Q1 2024: Exponential Biology & Eternal Punishment

Q: Allen, why title this WMQ “Exponential Biology & Eternal Punishments?”

As an investment advisory and strategic financial planning firm, FinTrust provides retirement advice as a core service. Retirement planning involves modeling financial resources to help clients balance how much to spend today (quality living) without running out of money in the future (quantity living). Life expectancy calculations therefore drive a lot of our work, so we pay special attention to longevity research.

People realize that we are living longer lives today than in the past, but we may be underestimating how much longer. In a personal example, my wife’s grandmother is now 99. FinTrust’s base life expectancy assumption is that clients will live well into their 90s, unless health indicators suggest using something shorter. The life expectancies we use, however, are before what many thought leaders now believe: we are on the doorstep to exponential improvements in our biology.

Demographers, technologists, biologists, investors and government statisticians study longevity because these calculations have implications beyond retirement planning and our individual lives. Exponential improvements in biology would create both risks and opportunities for many industries and government spending programs. Longevity assumptions therefore are a common and unspoken subtext in many of the most important and contentious issues in economics, politics, technology, and healthcare today. Stanford University Center of Longevity’s website succinctly states the issue this way, “Century-long lives are here” and “We’re not ready.”

I therefore decided to title this WMQ Exponential Biology & Eternal Punishment as we examine how longevity is viewed by today’s leading futurists, how it is portrayed in the ancient wisdom literature, and what longevity means for markets, investors, and retirement planning going forward.

Allen Gillespie, CFA®, Chief Investment Officer

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis, CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Neutral. The Federal Reserve has kept short-term rates high, but this has led to declines on the long end of the yield curve.

- Fiscal Policy: Inflationary. The CBO projects federal budget deficits to average 5.5 percent for the next ten years.

- Economic Vital Signs: Inflationary pressures have moderated. Oil prices have returned to average levels on an inflation adjusted basis.

- Yield Curve Watch: The yield curve continues to be inverted. Fed funds futures currently imply the first Federal Reserve rate cut will occur between March and May 2024.

Q: How do leading futurists view longevity?

