Attention & Distraction Markets

Third Quarter 2022

Q: Allen, why title this WMQ “The Culture of Attention & Distraction Markets?”

Each of us intuitively understands that time has value, but we rarely pause to think about the economics of it. Since none of us knows how much time we have, we should endeavor to use our time intentionally. Unfortunately, the marketplace for our attention does not care about our intention. As a result, I believe attention markets are critically important to understand. Beyond the impact on our individual lives, the hypergrowth of the attention and distraction markets has severely impacted the culture and lowered the degree of trust in institutions. This creates both risks and opportunities for investors.

Q: What are “attention markets?”

Attention markets are the marketplace for our attention. In the private sector, the attention market involves competition for our time, which is a scarce and valuable resource, to sell ad space. In the public sector, the goal is not to sell a product but to either garner support or distract us—depending on the situation.

Q: What are the economics of attention markets?

According to Statista, attention markets for online advertisers reached $360 billion in 2020. Importantly, online advertisers have learned that it only takes 3 seconds to increase the probability of making a sale by 50%. Emotional responses further increase the probability of a sale. Think about that—your attention and your emotions are being sold in 3 seconds increments.

Q: How are attention markets impacting culture?

At the core, attention markets segment, fragment, customize, and emotionally amplify information to create a response. A recent example of increasing market fragmentation would be television consumption. In television, there were initially just a handful of major channels and news shows, so people could easily have “water cooler” conversations. In fact, even as late as my college days in the early 1990s, groups of friends would gather around a single tv to watch “must-see tv” on Thursday nights—NBC’s lineup of Seinfield, Friends, Frazier, and ER. Now, significant others can be in the same bed but watch completely different shows on individual electronic devices—side by side yet worlds apart—she likes British period pieces while I like sports. In that regard, the market for television content doubled because couples are watching different shows at the same time.

Television watching habits are a relatively benign example. While the customization of information enables hyper-personalization, it breaks down the shared experiences.

Allen Gillespie, CFA®, Managing Partner Investments

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Tightening. The Federal Reserve has been raising interest rates and it intends to shrink its balance sheet.

- Fiscal Policy: Accommodative. The Democrats intend to make one more budget push before the mid-term elections.

- Economic Vital Signs: Energy prices are reaching levels associated with past economic slow-downs but have recently eased.

- Yield Curve Watch: The yield curve is beginning to invert, which historically has preceded recessions by about 18 months.

When mass fragmentation and emotional amplification are applied to more serious issues, they combine to lower the degree of common knowledge and increase the emotional intensity of society. A natural counter-response to the manufactured emotion becomes skepticism, outrage, and cynicism. These emotional responses move us toward the zero-trust world we discussed in our last WMQ.

Q: Can you give us an example of the opportunities, risks, and challenges attention markets create?

The opportunities come from the hypergrowth of niche markets. Returning to our television example, just think about the explosion in content. The risks come with the breakdown in larger systems, industries, and companies, like major beer brands losing market share to thousands of craft breweries. Anheuser Busch, for example, makes less money than it did 8 years ago, so recently it has begun buying up craft breweries.

The breakdown effects become more serious when applied to the government. In government, across the globe, there is a real battle raging between those that seek greater control and centralization under the UN’s 2030 Agenda and those that seek a freer, or at least, more locally controlled world. In that regard, this post-internet period has many similarities to the post-Gutenberg press era.

Q: Can you expand on those similarities?

Prior to the development of the printing press, books were relatively expensive, slow to be produced, and a limited number of people had access to the information. After the development of the printing press, the cost of books declined, production speeds increased, and popular books and pamphlets would be shared. Information was democratized.

In Western society, Erasmus’s work was reprinted an estimated 750,000 times, and the King James Bible became one of the most widely printed and read books. Whether someone agreed with it or not, there was common knowledge of its contents. You would think this would put everyone on the “same page” so to speak, but in fact, it led to the exact opposite effect.

The amplification of the emotional responses to the Bible, in time, led to both political and religious conflicts and wars. I can assure you that Martin Luther’s Theses were not just pinned to the door. How did the church authorities respond—he was excommunicated of course because they didn’t like what he had to say—just as Twitter bans and YouTube takedowns are becoming common. Ultimately, there were both civil, international, and cultural wars that were fought across all aspects of the culture including business. Before too long, there were not just Protestants and Catholics, but Anglicans, Baptists, and new countries emerging.

I find it interesting to consider that the internet’s most successful company, Amazon, began as a bookseller in 1994.

Q: Are there similarities between attention markets and financial markets?

In financial markets, quickly changing prices (up or down), high prices, and low prices all serve to capture investor attention. Financial markets then leverage these prices to create emotional responses from investors to produce action.

On Wall Street, an emotional response increases the probability of an investor “sell” when prices are low, and a “sold” to you when auction prices are high. Financial markets constantly advertise prices not values, just as attention markets communicate both noise and information.

