Q2 2023: Transitioning

Q: Allen, why title this WMQ “Hemlines, Lipstick, & Economic Transitioning?”

As I have detailed in several of our WMQs, economic and social trends are correlated. Economic recessions and sluggish economies impact consumer behavior differently than robust economic expansions. In addition, social, fashion, and technology trends are frequently set by younger generations, and we are at a point of a massive economic transition in demographics. As we have previously shared, the Millennials became the largest living generation in 2019. As a result, the cosmetic, fashion, and social trends of young people can tell us a lot about where we are in today’s economic cycle. Two of Wall Street’s most well-known social indicators are the Hemline and Lipstick Indices.

Q: What is the Hemline Index and what is it telling us about the economy?

The Hemline Index emerged from economic writings dating back to the 1920s on the hosiery industry, which is projected to be a $44 billion business in 2025. The economic theory proposes that hemlines move toward the floor when economic conditions are tough (because you can always cut off the excess fabric) and rise as economic conditions improve.

The theory, when quantitatively tested by Marjolein van Baardwijk and Philip Hans Franse at the Eramus School of Economics, proved to hold true. However, there was a lag time of about three years. If that is the case, then long-term investors may not really have to wait that long to see today’s investments pay off, as 2026 will be a fantastic and interesting year for the equity markets.

Q: What makes you so confident about investing with an eye toward 2026?

The world’s two big fashion shows are held each year in Paris and New York. Designers at the Paris show, according to Fashionista, “weren’t afraid to show a little skin with micro bikini tops and bikini bottoms-as-pants also proving to be popular.” Meanwhile, at the New York Fashion Week 2023 show, according to various commentaries and photos, “roses” and “flowers” and things that live among them, like animals and insects, were the most prominent design features. Beyond the roses, designers were focused on locally produced goods and provided hints of the 1990s and 1960s pop culture. Designers also highlighted technology-related fashions that can be transferred to avatars that exist inside video games and the metaverse.

Q: What do you think these fashion trends mean for the economy?

First, in Paris, “bottoms were up” to bikini levels. “Bottoms up” is a common phrase people make when giving a drinking toast, so it would seem to imply markets will be celebrating. I hope it is not because we will all be having a last drink on the Titanic and will be in need of bathing suits. At the New York show, everything was about “roses,” and “coming up roses” is another common saying for things turning out well.

Allen Gillespie, CFA®, Managing Partner Investments

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Tightening. The Federal Reserve is still targeting a 5% terminal Fed Funds rate.

- Fiscal Policy: Neutral. The CBO projects federal spending to flat-line in 2023.

- Economic Vital Signs: Inflationary pressures, while high, are moderating.

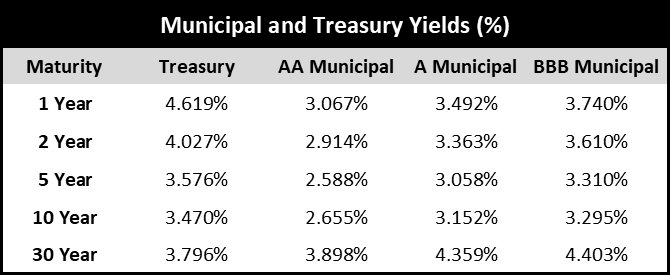

- Yield Curve Watch: The yield curve is inverted past the 3-month mark, with yields relatively flat to the 6-month mark before they decline. This implies the market expects rate cuts to start in late 2023 or early 2024.

Economic students will immediately recognize the connection between roses and John D. Rockefeller’s “American Beauty Rose.” Rockefeller saw his competitors as rose buds to be clipped. He famously stated that “the American Beauty Rose can be produced in all its splendor only by sacrificing the early buds that grow up around it.”

Economic students will immediately recognize the connection between roses and John D. Rockefeller’s “American Beauty Rose.” Rockefeller saw his competitors as rose buds to be clipped. He famously stated that “the American Beauty Rose can be produced in all its splendor only by sacrificing the early buds that grow up around it.”

