Interview

Editor’s note: The Q & A below is an interview conducted by Fintrust Director of Marketing and Client Engagement Paige Siniard, with Allen Gillespie, CFA®, President, Managing Partner Investments.

April 2020

Q1 2020: Toilet Paper Markets

Q: Allen, last quarter you were talking about the economic war between the US and China, nationalist v. globalist, the virus, social media wars, generational changes to investing, and crisis, but your comment that “you can’t buy toilet paper” in a hyperinflationary crisis really sticks out now. Can you help our readers make sense of what we are seeing?

A: I will try. As Gen. Rumsfeld famously said, “…there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know.”

Here is what I think we know. I believe, that in war and crisis periods, the universal urge to buy toilet paper is a physical manifestation, of the psychological urge, to maintain one’s human dignity and agency amidst uncertainty. The news articles about toilet paper shortages therefore suggest we are definitely at war or in a crisis.

Q: Do you believe we are at war?

A: I do, but not in the conventional sense of the word.

Q: Can you expand on that?

A: Economist have been taught, for generations, that what got the US economy out of the Great Depression was World War II government spending. Europe meanwhile was saved after the war by the Marshall Plan. The Global Financial Crisis, in 2008, was the first time since the Great Depression that home prices had fallen at a national level. As a result, economist have wondered whether massive, World War II level spending, might be necessary to shock the economy out of its malaise. Obviously, though, there has been a lack of political consensus for that level of government spending and economic involvement.

I would also point out that modern war does not necessarily have to be a “hot” war or have conventional enemies. Cyber wars are routine and from an economics and human life perspective, spending on a “war’ against a invisible, non-human, non-living organisms is preferable to a war against other humans.

Third, I think people should listen and consider carefully President Trump’s comments and questions regarding the War On Terror, since 9/11. The US has spent $6 trillion overseas for the purposes of killing terrorists— and what have we gained? It is a truth most of us do not want to face.

EXECUTIVE SUMMARY

FinTrust Investment Review Team:

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis, CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

- Monetary Policy: Accommodative. The Federal Reserve cut interest rates 3 times in 2019 and launched QE4.

- Fiscal Policy: Accommodative. The stock market begins to discount the economic impacts of elections and policy changes in first quarter of the election year.

- Covid-19 a Global 9/11? We believe Covid-19 is an event which will significantly change the U.S. economy and the global economy. Most immediately, inside the $2 Trillion stimulus bill, we see the emergence of a Made in America 2025 plan focused on the same industries outlined in China’s Made in China 2025 plan.

- Yield Curve Watch: The yield curve has regained its slope flowing the $2 trillion Stimulus Bill and is now pointing toward a weak economic recovery. Corporate credit curves still indicate high levels of financial stress.

We have lost thousands of honorable servicemen, and foreign countries have lost tens of thousands of people. Meanwhile, China has bought our bonds and used the interest from those bonds to develop its economy toward its Made in China 2025 plan. You can read more here in the U.S. Chamber of Commerce report, “Made in China 2025: Global Ambitions Built on Local Protections.”

US companies have moved production to China to save on labor costs. Here is Ray Dalio, manager of the largest hedge fund in the world, summarizing the issue in 1 minute.

I think the simple economic alternative view to this reality is—what happens if we spend $6 trillion at home? What happens if we spend $6 trillion trying to make the world a better, safer place, in time to compete with China by 2025? I think we are about to find out.

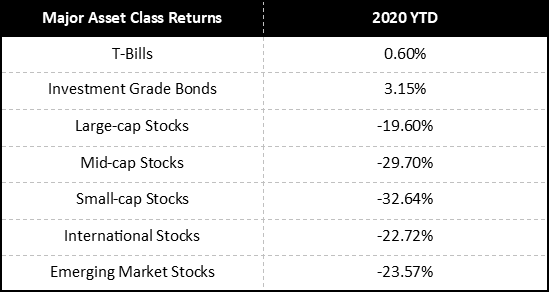

Source: Morningstar Direct, As of 12/31/2019

Q: You think the government is about to spend an additional $6 trillion in 4 years?

A: Yes. Government interest rates are now close to zero, neutralizing interest payments to foreign holders of US debt. The stimulus bill that just passed is $2 trillion, and it passed on a nearly unanimous vote. Congress is already working on the next phase of spending which will include infrastructure (5G, roads, airports, bridges, etc), and all the money will be spent domestically.

Q: These don’t sound like bad things, so is there something we are missing?

A: The optimistic view is that in a global war against “unseen” enemies, maybe the US and China can develop more of a Coke v. Pepsi, Georgia v. Florida, Clemson v. South Carolina type rivalry. That would be incredibly positive for the world. The negative view would be that the silent war goes hot.