Q: Beyond “selling” and “buying” at the wrong time, how do attention markets impact investors?

Remember, our attention can get distracted in as little as 3 seconds, particularly when we have an emotional response. In those 3 seconds, we may forget long-term planning intentions.

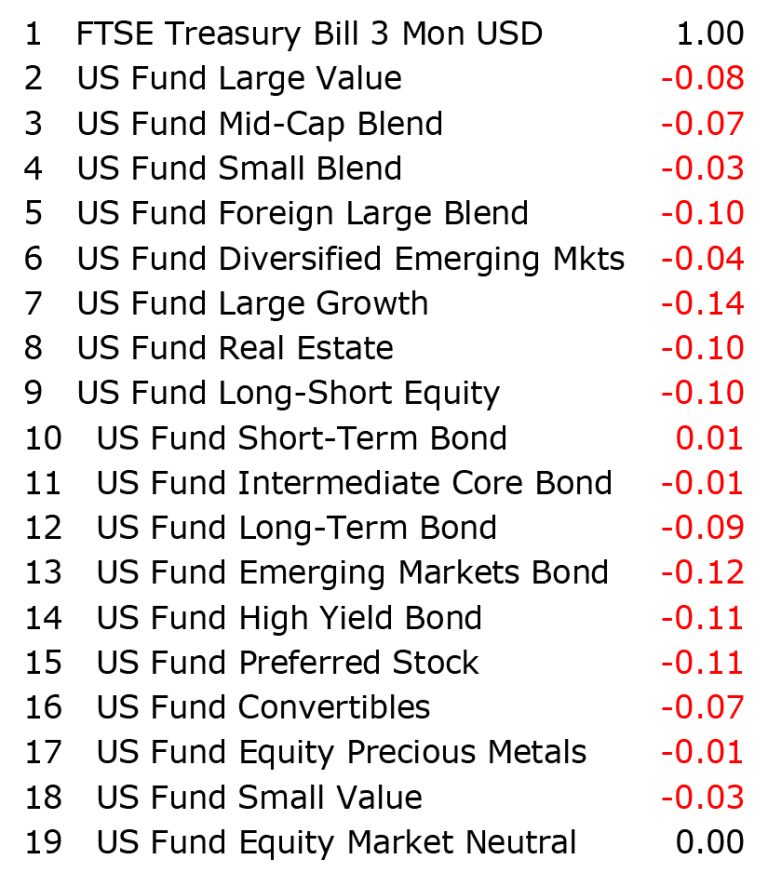

Average Correlation to Short-Rates

As of 6/30/2022

“On Wall Street, an emotional response increases the probability of a “sell” when prices are low, and a “sold” to you when auction prices are high.”

In financial planning and investing, time horizons and the time value of money are among the most important variables. Yet, many investors fail to think very deeply about them. Diversified portfolios frequently confuse the issue because they hold assets that have fundamentally different time horizons.

For example, let’s take an investor that has a portfolio of 50% bonds and 50% stocks. The bonds may have a 4-year average life but the time horizon for the stocks might be 12 years. In this case, the weighted average life for the portfolio would be eight years. The investor then might start to worry when markets are down over shorter time horizons. The emotional response then gets amplified when the investor starts looking at monthly statements and quarterly performance reports. The real-time horizon over which the investor should be thinking, however, is eight years in our hypothetical portfolio.

In that regard, I think the current market is a particularly dangerous market for investor decision-making.

Q: Why is the current market environment dangerous for investor decision-making?

I think the current market is challenging because what hurts in the short run actually helps in the long run. It’s like when my wife takes the ice cream away and says, “you don’t need that.” The Federal Reserve is saying to markets you don’t need too much monetary sugar.

Historically, the returns on long-duration assets like stocks, bonds, cryptocurrencies, and real estate are negatively correlated to increases in short-term interest rates (see table on the previous page). At the same time, long-duration asset returns are positively related to increases in long-term interest rates.

For example, if one bought a long-term treasury bond two years ago the interest rate was 0.73%, but now that same bond yields something close to 3%. Just two years ago a $10,000 bond investment would grow to a minuscule $10,754 dollars in 10 years, but today an eight-year investment (10 years minus the 2 that have passed) will grow to $12,667 dollars. Today’s market prices present more value to investors.

Another example can be found in today’s high energy prices. High energy prices hurt consumer spending and frequently precede a recession. High prices, however, also encourage increases in production which bring prices back down. The difficulty in the current market is that authorities currently want to encourage a mass movement toward renewable energy, but renewables do not yet have the capacity to deliver what the market needs, so the adjustment is taking longer. As a result, the Green New Deal policies are creating an energy squeeze. In time though, the market will sort things out.

