Q4 2023: Long, Dark Shadows

Q: Allen, why title this WMQ “Long, Dark Shadows?”

AG: In natural light, long shadows appear in the winter when the axis of the earth is pointed away from the sun. Halloween with its ghosts, jack-o’-lanterns, and shadows, fittingly announces winter’s approach. Beyond the solstice points, long shadows appear at dusk and dawn, the opening and closing of the day. Shadows, therefore, appear at turning points. Long shadows obscure clear views, but they disappear over time as the world turns.

Like our natural world, financial markets have shadows along with the people and objects which create them. Shadows remind us of the common theme that I try to share with our WMQ readers: that things in life and markets are not always as they appear. Financial market shadows appear at inflection points, obscure clear views of the future, and appear almost uniquely designed to frighten investors. Shadows get investors to either buy the wrong things or to buy the right things at the wrong times.

As a result, it is useful to learn more about shadows, particularly because of the long, dark shadows currently wandering about the financial landscape.

Q: What are some of the financial market’s “long, dark shadows?”

As I sat down to write this WMQ, the Israel/Hamas war broke out. It is a conflict that has been going on for a long time, and which casts long, dark shadows over our world. Prior to this attack, the November 2023 oil contract rose persistently from $69.73 at the end of June to a peak of $95.03 on September 28, topping just days before the Hamas attack on Israel.

How financial markets discount events such as this attack, the Ukraine War, or a 9/11 terror attack is an interesting area of study and discussion by academics and regulators. Donald Rumsfeld, the former Defense Secretary, is famous for saying,

“There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.”

While many found his comments comical, I think the economic literature and the markets understand the nuances and discount various types of events differently. For example, the Hamas attack was unknown except to insiders, during the planning stage, but now it is a known by the market. Since this was a specific event that has passed, the energy market topped just prior to the event, as Hamas’s military capabilities are more limited when compared to Israel.

Allen Gillespie, CFA®, Chief Investment Officer

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis, CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Tightening. The Federal Reserve is positioning for higher interest rates on a secular basis.

- Fiscal Policy: Inflationary. The CBO projects federal budget deficits to average 5.5 percent for the next ten years.

- Economic Vital Signs: Inflationary pressures while high are moderating. Higher oil prices are a negative at current levels.

- Yield Curve Watch: The yield curve continues to be inverted but has recently begun to regain its shape. Fed funds futures currently imply the first Federal Reserve rate cut will occur around May 2024.

Economically, it is important to consider the differences between Hamas and the Israeli Defense Forces (IDF), and their capabilities to make war. It is estimated that Hamas has 30,000-40,000 fighters. Hamas has no Air Force, Navy, tanks, or military vehicles. Meanwhile, according to the International Institute for Strategic Studies’ (IISS) Military Balance 2023, the IDF has 169,500 active duty members and a reserve force of 465,000, battle tanks, heavy infantry vehicles, jets, helicopters, subs, and nuclear arms.

Thus, from a military capabilities comparison standpoint, Hamas is capable of small scall surprise terror attacks on soft targets, but larger governments like Israel are capable of sustained actions. Financial markets, therefore, would be more likely to move ahead and top prior to “surprise events” or “plots” like the Hamas attack. Markets are more likely to move after and in a sustained way on “policy” decisions likely to emanate from large global governments like Israel.

Q: What do you think the “policy” decisions will be, and how will they impact markets?

We still do not know how Israel will respond. Nor do we know how various governments around the world will react to that response. Israel’s prime minister, Benjamin Netanyahu, has called the attack Israel’s equivalent to the 9/11 attacks. As a result, I think it is natural to assume the Israeli Defense Forces will conduct a ground war in Gaza. I also think that much of the fighting will actually occur below ground in the Hamas tunnel network, so the fighting will not necessarily make its way to Twitter feeds. Much of the fighting is going to happen in the shadows, underground, and through intelligence operations which will include social media influencer campaigns.

