A White Paper by: David E. Lewis, CFA

That question is being asked a lot these days, and many people are struggling to come up with an answer. The academics and followers of Harry Markowitz, The Efficient Frontier and Modern Portfolio Theory will tell you it is important to diversify your assets and that bonds offer stability in a volatile stock market.

For those that challenge this generally accepted and litigiously safe answer, I have an additional reason to offer you. It’s called the “D” word. With low inflation, an aging consumer and falling oil & energy prices, deflation has become more front and center in the media and in the minds of professionals and novices alike.

Bonds in a Deflationary Environment

So how do bonds benefit in a deflationary environment? I’m glad you asked. To understand this, we have to go back to a principals of economics class and revisit our old friend, the “basket of goods.” In the simplest of terms, the basket of goods theory is how we define inflation. You can buy a basket of household goods today for $100, but one year from now that same basket of goods will cost you $103. Why? The answer is 3% inflation. What happens when this works in reverse though? What if in a year from now instead of $103, the basket only costs you $98? That is deflation.

So how does this impact bonds? If we were to buy a $100 1-year bond with a 1% interest rate paid annually, we would receive $101 in one year. If inflation is 3%, then we actually lost 2% in real return (returns adjust for inflation). But in a deflationary environment, we would have made 3% real return. Because prices are dropping, our $100 is worth more in the future than it is today. This is a difficult concept to understand because many of us have never experienced this, but all we have to do is look at the Japanese and their historical inflation rates to see that this phenomenon does exists.

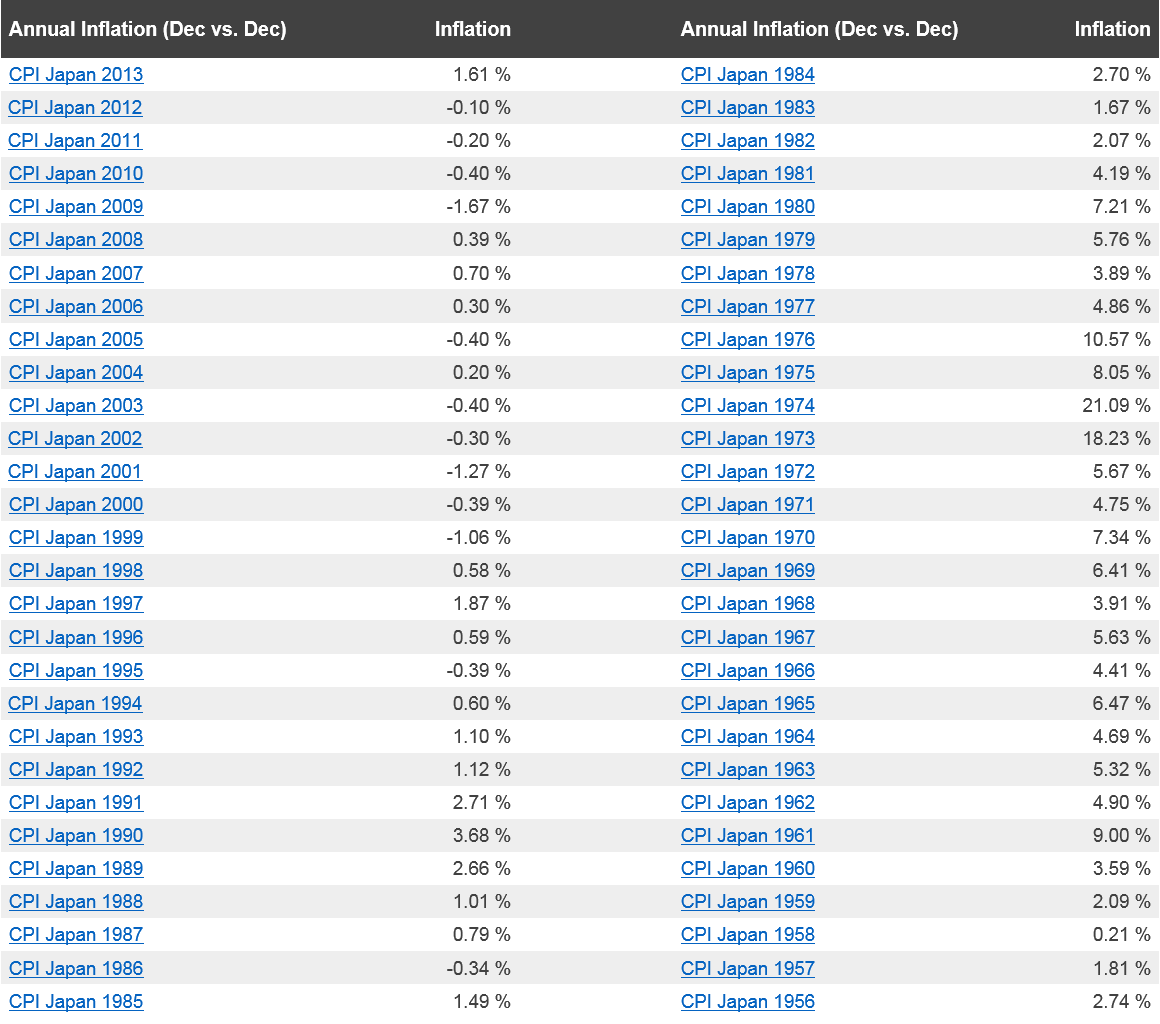

Table – Historic Inflation Japan (CPI) – By Year

– See more at: http://www.inflation.eu/inflation-rates/japan/historic-inflation/cpi-inflation-japan.aspx#sthash.xqRZ7SLm.dpuf

While the CPI does have its shortcomings, it is also the one index for which we have the most data, so we will have to rely on that. From 1956 to 1984, we can see that inflation was very persistent in the Japanese economy. In 1986, however, inflation was -0.34%. It turned positive for the next several years and then hit a prolonged period beginning in 1995 where it was either negative (deflation) or benignly low.

Looking Forward

While I am not in the business of predicting inflation rates in the US, or anywhere else for that matter, I can say two things about bonds and inflation. First, the interest rate earned is not the only component to the real return of the bond. To obtain the real return you have to subtract the inflation rate, which acts as a positive when deflation occurs. Second, I do believe bonds have a place in most people’s portfolio, and they play a particularly key role in a deflationary environment.

David E. Lewis, CFA® is a Financial Advisor/Portfolio Manager at FinTrust Investment Advisors located at the Greenville, SC office. For more information, call 864-288-2849 or e-mail dlewis@fintrustadvisors.com. The information contained herein has been obtained from sources considered reliable, but its accuracy and completeness are not guaranteed. The material has been prepared for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Past performance is no guarantee of future results. Securities offered through FinTrust Brokerage Services, LLC.