Unfortunately, right now, there are signs of both—if one follows the Fentanyl Crisis and knows the history of the Opium Wars, one sees the hot side—if one focuses on naval activities, China’s One Belt One Road Program, and the new developments with Space Force, the arrest of a Harvard professors and Chinese Nationals associated with China’s Thousand Talents Program —one sees the potential hot side. On the positive side, after the virus, we may both go to our respective corners like two champion heavy weight fighters.

Q: Last quarter, you stated that social media companies were creating large battlegrounds. What is the role of information now?

A: In war, information, disinformation, and propaganda are important weapons. We know this now takes place inside of social media platforms, through amplification and redirection campaigns. During wars, however, financial markets are probably better source of information than news outlets because they focus on future events rather than current news.

Q: Can you give us an example of markets discounting outcomes during war?

A: Sure, during World War II the US stock market made its low on April 28, 1942, the day of Roosevelt’s 21st Fireside Chat—Economic Sacrifice. The US had just lost at Bataan.

From a military perspective, the Allies were not exactly winning the war in April, 1942. Yet the market sensed that was the inflection point. Why? The full text is available thru the link, but here are a few of his words I wanted to highlight.

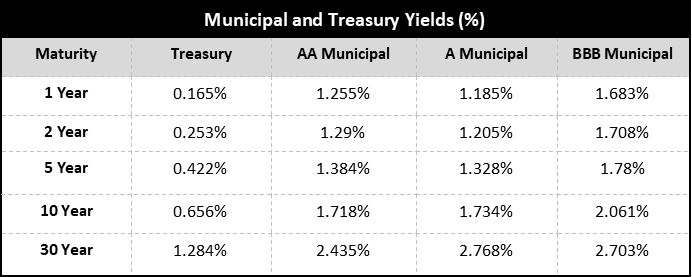

Source: Bloomberg as of 12/31/19

“But there is one front and one battle where everyone in the United States — every man, woman, and child — is in action, and will be privileged to remain in action throughout this war. That front is right here at home, in our daily lives, (and) in our daily tasks. Here at home everyone will have the privilege of making whatever self-denial is necessary, not only to supply our fighting men, but to keep the economic structure of our country fortified and secure during the war and after the war. This will require, of course, the abandonment not only of luxuries but of many other creature comforts. Every loyal American is aware of his individual responsibility.

Whenever I hear anyone saying “The American people are complacent — they need to be aroused,” I feel like asking him to come to Washington (and) to read the mail that floods into the White House and into all departments of this Government. The one question that recurs through all these thousands of letters and messages is “What more can I do to help my country in winning this war”?

To build the factories, (and) to buy the materials, (and) to pay the labor, (and) to provide the transportation, (and) to equip and feed and house the soldiers, sailors and marines, (and) to do all the thousands of things necessary in a war — all cost a lot of money, more money than has ever been spent by any nation at any time in the long history of the world.”

We are now spending, solely for war purposes, the sum of about one hundred million dollars every day in the week. But, before this year is over, that almost unbelievable rate of expenditure will be doubled.

All of this money has to be spent — and spent quickly — if we are to produce within the time now available the enormous quantities of weapons of war which we need. But the spending of these tremendous sums presents grave danger of disaster to our national economy.

When your Government continues to spend these unprecedented sums for munitions month by month and year by year, that money goes into the pocketbooks and bank accounts of the people of the United States. At the same time raw materials and many manufactured goods are necessarily taken away from civilian use, and machinery and factories are being converted to war production.

You do not have to be a professor of mathematics or economics to see that if people with plenty of cash start bidding against each other for scarce goods, the price of those goods then goes up.”

Q: Is this why last quarter you used the word “hyperinflation”?

A: Absolutely. It is an unavoidable reality that our dollars will be worth less in the new environment—already the Federal Reserve’s balance sheet has expanded from $4.5 trillion to $6.5 trillion. Fortunately, paper dollars can substitute for the missing luxury we previously mentioned.

Government, of course, will do its best to contain the coming price shocks, as Roosevelt explained in the rest of the speech, but it will not be able to completely stop them.

Q: So, what should an investor do?

A: Naturally, traditional fiat currencies are likely to lose value against hard and virtual currencies in the new environment, so one can diversify the forms of one’s “cash” savings.

I think in the stock and bond markets one will find things uneven. As Roosevelt said, things will be taken away from civilian use and other things will be converted. This means that certain segments of the economy will die but new opportunities will also open up.