Q: Can you expand on the Rockefeller and roses connection?

I think the logical connection is that the economy will be doing better by 2026, even if a few companies are clipped in the interim. For example, recently, we have seen the failure and bankruptcy of a few high-profile businesses like Silicon Valley Bank, Bed Bath and Beyond, and First Republic Bank. Still, I think the Rockefeller and roses connection runs deeper.

At the time of his American Beauty Rose comment, Rockefeller was viewed as a robber baron. As a result, he was not very popular with many Americans. American politics were anything but peaceful and settled. William McKinley had defeated the populist presidential candidate William Jennings Bryant and his calls for bi-metals (gold and silver), but later McKinley was assassinated by an anarchist.

During Rockefeller’s time, new technologies from the likes of Tesla, Edison, and Westinghouse, were also electrifying and transforming America. A great historical fiction book to read on the period is The Last Days of Night by Graham Moore. Anti-Trust and anti-business sentiment was high, and both JPMorgan and Rockefeller’s Standard Oil were sued under new anti-trust laws.

Personally, Rockefeller was known for keeping a safe full of money (which would have included gold at the time) next to his bed, along with his bible on top. The Bible inspired him to be generous. He kept a journal of his charitable giving since the very first money he earned. Over time, he gave away vast sums. He once said, “I believe the power to make money is a gift from God. I believe it is my duty to make money and still more money, and to use the money I make for the good of my fellow man according to the dictates of my conscience.” Among Mr. Rockefeller’s biggest philanthropic achievements were gifts for the creation of the University of Chicago and Rockefeller University. Rockefeller is also known for his investments in public parks and his private gar-dens like KyKuit.

As a result, one can see that Rockefeller believed in cash and gold. He made green investments in his gardens and supported medical research. It’s important to note, however, that his main investments were obviously in energy. Therefore, I think the connection between roses and Rockefeller is that current conditions may be tough, so reserve holdings of cash, gold, and alternative currencies are probably logical. At the same time, long-term investments in biofuels, solar, and energy investments would seem to make sense. Finally, Rockefeller provided almost venture capital-like support for two of today’s major research universities, so I would also suggest that he was a major investor in the medical and biotechnology industries.

Today’s bankruptcies and what we are seeing in the Lipstick Indicator would seem to imply markets may be in the process of making Rockefeller’s “American Beauty Rose.”

Q: What is the Lipstick Indicator?

Unlike the Hemline Index, which is a leading economic index, the Lipstick Index is a coincident index and is based on the economics of substitution. Lipstick serves as a more affordable fashion luxury item when compared to the cost of dresses, apparel, jewelry, and shoes. Leonard Lauder, of Estee Lauder, is credited with noting the negative correlation between lipstick sales and the economy, but I had heard of it from old timers in the earliest days of my career. There are three current trends in lipstick sales

“The American Beauty Rose can be produced in all its splendor only by sacrificing the early buds that grow up around it.”

that are really interesting to me. These trends point to today’s conditions being tough, but they also highlight some of the social issues dominating the news.

First, lipstick sales plunged during the mask-wearing phase of the Covid pandemic. As a result, some initially argued that the Lipstick indicator failed during the Covid recession. Lipstick sales then experienced a large recovery bounce. Next, since the initial recovery, lipstick sales, unlike other spending categories, have continued powering higher. Many major beauty lines have been reporting double-digit growth in lipstick and lip gloss product sales.

A third interesting trend in lipstick sales, in my opinion, is the incredible growth from the up-and-coming company E.L.F. Beauty. ELF is a more recent entrant into the beauty category, compared to companies like Estee Lauders and L’Oreal. The company made its mark by being one of the first companies to start specifically targeting men with cosmetic and beauty products beyond razors and shaving cream. Initially, the target market was defined as “metrosexual” men. In its most recent quarter, the company’s sales were up 49% year over year, both through the growth of cosmetic sales but also through an expansion in the company’s distribution deals with companies like Walmart and Target.

