Q3 2021: Variant Perception

Q: Allen, why title this quarter’s WMQ Variant Perception?

One of Wall Street’s most legendary portfolio managers was a hedge fund manager by the name of Michael Steinhardt. Over the 28 years of his partnership (1967-1995), Steinhardt compounded capital at 24% net of fees. A $10,000 investment in Steinhardt Partners became more than $4.6 million, while a similar investment in the S&P 500 became $190,000. In his book, “No Bull,“ and when interviewed regarding his investment philosophy and process, he stated it simply as “variant perception.”

Given that markets, politics, and policies are currently all about Covid, vaccines, and the “delta variant,” it seemed timely to discuss the importance of variant perceptions to successful investing.

Q: Is investing based on variant perceptions just about being a contrarian?

Steinhardt does a great job illustrating the difference between a contrarian view and a variant view. A contrarian is always, and automatically, against the consensus view. As Steinhardt explains, “being a contrarian is a plus, but it’s not enough….you have to be right. To be a contrarian is easy, but to be contrarian and to be right in your judgment when the consensus is wrong is where you get the golden ring, and it doesn’t happen that much, but when it does happen you make extraordinary amounts of money.”

Therefore, as Steinhardt explains, in order to develop a variant perception, one must first understand the consensus view by “becoming sufficiently knowledgeable about whatever the subject is” and then to have a reason to be willing to take a stance at variance from that consensus.

Q: In financial markets, are there any current consensus views that may be wrong?