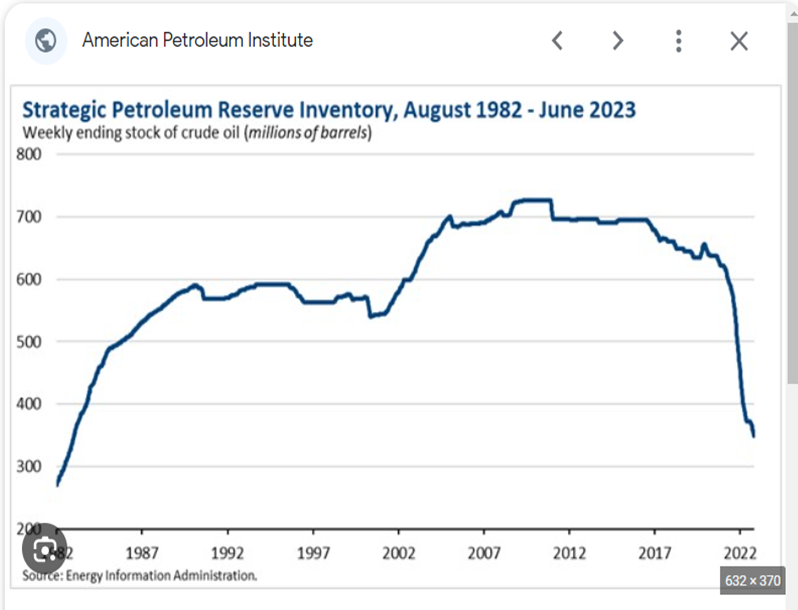

In my research, I did find that following the Yom Kippur War in 1973, the oil states conducted a year-long embargo campaign on Israel and its allies. The oil embargo in 1973-1974 raised the average price of crude oil by over 200% according to data from the Federal Reserve. Increases in energy prices have the power to drive inflation rates higher, particularly for key goods like food. Given that the U.S. has drastically reduced the size of its Strategic Petroleum Reserve, I do think there is a risk that energy prices could be driven unnaturally high as an economic weapon of war.

As we have repeatedly discussed, high energy prices negatively impact consumer spending, which accounts for the majority of U.S. GDP. High prices also encourage substitution and conservation. Given the rise in energy prices during the third quarter, I would currently expect a deterioration in consumer spending, but that is likely already reflected in market prices. If there were to be an oil embargo, more sustainable economic impacts could be expected which would require portfolio adjustments.

Q: Are there portfolio changes investors should consider due to the shadows of war?

Inflation has been called a hidden tax, so one can think of it as a shadow tax. During wars, taxes and inflation tend to go up as governments finance themselves. Inflation distorts prices and obscures our ability to observe real values. Inflation makes prices go up but forces a decline in real values. As a result, I do think investor time horizon planning or hedges against inflation are important considerations for portfolios.

Q: How should investors hedge inflation? Should they buy gold?

These are probably the most common questions we receive from clients. I do believe precious metals like gold are re-emerging from the shadows to be a safe haven asset. Thus, I believe gold does have a role in client portfolios depending on their specific goals, objectives, financial needs, wealth, and time horizons. In the 10 days since the Hamas attack, gold has risen over 8% despite higher interest rates. Now, I would caution because it is a mistake I see a lot of investors make; gold and stocks are not substitutes for each other.

Gold is a substitute for fiat money, and a diversifier away from stocks and bonds. Stocks are ownership in a company and its productive assets. Stocks and gold are related as stock prices are also denominated in fiat currency. Gold’s price is a function of the decline in the purchasing power of a currency, so it reacts more immediately to currency concerns. It may take time, however, for companies to reprice their goods and services, so it can take longer for stock prices to adjust to currency concerns. As a result, over long periods, stocks have historically been higher returning assets than gold, as companies pass through their costs and “outgrow” the inflation. Gold and commodities have traditionally reacted more quickly which makes them good hedges against more immediate wartime inflations and shortages. War increases government financing needs, and the bigger the war, the bigger the financial needs.

The cost of war is high, particularly for the “losing side” of a conflict, which is something politicians rarely consider. War can be very expensive for both sides. For example, after Russia “lost” the “Cold War” in 1989—its currency collapsed in 1998. Following World War I, everyone lost financially. The German Mark fell into hyperinflation by 1923 and the “British Pound Sterling” lost its sterling reputation and reserve status. The pound was finally devalued relative to gold by over 30% in 1931. Within a few years, nearly every nation had abandoned the gold standard. After the U.S. “won” World War II, our currency gained globally and became the “reserve currency” until the Vietnam Era. During the Nixon and Carter administrations, the U.S. dollar fell relative to gold as the U.S. “lost” in Vietnam and the Bretton Woods system collapsed.

Q: What else can you teach our reader about economic shadows?

Shadows are not always negative, particularly as they recede. Since the 2008 financial crisis, market participants have regularly referred to non-bank lenders as “shadow-banks” and their managers as “shadow-bankers.” Shadow-banks are pools of capital that in many regards act like banks, and provide many of the same services as banks, but without a banking regulatory framework. The lessor degree of regulation gives them more flexibility.

Shadow banks are not subject to banking regulations because they do not have “depositors” per se. They have investors, which the FDIC is not on the hook to protect. These investment pools, however, may be subject to a variety of other regulatory restrictions depending on how they are organized.

For example, just past a bank deposit in terms of risk is a basic prime rate money market fund organized under the Securities Act of 1940. Prime rate money market funds make short-term commercial paper loans to high grade borrowers. The hidden tax of inflation has driven interest rates higher, but the higher interest rates flow directly into prime rate money market funds. Many investors are perfectly pleased for their near cash investments to be once again earning something.

Continuing up the risk scale, you get to mutual funds, and private funds organized under various parts of the Securities Act which invest in private debt, private equity, and real estate

These investment funds make business loans, loans against real estate, and invest in a wide range of assets. Private credit funds may be one of the hottest areas of finance at the moment because in a stressful environment they have more flexibility than banks. Since they do not use leverage, these funds can bear more risk than a bank.