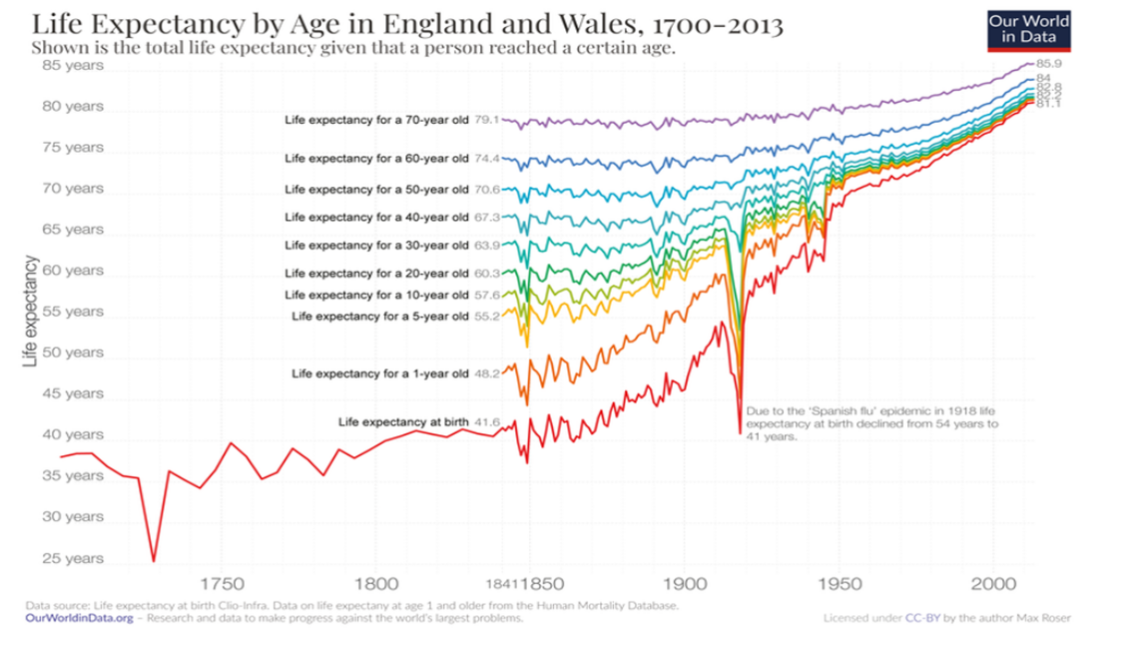

Over the last 175 years, life expectancy from birth has roughly doubled. The biggest improvements have come from a reduction in infant and female mortalities associated with childbirth. Improvements from the age of 40, however, have only been about 22%. Futurists view these gains as painfully slow and inadequate.

If you read and listen to certain futurists, and watch where venture capitalists are investing, you might conclude that they believe in transhumanism and that the “singularity” approaches. For example, Google Futurist Ray Kurzweil’s books include the following: The Singularity Is Near: When Humans Transcend Biology, Transcend (2005), Nine Steps to Living Well Forever (2009), and The Singularity is Nearer (2024).

Q: What is the “singularity”?

In technology, the “singularity” refers to the point at which artificial intelligence (“AI”) not only surpasses human intelligence, but that it develops the ability to advance itself. Importantly, at the singularity, technologists believe humans will merge biologically with our machines. Once we merge with our machines, we will become “transhuman.” Transhumans are anticipated to be an entirely different species from our homo sapien selves. During a recent interview with Lex Fridman, Jeff Bezos noted simply that historically, “our tools change us.” This is true whether the tools are stone, bronze, iron, gunpowder, or computers.

Q: What are the central beliefs of transhumanism?

The core idea behind transhumanism is to transcend the limitations of the human body and mind, through the use of technologies and knowledge, to achieve a post-human state. Transhumanism supports the use of science and technology to improve human performance, health, and lifespan. This includes genetic engineering, cybernetic implants, brain-computer interfaces, regenerative medicine, and cryonics. A significant focus of the transhumanism movement is on technologies that could extend human lifespans indefinitely, potentially even achieving a form of immortality. This immortality, of sorts, would be achieved by the transhumanists through the recording of everything we see, hear, or sense through cameras, microphones, and biological nanomaterial sensors that log everything into an AI database. Most of us understand and can see the cameras and microphones going up around us, but to fully understand the transhumanist’s world, one must spend time in patent filings and journals like the Journal of Nanobiotechnology.

Q: Can you expand on the merging of biology and technology?

Futurists think about human biology in terms of hardware, software, memory, and systems like power and electricity. For example, our physical bodies are viewed as hardware that can be replaced like motherboards. We have already come to terms with the physical hardware upgrades. People regularly go for pacemakers, knee, and hip replacements.

The question now before us relates to software upgrades. First, would you do it? Second, who gets to control it? Would you be comfortable with centrally controlled pacemakers or brain implants? These are important questions for which we are going to need to answer.

Q: How close are we to these technologies?

Neuralink is currently enrolling additional people for human trials for its brain-computer interface. Just this month, Elon Musk announced on X that Neuralink has implanted a device in its first human. It is easy to imagine some of the first use cases, Stephen Hawking being a famous example. Soldiers with PTSD are another area of focus for the computer chip implant researchers. They are working to reprogram the mind after traumatic experiences. We understand these use cases, but are we moving toward a generalized use of lobotomies through computer chips? These technologies raise important moral and ethical questions.

Incidentally, ancient thinkers had very different views regarding longevity and technology transfer than today’s tech leaders.

Q: How did the ancients view longevity and tech transfer?