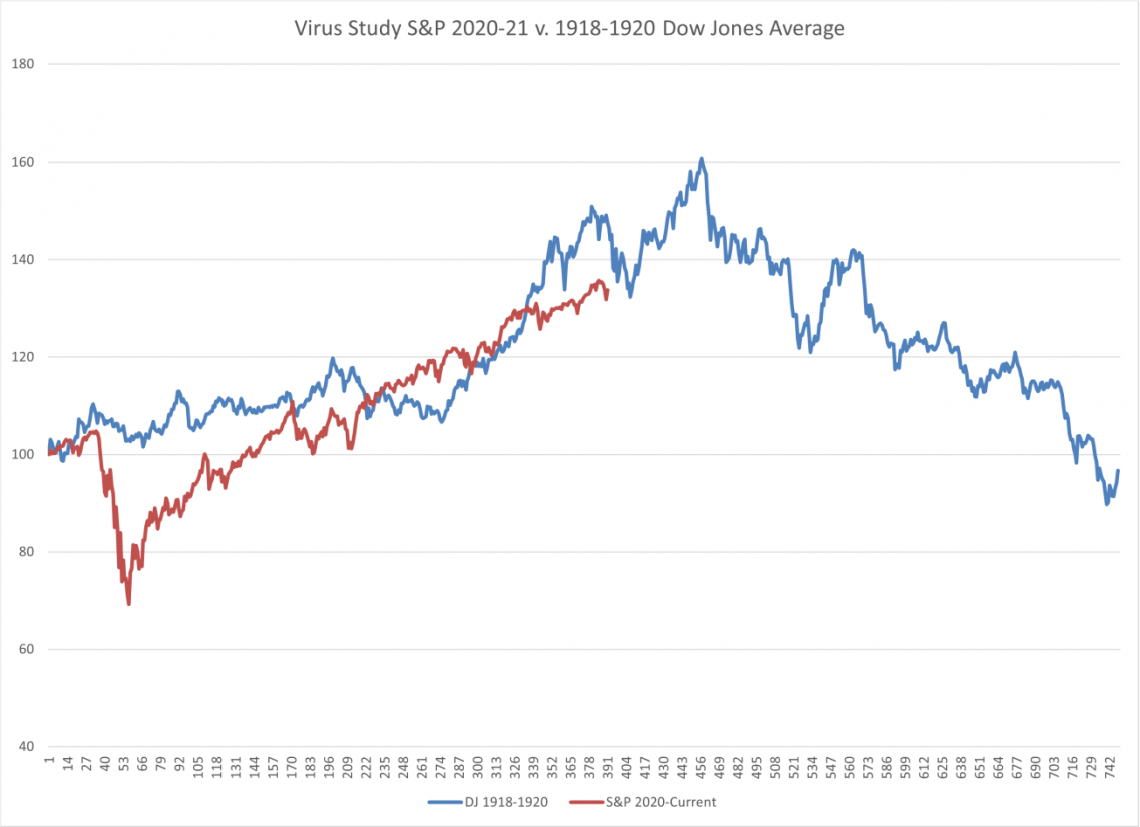

Great question. First, I think that market participants are allowing the short-term news flows around Covid, its variants, and vaccination rates to drive too much thinking. During the latest quarter, people have been selling off recovery stocks and buying the shutdown stocks and governments are getting more aggressive about vaccinations. Economically, however, we are seeing global recoveries both in places where vaccination rates are high, like the US and Israel, and in economies like Sweden which have taken a different approach toward reaching herd immunity. I think the market is saying natural immunity is a viable Covid solution, though obviously more impactful on at-risk populations. Interestingly, the equity markets continue to track the 1918 Spanish flu pattern quite closely regardless of government policies.

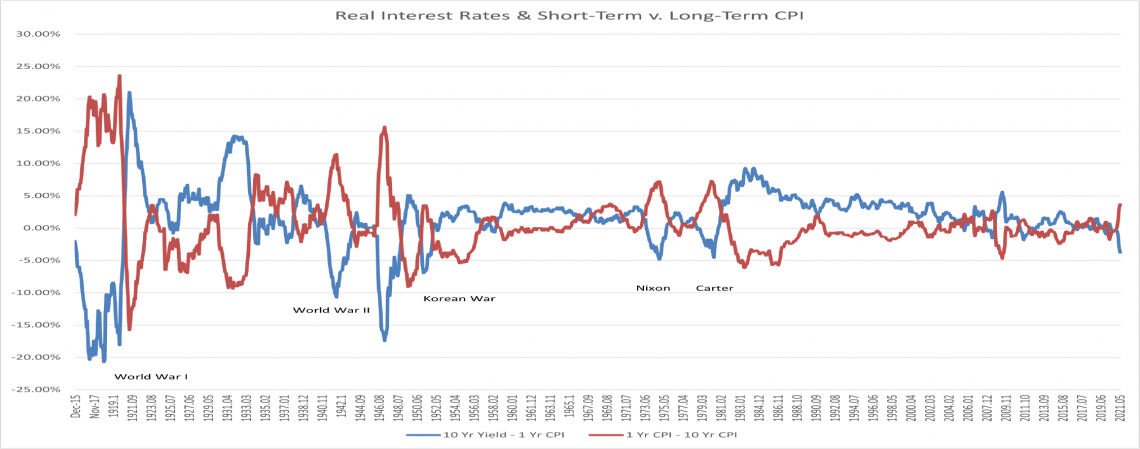

The biggest consensus view that I believe is wrong can be seen in the bond market. At the end of June, the 10-year government bond yielded 1.52%, while the 10-year realized inflation rate was 1.63%, as measured by the consumer price index. This implies that the market will continue to expect low inflation over the next decade. However, over the past year, the CPI is up 5.32%, so on that measure, the real interest rate for a 10-year government bond is currently a negative (-3.80%), so bond investors have already lost 3 years of interest.

If you track all the interest rate data from the Federal Reserve back to its inception, you’ll only find 5 periods with this type of set-up. They are World War I, World War II, the Korean War, and the presidencies of Richard Nixon and Jimmy Carter.

So, the consensus view in the bond market is that inflation is transitory and that the Federal Reserve is capable of maintaining its stranglehold on interest rates.

Allen Gillespie, CFA®, Managing Partner Investments

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

Monetary Policy: Accommodative. The Federal Reserve has massively expanded its balance sheet and interest rates remain low.

Fiscal Policy: Accommodative. With Democrats controlling both the White House and Congress, expectations are high for additional rounds of stimulus.

Economic Vital Signs: high debt to GDP, low money velocity, high money supply growth, high anxiety, positive millennial demographics ahead.

Yield Curve Watch: The yield curve remains positively sloped though very low on the front end of the curve, indicating a weak recovery.

Q: Do you have a variant perception of transitory inflation and Fed control?

The simplest variant perception in bonds would be that the inflation is not transitory, the Fed will lose control, and interest rates will rise. I believe the difference in the market consensus and market data exists because there are very few portfolio managers, including myself, who are old enough to remember the inflation of the 1970s, much less the Korean or World War experiences. Let’s look at each of the time periods. Most recently, during the Nixon and Carter episodes, the Fed lost control of gold, energy, and commodities. Additionally, commodity-related stocks exploded higher while bonds cratered. During the war periods, stocks did okay, but they had plenty of ups and downs. There were also many goods shortages, but interest rates and bond prices were relatively tame because of the central bank.

