Thank You For Being Late

Fourth Quarter 2022

Q: Allen, why title this WMQ “Thank You For Being Late?”

I decided to borrow this Wealth Management Quarterly title from Thomas Friedman’s book, Thank You For Being Late: An Optimist’s Guide to Thriving in the Age of Accelerations.

Friedman’s “field guide to the 21st century” addresses the stress technology’s exponential change creates in our world, our workplaces, our culture, our politics, our communities, our ethics, and ourselves.

Friedman starts his book by thanking a breakfast meeting for being late—the tardiness helped him slow down for a few minutes. It created a space for Friedman to think. He was grateful for the opportunity. Friedman later concludes, as summarized by the Financial Times, that “we can overcome the multiple stresses of an age of accelerations–if we slow down if we dare to be late and use the time to reimagine work, politics, and community.”

Today, when someone is late for a meeting, what do people do? Do they check their emails and text on the phone? Or do they converse with a stranger or the waiter or waitress? Or, do they ever sit quietly and think?

Friedman reminds us the “smartphone” is only 15 years old. Could you Uber to the meeting without a cell phone? Could you work remotely? Would politics be upset by a tweet? Could a political campaign be run from a basement? Would two-factor and three-factor authentication be possible and necessary for banking and work (something you know—password, something you have—phone authenticator, and something you are—fingerprint)? Previously, if someone was late, could you have sat quietly listening to all the world’s music available at a button push through Spotify?

Friedman concludes that by slowing down, we will be able to better handle and appreciate our changing world with a sense of optimism.

Allen Gillespie, CFA®, Managing Partner Investments

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Tightening. The Federal Reserve has been raising interest rates, and it intends to shrink its balance sheet.

- Fiscal Policy: Tightening. The CBO projects federal spending to flatline in 2023.

- Economic Vital Signs: Inflationary pressures while high, are starting to show signs of moderation.

- Yield Curve Watch: The yield curve is beginning to invert, which historically has preceded recessions by about 18 months.

Q: Allen, what prompted you to “slow down?”

I was traveling every week in October, to Alabama, to Denver, to Charleston, to Orlando, to Georgia, and back to Alabama. Unfortunately, it was then that my Windows software suffered a major failure—network overload, I guess. The malfunction wiped out the original version of the WMQ I had written.

I had not yet saved my draft on our cloud drive. I had saved it to my desktop for quicker access since I did not want to deal with Wi-Fi on planes and in rural hotels. It was a silly mistake. When you lose hours of work due to a computer’s failure, well, you also lose a little bit of yourself. You never get those hours back. Life and technology can make for a stressful, frustrating, and times wonderful co-existence.

My self-imposed deadline for writing each Wealth Management Quarterly is the second week of the quarter, so obviously, this WMQ is late. My hope, therefore, is that this tardy WMQ will create a mental space and time for our readers to think about the importance of time and time horizons in their lives and investing.

Q: How does time impact investing?

Time is an essential component of compounding. We all want instant results, but that is not how investing works. It takes time for companies to change prices, fix supply chains, hire competent workers, and earn money for investors, for investments to pay off. In investing, there are frequently J-Curves.

Q: Can you explain J-Curves to our readers?

A J-Curve is the economics term for the old saying, “it takes money to make money.” At the corporate level, a company first has to make a new capital investment in products, services, or people before it can have something to sell that will generate profits in the future. As a result, the profit trendline in a J-Curve shows an initial loss which is later followed by a dramatic gain. Obviously, not every investment, particularly in technology, works out. As a result, drawdowns during the J-Curve are a necessary part of the process, but they are also an uncomfortable time of uncertainty. In fact, stocks have historically spent about 95% of their time below their all-time high, and yet we all want stocks to stay right there near their peak all the time.

Q: What are other ways time impacts investing?