Q: How can we align our attention and time horizons to become better investors and decision-makers?

I recently read about the 10-10-10 rule, which I think is a good approach to decision-making and investing.

The 10-10-10 rule encourages you to think about your emotional responses to a decision over three different time horizons (i.e., 10 minutes, 10 months, or 10 years) before making a decision. The longer the time horizon over which a decision will impact you, the longer you should think about the decision.

This is how financial markets get people to make mistakes—because you can instantly trade stock on your phone, you can quickly change your mind, so it does not feel like a big decision — in reality though, we should be carefully considering what businesses we want to own 10 years from now.

Financial markets are very good at stealing attention and amplifying emotions by pulling attention to current events and earnings. A better way to make financial decisions, however, is to stay focused on a long-term plan and investment time horizon.

Q: How would you apply the 10-10-10 rule apply to the current market environment?

Federal Reserve tightening cycles and recessionary periods typically last 10-21 months, so they are in the second 10 of the 10-10-10 sequence time horizon bucket. When you are financial planning for retirement, however, you might be saving and investing for decades, so you are thinking in the third bucket. On top of that, the average retirement now lasts 19 years, so even when you are retired you still need to consider a longer time horizon for a good portion of your money, like that third bucket.

Q: Any final thoughts?

Attention markets are designed to operate in shorter time horizons and amplify emotions—so longer-term thinking is critical. When we are aware of the techniques companies, governments, and markets use to steal our attention, then we can be of better service to ourselves and our communities.

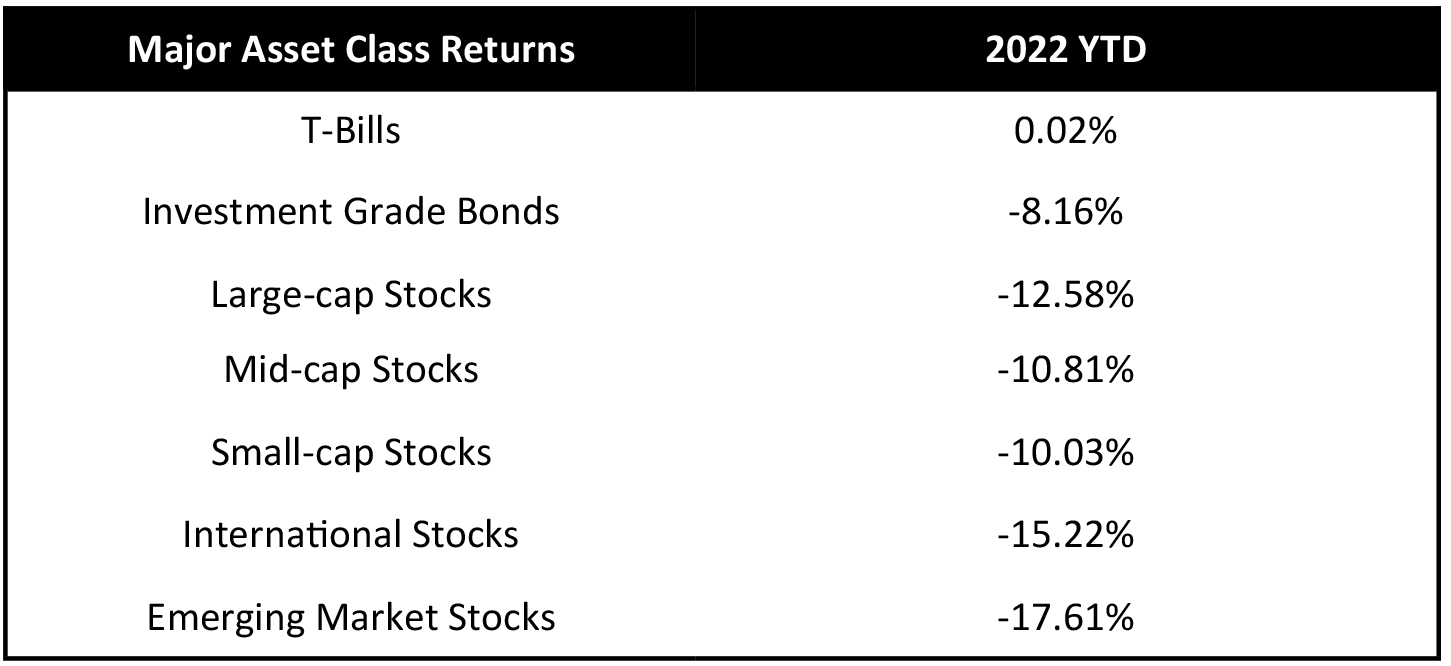

QUICK TAKE MAJOR ASSET CLASSES

Cash and Cash Equivalents

The Federal Reserve raised short term rates in 2022 to the point where short-term interest rates now exceed long-term realized inflation measures. The 10-year realized inflation rate now sits at 2.29%. As a result, we now believe short-term bonds can be utilized for conservative investors.