“There are very few portfolio managers, including myself, who are old enough to remember the inflation of the 1970s.”

Therefore, a more complex variant perception, is that the inflation is not transitory because there is a currency crisis brewing. The Fed will continue to control nominal prices but not real or inflation-adjusted prices.

We can already see that hyperinflationary effect in markets. Cryptocurrencies are going up the fastest, followed by stocks. Commodities are being to shoot higher, meanwhile, bond prices are stable.

Historically, I think the situation we are facing is most similar to when the British pound lost world currency reserve status in 1928. Only this time, considering the US and China rela-tionship, no one is sure what the replacement should be.

Q: What does this mean for portfolios?

First, at FinTrust, we globally diversify portfolios across both asset classes and strategies. Second, we are trying to educated clients on newer areas for diversification like cryptocurrencies.

Q: You first wrote about cryptocurrencies in 2013 when Bitcoin was at $80, can you dive deeper into what you are seeing today?

Financial markets hate a vacuum. There isn’t a sound reserve currency, and there is a lack of price discovery in interest rates, gold, and stocks because of central bank activities. As a result, the market created cryptocurrencies, which don’t rely on the existing market infrastructure. There truly are two parallel financial systems now—one centrally controlled and one is wide open and free.

Now, however, institutional market participants are working hard to get involved with cryptocurrencies. To put this into perspective, Fidelity now has 900 people working on its digital assets team.

As a firm, we have also established an institutional custodial solution for clients. We signed an agreement with the King-dom Trust Company—which works closely with Fidelity Digital Assets and Komainu (owned by Nomura). This agreement enables us to help clients directly with cryptocurrencies and remove many of the technology barriers.

Q: You mentioned a parallel financial system? Please expand on that thought.

It’s fascinating to watch, but cryptocurrency markets have developed prime collateral lending rates. You can now buy Bitcoin (“BTC”) and lend it (known as “staking”) at a 2% rate. Think about that for a second. Apple and Microsoft borrow money at that type of rate. The problem is they pay interest in dollars, so you still have inflation risk.

BTC, on the other hand, has limited supply characteristics and supply elasticity relative to dollars, so it may provide a large degree of inflation protection plus the 2%. If the BTC network continues to develop like Apple and Microsoft’s network of users, then an investor might expect further appreciation on top of that. Better yet, I can check my phone and see the second-by-second compounding of my money after a bio-metric security check.

To put the importance of this BTC staking rate into perspective, I think it is the equivalent of the gold leasing rate market for the digital economy.

Q: Gold leasing? Can you explain what that is?

The gold leasing rate has historically been one of the lowest interest rates on the planet because the transactions are nearly devoid of both credit risk and long-term inflationary risk. The gold leasing market has very low counterparty credit risk; the deals I am referencing are primarily taking place between central banks, bullion banks, and gold companies.

In that regard, the gold lease rate is very similar to the low-interest rates paid by Apple and Microsoft because they are AAA-rated credits. The difference, however, is that a gold company delivers gold into the lease rather than fiat currency.

Q: What are the mechanics of a gold lease rate transaction?

In a gold lease rate transaction, a central bank lends its gold to a miner via a bullion bank. The gold miner then sells the gold at the spot rate for whatever fiat currency it needs to finance the development of a mine which later (in the future) can return the gold to the central bank once it is dug up. Gold lease rate transactions really picked up after gold hit its peak in 1980 because the mining cost were much lower, so gold miners became very heavy sellers of gold while investors were panic buyers after the Jimmy Carter years.

Q: What does all this mean for today’s investors?

First, I think the big takeaway is that gold is still a good inflation hedge for the industrial economy. I have a long-term price target of $6700 an ounce. I think the mistake people make when they read a price target like that, is that they think of gold as a substitute for stocks. It’s not. Gold is a diversifier for cash and government bonds.

People also think of Bitcoin as a replacement for Gold. It’s not, because it measures something different. I think it hedges the inflationary cost of electricity embedded in the digital economy.