Investors recently have become aware of inflation again, as it has been hitting 40-year highs. Inflation erodes purchasing power with time. Inflation is a form of wealth taxation. Inflation, like its modern Metaverse counterpart, creates two worlds: it creates a nominally priced world that we see and transact in every day, and it creates a real price world defined by purchasing power—inflation creates a virtual reality in our modern language.

Q: What are the consequences of this inflationary virtual reality?

The first effect has been that the prices for “stuff” like cars, energy, and houses have increased. The increasing goods prices caused interest rates to rise because many of these goods require financing. In that regard, the Federal Reserve is following, not leading, the market. Today, US treasuries yield a little over 4%, up from below 2% not too long ago. While interest rates and stock prices change daily, it takes time for companies to reprice their goods and services. As a result, profit margins have been declining. The declining margins create concerns about the possibility of a recession.

Inflation creates a J-Curve profit margin pattern for many companies because the cost of goods sold initially increases as inventories are replaced. For example, you might be selling an old widget out of inventory that costs $10 to build, but the cost to build another widget might be $11. If you don’t move the price of your next widget up by more than $1, your profit margins will go down. Even if you do manage to raise your price by $1, your interest costs are higher, so your net income might still go down. In addition, maybe demand has softened, and it takes you longer to sell the next widget. The inflationary J-Curve is an uncomfortable time.

More immediately, higher interest rates increase the competition between bonds and stocks. Previously, many investors were happy to be in stocks that paid dividends because interest rates were below 2%. Now that investors can receive 4-5% in interest on bonds, investors are taking money out of stocks and placing it back into the bond markets.

“Inflation creates a virtual reality.”

Q&A with the Research Team

These combined effects — inflationary reduced profits and higher interest rates — pull investors towards sub-optimal decision-making in the inflationary metaverse.

Q: Can you please explain “sub-optimal decision-making in the inflationary metaverse” to our readers?

Absolutely. Inflation creates timing differences in asset class returns. The initial effects have profit margins, net income, and equities under pressure. The interest rates look like a sure thing, but remember, under an inflationary regime there is a “nominal price” and a “real price,” — which is the return after inflation. For example, the 12-month change in inflation in October was 7.75%. If you buy a bond paying, say, 4%, then you are making an investment, assuming that the average inflation rate over the life of the bond will be less than 4%. If it is not, then you will make 4% in nominal terms but lose purchasing

power in real terms. For example, let’s assume it is a 1-year bond. At the end of the year, you will have 4% more, but your purchasing power will have declined -3.75% if inflation stays at 7.75%.

Conversely, equities, because of the cost of goods sold effect we discussed earlier, might initially show a decline. Later, however, the equity might recover when the next widget is sold as profit margins are restored.