Investment Grade Fixed Income

The yield curve has begun the year with a sharp move higher but longer-term yields are beginning to invert. Investment grade fixed income markets reflect a slowing economic recovery, so we would expect credit spreads to gradually widen. The 10-year treasury yield is once again equal to the 10-year realized inflation rate, but inflation readings have been coming in hot. We believe these inflation readings will peak in the second quarter and that investment-grade corporate bonds now offer reasonable yields for the environment.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given that equity market-neutral strategies historically are positively correlated to higher interest rates, we continue to favor these types of strategies. At the margin, however, since we believe inflation has peaked we think rebalancing tactical fixed income back toward more tradition fixed income assets is appropriate.

Core Equities

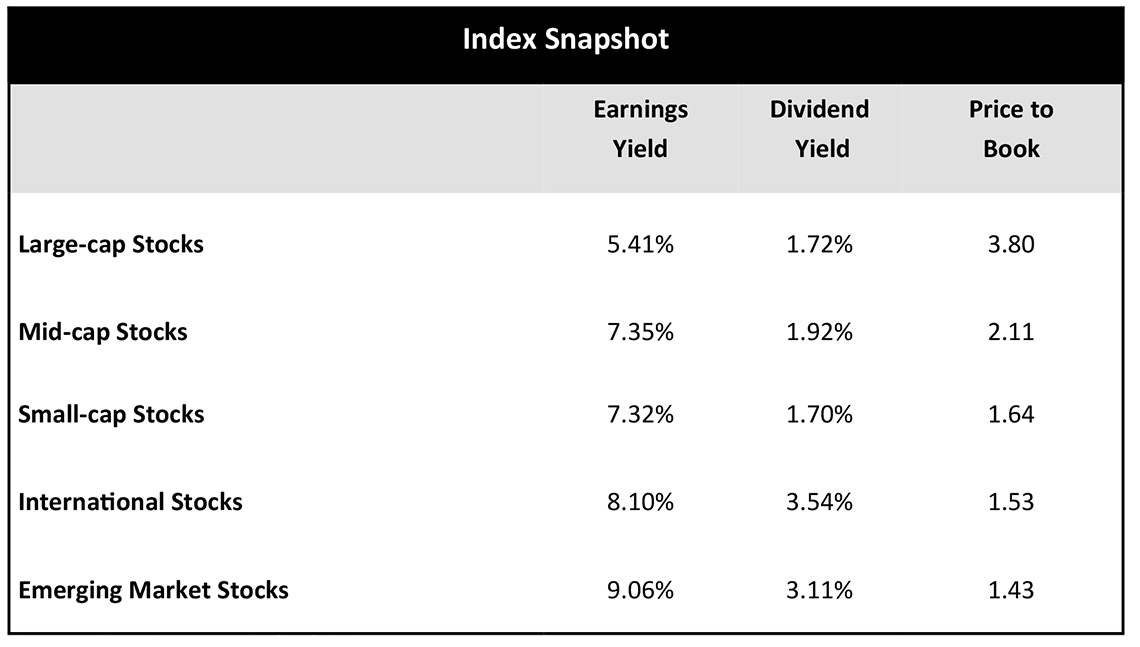

Since our last report, equity prices have recovered somewhat as both interest rates and energy prices seem to have peaked during the second quarter. After adjusting for recessionary recovery, we believe equities are fairly valued relative to historical valuations. Given high levels of volatility, we would not overweigh equities beyond investor risk determined allocations. Given our inflation outlook, we are also more constructive on small-cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given economic volatility and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds.

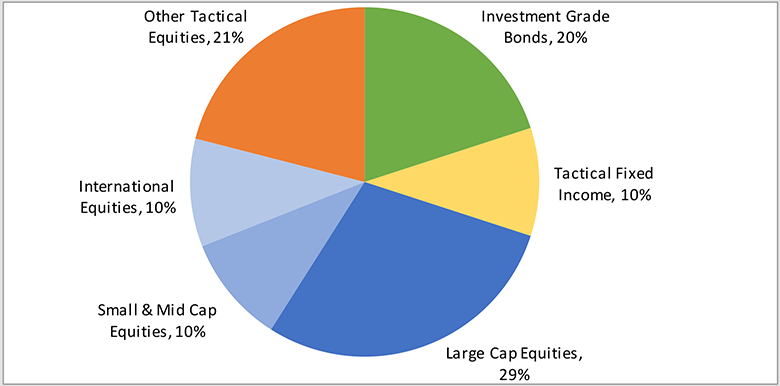

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 6/30/2022. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is

unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets

not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments

to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and

other factors.

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is a wholly-owned registered investment advisory subsidiary of United Community Banks, Inc. that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.