In Greek myths and religious traditions, living forever was generally reserved for those sentenced to eternal punishment for giving mankind something the gods did not want men to have. For example, the Greeks provide us with the story of the goddess Eos. She falls in love with the beautiful Tithonus and wishes that he might live forever. Zeus grants her wish, so Tithonus receives immortality, but not eternal youth. He must constantly age which becomes problematic.

Another Greek myth is that of Asclepius, a physician who mastered the ability to bring people back to life. Since he broke the natural order, Zeus struck him down with a lightening bolt. He died suddenly rather than from old age.

Sisyphus also cheated death twice. When he was recaptured, he was sentenced to roll the same rock, up the same hill, only to watch it roll back down repeatedly for eternity. Biomedically, Prometheus gave humans the technology of fire which he stole from the Olympic gods. For his punishment, he was sentenced to have a liver that would regenerate nightly. He then would have to endure the pain of having it eaten out by an eagle every day.

Q: What does increased longevity mean for investors?

At an individual level, clearly it means we need to save more.

We need to be prepared to invest for longer periods of time. It also means that we need to maintain a long-term mindset when investing, even while in retirement. Investing with a long-term frame of mind can become increasingly difficult for people when they perceive that their time horizon is shrinking and markets are acting volatile.

Longevity and the large Baby Boomer demographic also means we are going to see immense pressure on the Federal deficit for the foreseeable future. The Congressional Budget office is expecting deficits to be between 5% and 10% for the next decade, as the cost of benefit programs like Medicare escalate. I believe these deficits will create upward pressure on inflation and interest rates.

When looking toward investments, longevity clearly drives a lot of medical research. Compared to software companies though, biotechnology companies are tougher to understand, as they carry a much wider range of outcomes. I think this has always held back the public’s enthusiasm for investing in the space. I think, however, the industry is going to be a great place for growth focused investors to allocate capital going forward.

On the risk side, I think longevity creates two competing political camps and views of the future. One line of thinking is a direct extension of Malthusian thinking. It holds that we are resource constrained and at risk of overpopulation, so we should promote policies which limit or even reverse population growth. The competing camp believes we are going to need people and longevity to achieve the great deeds of the future like long distance space travel.

Q: Allen, any final thoughts on Exponential Biology and Eternal Punishments?

I recently read that as we age, fitness can be measured across five factors: flexibility, balance, endurance, strength, and mental health. The Hartford in conjunction with MIT Age Labs just published a nice brief on 10 things to keep our brains healthy as we age. I think these areas of focus are not only good advice for health, but good advice for retirement portfolios.

Diversified portfolios are designed for long-term endurance through risk control. In contrast, concentrated portfolios are made for quick sprints. Unfortunately, market indices have now become taken on concentrated portfolio characteristics.

Rebalancing portfolios, like stretching, is also an important activity because it brings investments back into long-term policy alignment. Portfolios, however, need some flexibility because financial markets, financial products, industries, and companies change.

In health, strength comes from resistance training, rest and recovery. In financial markets, strength is built by resisting short-term emotional thinking during periods of market euphoria and depression. I have learned over my career that the market, at times, needs its own brain chip.

Sincerely,

Allen R. Gillespie

QUICK TAKE

MAJOR ASSET CLASSES

Cash and Cash Equivalents

According to the CBO, the Federal deficit as a percentage of GDP is 5.5%, so short-term interest rates are in line with inflationary spending levels. Cyclically, inflation measures are well below short-term interest rates, so the market has begun to price in interest rates cuts. We believe the Federal Reserve policy is now neutral to restrictive, so allocation to short-term cash and cash equivalents may produce competitive returns.

Investment Grade Fixed Income

The yield curve has inverted to levels last seen in the early 1980s. We are expecting the yield curve to return to a normal shape during 2024. The normalization of the yield curve will likely create some short-term pressures on investment grade fixed income markets, but we believe core bonds reasonably reflect both recessionary and inflationary pressures. As a result, we believe tactically rebalancing within the space will be increasingly attractive over the next few quarters.