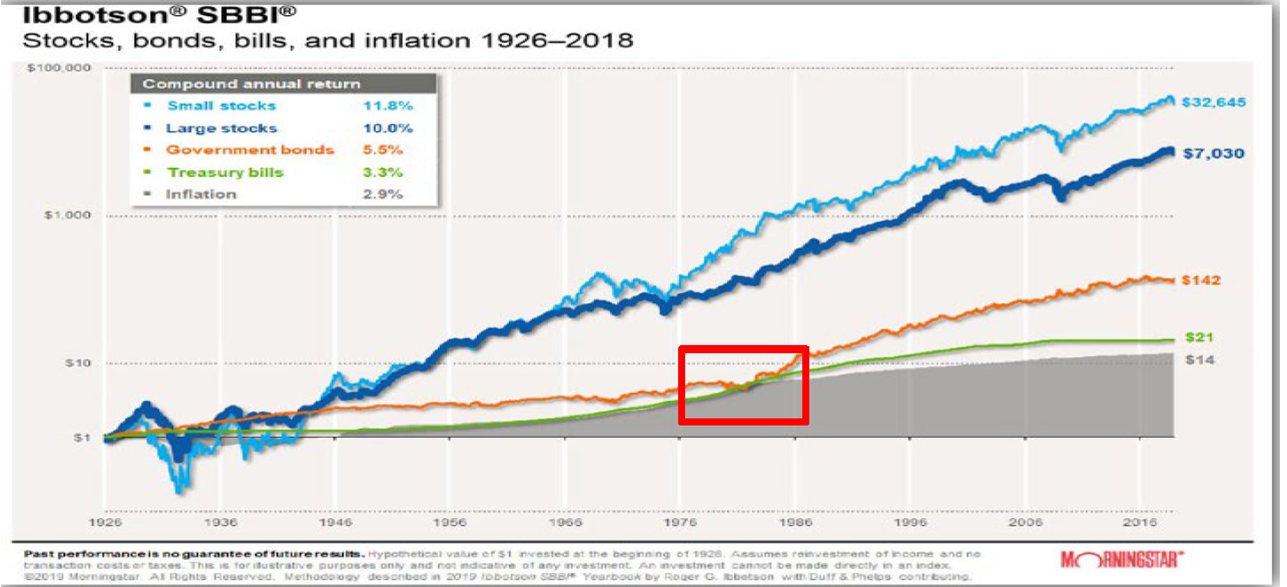

The historical chart above suggests that equities handle inflation better over time than other asset classes, but companies cannot instantly adjust to inflation. Over time, companies must pass through all their costs; otherwise, they will go out of business. If the companies go out of business, then the surviving companies consolidate their sales as a way to reduce costs, and the industry will recover.

Meanwhile, bonds also suffer for a time, but eventually, even bond investors demand compensation against inflationary risk. I have highlighted the period of the late 1970s in the

chart where bonds underperformed more cash-like investments for a period.

Q: What actions should investors be considering?

I think reviewing time horizons is critically important. Successful investors understand that there is a cycle, and the best investors invest through the cycle. They do not try to time the cycle because some cycles are short and some cycles are long. Some cycles are deep, and others are shallow. Successful investing and planning are about consistently doing the right things over long periods.

Q: What does this mean for investment expectations?

Since equities are the riskier asset class, they have historically offered higher returns than bond and cash. As a result, as the inflation rate declines—it would be reasonable to assume that

equities will return to a “real return” status sooner than bonds and cash. In recessions, bonds typically bottom before stocks, but I believe that in a high inflationary environment, equities might stabilize before bonds because they will begin to offer real rates of return sooner. The inflationary illusion is leading investors to seek the safety of “cash,” but I actually think equities might turn out to be the better inflationary hedge here

Any final thoughts?

Inflation forces you either into immediate consumption before your money loses value, or it forces you to invest in the future and accept J-Curves to protect its value.

For retirement savers, my final thoughts then would be this: Don’t waste time—use some of your money and time on things important to you—also, keep investing through the inflationary J-Curve to allow compounding to work for you. Thank you for allowing me to be late.

Sincerely,

Allen R. Gillespie

QUICK TAKE MAJOR ASSET CLASSES

Cash and Cash Equivalents

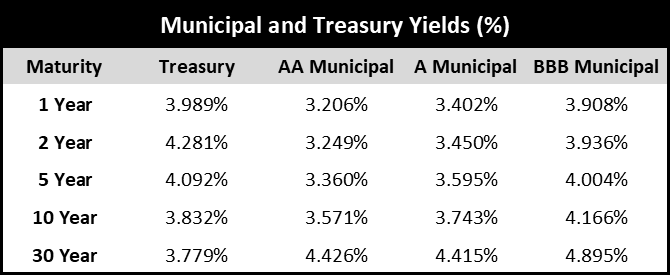

The Federal Reserve raised short-term rates in 2022 to the point where short-term interest rates now exceed long-term realized inflation measures. The 10-year realized inflation rate now sits at 2.41%. As a result, we now believe short-term bonds can be utilized for conservative investors.