The BIG THEME I see opening up is Made In America 2025, as the competitor to Made In China 2025. The industries included in various reports include: Aviation Equipment, Robotics, Electrical Equipment, New-Energy Vehicles, High-End Numeric Control Machinery, Medical Devices, Next-Generation IT, High-Tech Maritime Vessel Manufacturing, Advanced Rail, Agricultural Machinery, and Biomedicine.

Inside the stimulus bill was a lot of money for things like rural broadband to support remote work and telehealth. There was money for zoologics and other healthcare items. There was money for the aviation industry and small business.

I also see a BIG THEME in the transition from the Baby Boomer Economy to the Millennial Economy. What do I mean by that? Online, local, just in time purchases from short supply chains, with a focus on efficiency. Millennials are now the primary purchasers in many categories including homes. Businesses better know what they want.

Q: Any final thoughts?

A: Wars can be quick, or they can be long.

Wars can be internal, between countries, or global, and wars can be successful or unsuccessful.

Wars always usher in new societal norms, patterns of behavior, and remake the economy.

Finally, It is tough for us Generation X types, but during “wars” government grows, the private sector shrinks, and individual liberties get restricted, and the young people fall in line.

Let me be specific. The very first Amendment in the Bill of Rights states that “Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof or abridging the freedom of speech or of the press, or the right of the people peaceably to assemble and to petition the government for a redress of grievances.”

The way government is getting around this restriction currently is by allowing health officials and State Governors to restrict the people’s ability to peaceably assemble. Congress hasn’t done anything to create this shutdown, but it most certainly has happened.

Or what about the fourth amendment and one’s right to secure your persons, house, papers, and effects against unreasonable search and seizure?

How do you think governments are going to treat your biological data now? Millennials grew up with cell phones, and some do not give much thought to their data being tracked and shared. Generation X grew up with computers and computer hackers, and with movies like War Games and Red Dawn where the world is brought repeatedly to the edge of total destruction by government, only to be saved by a free-thinking individual at the last second.

QUICK TAKE: MAJOR ASSET CLASSES

Cash and Cash Equivalents

Since last quarter, President Trump has in fact gotten the Federal Reserve to lower rates to zero to match Europe and Japan. As a result, we believe there could be a flight to safety in alternative currencies like, gold, and cryptocurrency.

Investment Grade Fixed Income

Due to the virus outbreak in China, and business shutdowns, investment grade corporate interest rates have risen materially and now reflect severe recessionary conditions. We think investment grade bonds still have a defensive roll to play, and now offer better return potential. We would not expect material appreciation, as economic conditions are likely to remain stressed, but interest rates appear to account for likely credit losses.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given the stresses in credit, we continue to favor arbitrage related strategies, as we do not yet believe high yield credit fully reflects the economic challenges ahead.

Core Equities

Since our last report, equity prices have declined materially. As a result, we believe equities are slightly undervalued relative to historical valuations. As a result, we are modestly constructive on equities, but we believe individual security selection rather than asset allocation will be increasingly important going forward due to the structural changes in the economy. Given the high levels of volatility, we would not overweight equities beyond investor risk determined allocations.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward trade-offs. Tactical equity strategies, like long/short equity, option based strategies and market neutral strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low interest rates and the likely structural changes to the economy.

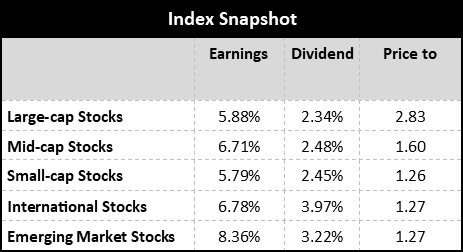

Source: Bloomberg as of 03/31/20

Other Markets

Other markets like gold, cryptocurrency, and real estate do offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. We are concerned that recent events will accelerate trends towards online purchasing and remote work, which will increasingly pressure certain real estate sectors. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

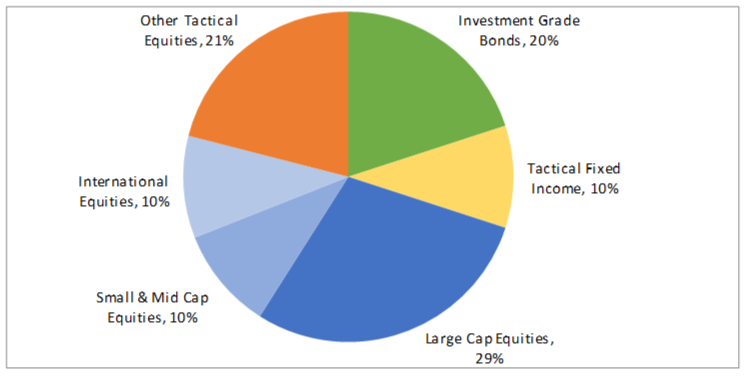

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 3/31/2020. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research