Tactical Fixed Income

Tactical fixed income sectors are beginning to exhibit some spread widening behavior. While we moved our tactical fixed income allocations to be more in-line with bond benchmarks, at the margin, we believe investors should begin to extend credit risk over the next few quarters.

Core Equities

Given recessionary risks and the inverted yield curve, we would not overweigh equities beyond investor risk determined allocations. We believe a normalization of the yield curve will temporarily impact long-term growth assets. Given our inflation and valuation outlook, we are also more constructive on small cap, value, growth at a reasonable price, and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given economic volatility and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios. We believe commercial real estate in major metro markets may see pockets of distress due to shifts in product and populations. Gold appears to be regaining its status as a safe haven asset and cryptocurrency markets have been supported by favorable regulatory rulings recently.

Index Snapshot

| Earnings Yield | Dividend Yield | Price to Book | |

|---|---|---|---|

| Large-cap Stocks | 4.64% | 1.50% | 4.48 |

| Mid-cap Stocks | 6.27% | 1.65% | 2.39 |

| Small-cap Stocks | 6.85% | 1.86% | 1.86 |

| International Stocks | 7.82% | 3.40% | 1.60 |

| Emerging Market Stocks | 6.84% | 2.62% | 1.61 |

| Source: Bloomberg as of 12/31/2023 | |||

| Major Asset Class Returns | 2023 YTD |

|---|---|

| T-Bills | 5.11% |

| Investment Grade Bonds | 5.53% |

| Large-cap Stocks | 26.29% |

| Mid-cap Stocks | 16.44% |

| Small-cap Stocks | 16.05% |

| International Stocks | 18.85% |

| Emerging Market Stocks | 10.27% |

| Source: Morningstar Direct, As of 12/31/2023 | |

Municipal and Treasury Yields (%)

| Maturity | Treasury | AA Municipal | A Municipal | BBB Municipal |

|---|---|---|---|---|

| 1 Year | 4.773% | 2.749% | 3.083% | 4.232% |

| 2 Year | 4.251% | 2.651% | 2.991% | 4.198% |

| 5 Year | 3.848% | 2.369% | 2.721% | 4.188% |

| 10 Year | 3.880% | 2.466% | 2.901% | 4.426% |

| 30 Year | 4.029% | 3.779% | 4.217% | 5.423% |

| Source: Bloomberg as of 12/31/2023 | ||||

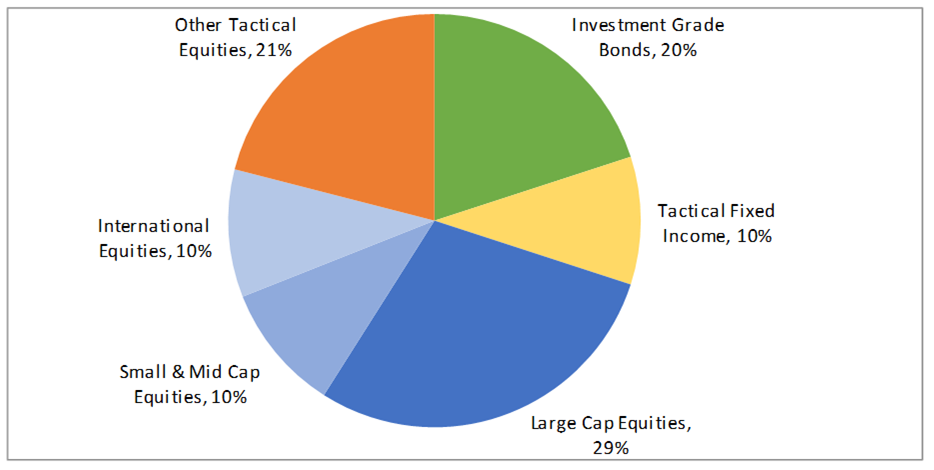

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 12/31/2023. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limited to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is a wholly owned registered investment advisory subsidiary of United Community Banks, Inc. that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Insurance and Benefits, Inc.. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.