Investment Grade Fixed Income

The yield curve has begun to invert past the 1-year mark. Investment grade fixed income markets reflect a slowing economic recovery, so we would expect credit spreads to gradually begin to widen. The 10-year treasury yield is once again above the 10-year realized inflation rate, but inflation readings have been coming in hot. We believe these inflation readings peaked in the second quarter and that investment-grade corporate bonds now offer reasonable yields for the environment.

Tactical Fixed Income

Historically, fixed-income and equity arbitrage strategies earn a risk premium above cash yields. Given that equity market neutral strategies historically are positively correlated to higher short-term interest rates., At the margin, we believe inflation has peaked, so we think rebalancing tactical fixed income back toward more tradition fixed income assets is appropriate.

Core Equities

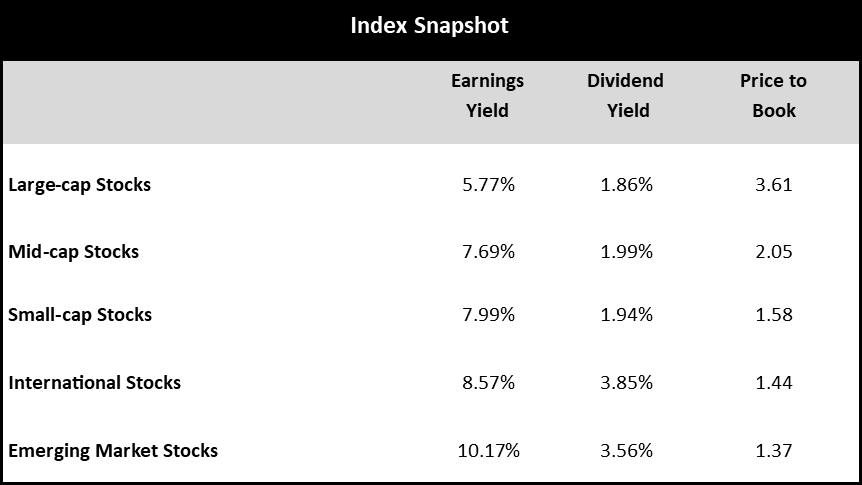

Since our last report, equity prices have recovered somewhat, as both interest rates and energy prices seem to have peaked during the second quarter. After adjusting for the recessionary recovery, we believe equities are fairly valued relative to historical valuations. Given high levels of volatility, we would not overweigh equities beyond investor risk-determined allocations. Given our inflation outlook, we are also more constructive on small-cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given economic volatility and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds.

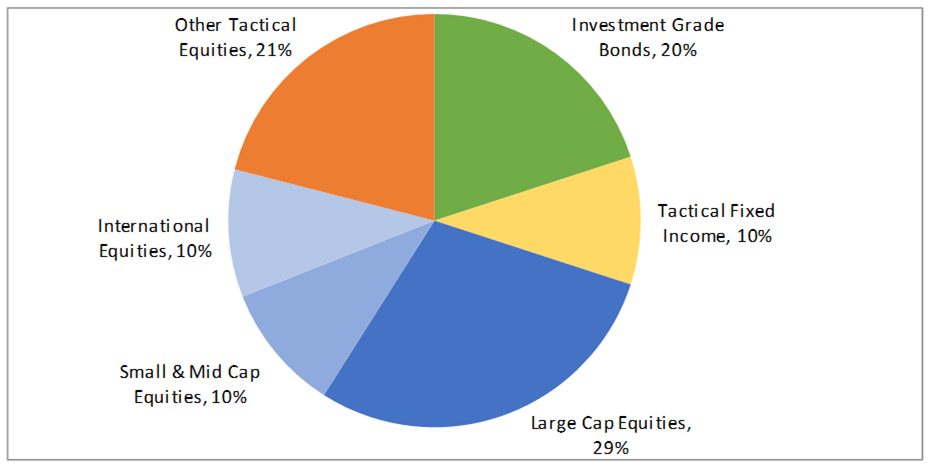

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 9/30/2022. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is a wholly-owned registered investment advisory subsidiary of United Community Banks, Inc. that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.