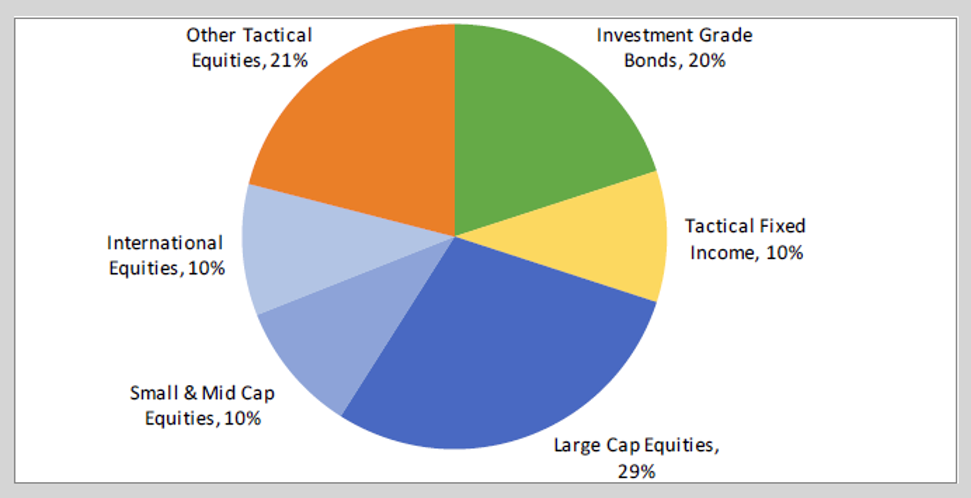

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 9/30/2019. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research