I also think cryptocurrency is in the process of making its mainstream appearance from the “shadow banking” system. The shadows and shady figures in crypto are gradually fading. We are moving away from the shady world of Sam Bankman-Fried, the indicted former CEO of FTX and his shenanigans, to the SEC opening up potential approval pathways for firms like Fidelity, Grayscale, Blackrock and WisdomTree to offer crypto associated ETFs. At FinTrust, we can now buy Bitcoin and Ethereum for clients through Fidelity.

Q: Are there other economic shadows which are fading?

Demographically, I think economic shadows are getting shorter. The long, dark shadow of the economic slowdown associated with the aging of the Baby Boomer generation is fading. Economic spending tends to peak around age 50, with the exception of healthcare. As a result, Boomer demographic spending peaked in 2007 (1957+50), but somewhere between 2019 and today, we reached the low of that effect. The average Millennial age is now in the early 30s, and the low point of Generation X (1973) is reaching age 50 now (1973+50). Since the peak of Boomer spending, economic growth has been hard to find, but that should not be a problem going forward. As a result, I think the economic challenges we face are more of a product, business cycle, and policy level than an underlying demographic issue like we have faced for 15 years.

Q: Allen, any final thoughts on today’s economic shadows?

Shadows are a part of our natural world, and they are their longest at inflection points. Similarly, the news, risk and rewards, and relative values in financial market shadows are most extreme and noticed at turning points. The environment reminds me of Charles Dickens famous opening line in A Tale of Two Cities:

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way—in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only.”

There are investing shadows lurking, but shadows do fade. As a friend recently stated, “with investments the best time to have invested would have been 20 years ago, and the next best time is now. There is never a bad time to invest in making the world a better place.”

Sincerely,

Allen R. Gillespie

QUICK TAKE MAJOR ASSET CLASSES

Cash and Cash Equivalents

According to the CBO, the Federal deficit as a percentage of GDP is 5.5%, so short-term interest rates are in line with inflationary spending levels. As a result, we now believe short-term bonds can be utilized by both conservative and aggressive investors, as we believe the Federal Reserve policy is now neutral to restrictive.

Investment Grade Fixed Income

The yield curve has inverted to levels last seen in the early 1980s. Historically, inverted yield curves are associated with approaching recessions which in turn lead to spread widening in credit markets. Investment grade fixed income markets reflect a slowing economic recovery. We continue to believe that cyclical inflation readings have peaked and that investment grade corporate bonds will become increasingly attractive over the next few quarters.

Tactical Fixed Income

We recently moved our tactical fixed income allocations to be more in-line with bond benchmarks as interest rates have risen. At the margin, we believe the inflation rate has peaked, and will ultimately settle in the 3%-4% range. As a result, we have rebalanced tactical fixed income positions back toward more traditional fixed income assets.

Core Equities

Since our last report, equity prices have declined due to higher interest rates, war uncertainty, and increased energy costs. After adjusting for recessionary recovery, we believe equities are fairly valued relative to historical valuations. Given recessionary risks and the inverted yield curve, we would not overweigh equities beyond investor risk determined allocations. Given our inflation and valuation outlook, we are also more constructive on small cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given economic volatility and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but real estate may suffer from higher interest rates until capitalization rates adjust. Gold appears to be regaining its status as a safe haven asset and cryptocurrency markets have been supported by favorable regulatory rulings recently.

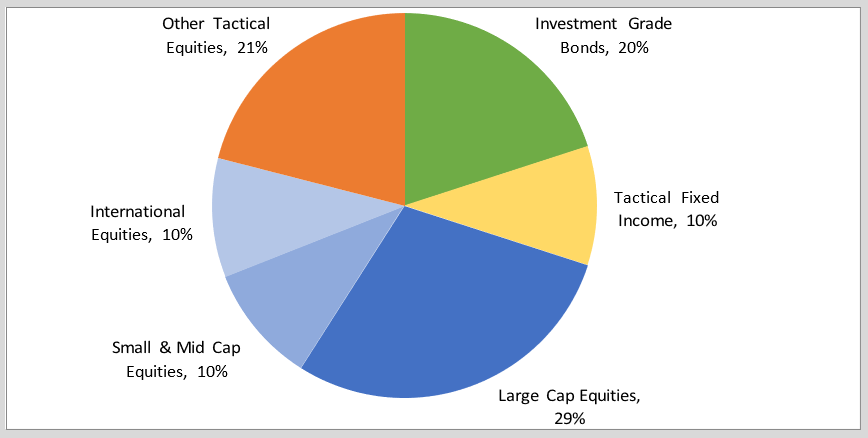

FinTrust Allocations (70/30 Risk Profile) with Tactical

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is a wholly owned registered investment advisory subsidiary of United Community Banks, Inc. that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Insurance and Benefits, Inc.. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.