The lipstick sales plunge, rebound, and now continued growth would be consistent with a view that the Covid shutdowns were the worst economic recession since the Great Depression, as people could not even spend on lipstick. Given that lipstick sales are still powering higher, however, it suggests that the economy still has not fully recovered.

Q: When you combine the Hemline and Lipstick Indices, what do you think that tells us about the economy?

I think the Hemline and Lipstick Indices are sending a clear signal that we are undergoing an economic transition. We are currently in the tough, sloppy, trough part of the cycle, and we are trying to put lipstick on the economic pig. Buds are being clipped. In a few years, however, everything will be coming up roses, unless, of course, we make the mistake of just viewing the world through rose-colored glasses.

Q: Can you expand on what you mean by the risk of rose-colored glasses?

While I personally believe our demographics are improving the economic outlook, and that things will come up roses, I do worry about “rose-colored glasses” risk. In that scenario, the quantitative easing period of 2012-2022 has papered over many festering problems. Consequently, as a society, we may not have the realism and political will necessary to address our economic problems. Our economic problems, in turn, are spilling over into cultural wars and into our politics.

Q: Can you give an example of “rose-colored” risk?

Globally, the world is transitioning away from the US Dollar as the reserve currency. I believe we are moving into a world where there is no reserve currency. As a result, we will no longer just be able to print currency to solve issues like the banking crisis of 2008. Currency transitions can be orderly or disorderly.

On the orderly side, we have examples of the US moving from bi-metallism to a gold standard, then to the Bretton Woods system, and later to petro-dollars. In an orderly transition, the US will become much more self-sufficient and productive again. At a corporate level, companies will need to learn to reach millennial customers, or they will fade away. A great example of this premise is the transition from Blockbuster video stores to Netflix and streaming. Blockbuster did not survive.

On the disorderly side, I am probably most concerned about a hyperinflationary outcome like the Weimar Republic. Many of today’s hemlines, lipstick, and social trends seem to be echoes of that post-Spanish Flu and World War I period. Fortunately, I think the Federal Reserve’s recent aggressive actions have lessened this risk.

Q: Can you expand on that last thought?

Until today, the Weimar Republic may have been one of the most progressive societies in history. The primary art movement at the time was German Expressionism. Expressionism’s main characteristics were the distortion of external realities and a focus on internal conflicts. Expressionism served as an escape from Germany’s isolation and its terrible post-war economics. Gender-bending actors, like Conrad Veidt, who later played Major Strasser in Casablanca, became famous. Horror films became a popular genre, and light, darkness, and shadows were constant themes.

An art student at the University of Chicago (back to our Rockefeller connection), Kaz Rowe, has a good video titled “The Queer History of Weimer Germany” on YouTube for those interested in learning more. Today’s world of social media influencers and the metaverse certainly appears detached from reality at times. Meanwhile, the storm clouds of a potential world war seem to be expanding, as global defensive budgets just rocketed to record highs at $2.2 trillion.

Expressionism peaked along with the German hyperinflation when the government replaced the German Mark with the “Rentenmark,” which attached the value of the currency to something “real.” Then, in that particular case, it was real estate. Unfortunately, over time, the turn toward German realism resulted in a backlash against a wide range of internal minorities, and external enemies to which Germany owed World War I reparations payments.

Since 2008, the US government has been using monetary policy to distort prices from the economic realities of the housing collapse. Then in 2020, the US government used fiscal and monetary policies to further cover up the terrible economic consequences of the Covid shutdowns. Government outlays doubled in the last five years to $7.2 trillion, and then inflationary reality hit. Fortunately, the Federal Reserve is trying to re-introduce some realism into prices with higher interest rates.

Despite the risks, I am hopeful that if we can find the right balance between personal expression and sound economics, everything might just come up smelling like roses for the U.S. in a few years.