People make the gold v. stock mistake because gold has been compounding at an 8.9% annual rate for the last 23 years after it hit its 1998 low. However, if you look at the embedded inflation rate in the gold price since 1900, at $1800, it would be a much more modest 3.7% rate. At $6700, the embedded inflation expectation would be about 4.8% and that would match the 1980 high. As a result, I think gold and gold stocks should be mixed into diversified portfolios which contain cash and fixed income.

Cryptocurrencies, meanwhile, are more of a technology, digital economy investment. The cryptocurrency space is the first time we can watch technology venture capital markets in real-time.

Q: Any final thoughts or comments on equity markets?

We think the consensus view is that as labor markets open back up, wage pressures will moderate. We think, however, that the exit of Baby Boomers from the workforce will create persistent downside pressures on labor force participation. Thus, staffing and wage rates will become a much more persistent issues for many business and their profit margins.

Cash and Cash Equivalents

Cash rates now sit near zero, but markets are beginning to project a future rise in short-term rates following the 2022 elections. As a result, we believe alternative currencies like gold and cryptocurrency offer positive carry against cash. Given some quantitative studies we have seen we are particularly interested in gold and silver.

Investment Grade Fixed Income

Investment grade fixed income markets reflect an economic recovery. Now that 10-year treasury yields are at least equal to 10-year realized inflation rates, we are incrementally more constructive on investment grade fixed income. Given the still historically low levels, however, we still believe investment grade bonds will be a challenging asset class. We think investment grade bonds still have a defensive roll to play, but we would not expect capital appreciation from bonds going forward.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given that equity market neutral strategies historically are positively correlated to higher interest rates, we continue to favor these types of strategies.

Core Equities

Since our last report, equity prices have appreciated materially on fiscal stimulus and economic re-openings. As a result, even after adjusting for recessionary recovery, we believe equities are slightly overvalued relative to historical valuations. As a result, we are modestly constructive on equities. Given high levels of volatility, we would not overweight equities beyond investor risk determined allocations. Given our inflation outlook, we are also more constructive on small-cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low-interest rates and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. We are concerned that recent events will accelerate trends towards online purchasing and remote work, which will increasingly pressure certain real estate sectors. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

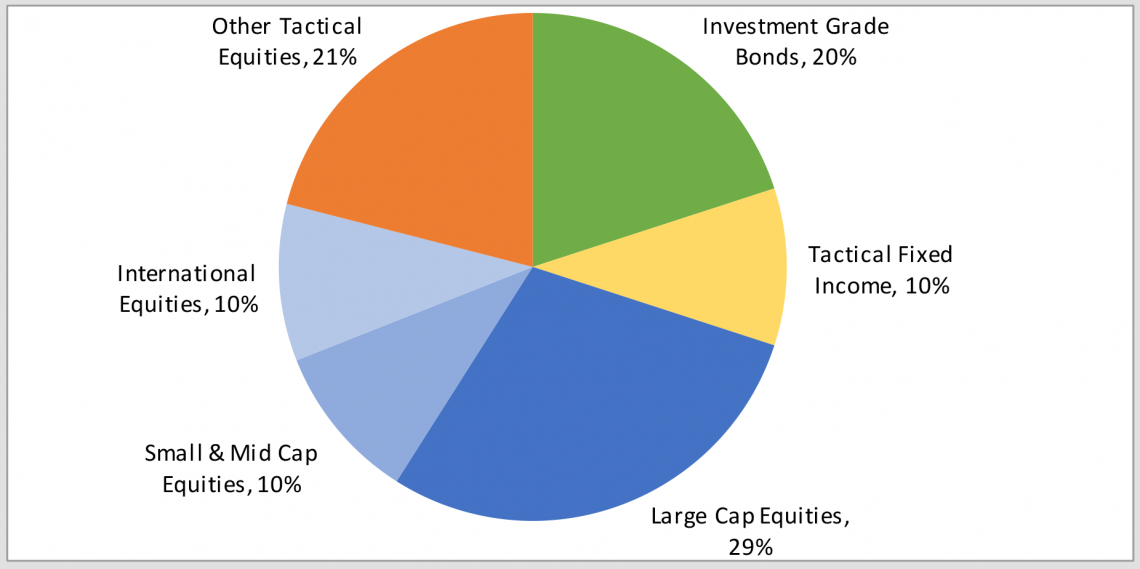

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 12/31/2020. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation

is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets

not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments

to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and

other factors.

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is the registered investment advisory subsidiary of United Community Banks, Inc., and serves both personal wealth and corporate and institutional clients. FinTrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.