Sincerely,

Allen R. Gillespie

QUICK TAKE

MAJOR ASSET CLASSES

Cash and Cash Equivalents

The Federal Reserve finally reached its goal of pushing short-term interest rates to 5%. Short-term interest rates now exceed long-term realized inflation measures and the rates offered on longer-term bonds. Short-term interest rates are now in-line with headline inflation readings. As a result, we now believe short-term bonds can be utilized by both conservative and aggressive investors, as we believe the Federal Reserve policy is now neutral to restrictive.

Investment Grade Fixed Income

The yield curve has inverted to levels last seen in the early 1980s. Historically, inverted yield curves are associated with approaching recessions which in turn lead to spread widening in credit markets. Investment-grade fixed-income markets reflect a slowing economic recovery. We continue to believe that cyclical inflation readings have peaked and that investment-grade corporate bonds will become increasingly attractive over the next few quarters.

Tactical Fixed Income

We recently moved our tactical fixed-income allocations to be more in line with bond benchmarks as interest rates have risen. At the margin, we believe the inflation rate has peaked, and will ultimately settle in the 3%-4% range. As a result, we have rebalanced tactical fixed-income positions back toward more traditional fixed-income assets.

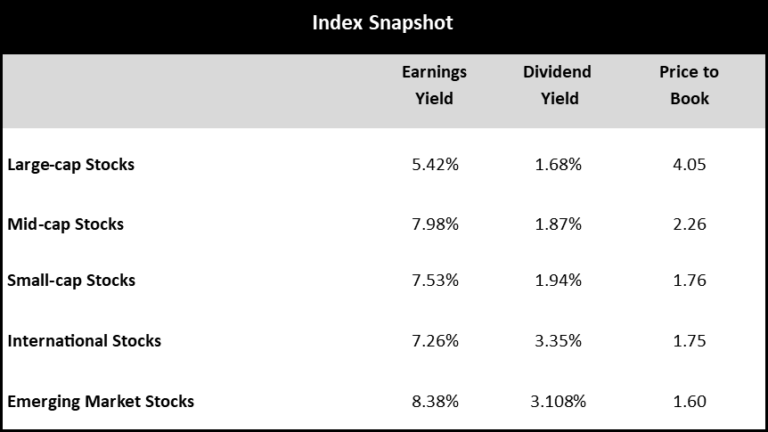

Core Equities

Since our last report, equity prices have recovered from the interest rate-induced declines in 2022. After adjusting for the recessionary recovery, we believe equities are fairly valued relative to historical valuations. Given recessionary risks and the inverted yield curve, we would not overweigh equities beyond investor risk-determined allocations. Given our inflation and valuation outlook, we are also more constructive on small-cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies, have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis, given economic volatility and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds.

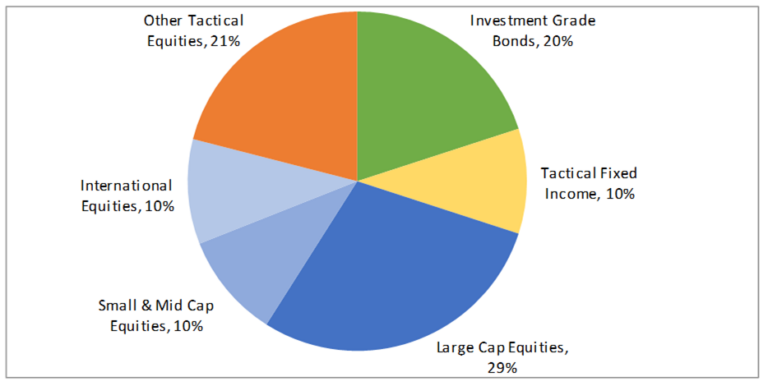

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 12/31/2022. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors is a wholly owned registered investment advisory subsidiary of United Community Banks, Inc. that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Insurance and Benefits, inc.. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.