Q4 2021: Hello Dolly

Q: Allen, why title this WMQ Dolly and the White Squirrel?

Since this WMQ is going to touch on some complex topics, I wanted to challenge our readers to think creatively. Louis Armstrong, the famous jazz singer, made the song Hello Dolly! into a true musical classic. Most of us know the song’s famous opening line “Hello Dolly, Well Hello Dolly” but few of us realize the song ends with “Dolly, never go away again.”

I got to thinking about the song’s closing line, and Dolly the cloned sheep, after seeing a white squirrel during one of my recent walks. Covid-19, which appears to have been developed in biosafety level 4 lab, mRNA vaccines, cloned animals, and white squirrels are all part of the genomic, technological, and some would say transhuman, age into which we have all been thrust, ready or not. Dolly, never go away again.

Q: Can you share with us more about the white squirrel you saw?

First, the white squirrel really made an impression on me. He seemed so out of place, easily spotted, on the dead leaves and tree bark. At the same time, I would not have seen him had my face been buried in a cellphone. Yet, I was able to take his picture because I did have my phone with me.

The smartphone also enabled me to conduct some quick research on white squirrels, read about Native American white animal symbolism, and listen to a podcast on the medical ethics of gene editing science. It made an interesting juxtaposition, being in nature with a cellphone.

Until the other day, I had never seen a white squirrel.

Q: What did you learn in your quick research on white squirrels?

Well, in case you are wondering, white squirrels are different than Jefferson Airplane’s white rabbits. White squirrels result from a genetic anomaly in the common Eastern Grey Squirrel. White squirrels are not albino, and they also have a special place in the history of Brevard, NC. I guess that is why I was able to see a white squirrel here in Greenville County, SC. You can read more about White Squirrels here (www.whitesquirrelinstitute.org).

In nature, except for snowbound areas, a white coloring reduces an animal’s natural camouflage and increases its exposure to predators. Given the rarity of white animals then, Native American folk tales do not consider these creatures to be of this world. Stories, like the white buffalo tales of the Lakota tribe, frequently considered white-colored animals spiritual omens or messengers.

Allen Gillespie, CFA®, Managing Partner Investments

Mercer Treadwell, CFA®, Senior Vice President, Investment Advisor

David Lewis CFA®, Chief Financial Officer

Thomas Sheridan, Financial Analyst

Holland Church, Data Analyst

EXECUTIVE SUMMARY

- Monetary Policy: Accommodative. The Federal Reserve has massively expanded its balance sheet and interest rates remain low.

- Fiscal Policy: Accommodative. With Democrats controlling both the White House and Congress, expectations are high for additional rounds of stimulus.

- Economic Vital Signs: energy prices are reaching levels associated with past economic slowdowns.

- Yield Curve Watch: The yield curve remains positively sloped though very low on the front end of the curve, indicating a weak recovery.

Q: Do white squirrels have a connection to investing?

I think so. Successful investing requires that one think about the future, and how it may look different than the present. Generally investors anchor expectations for the future in their personal experiences and current circumstances. Most of the time this is reasonable because the near future will not look too much different than the present. White squirrels, however, remind us that rare things do occur both in life and in markets. These rare events can show up unexpectedly, and they may not have happened in our lifetimes.

Genetically rare animals remind investors to contemplate an uncertain future and maybe even consider and contemplate things that are not easily visible like the spirit world of Native Americans, DNA, values, ethics, and morals.

Q: Can you give us some examples of things that may be rare but you feel investors should be considering?

As I have mentioned in previous WMQs, hyperinflation has been on my mind. At the same time, I think it is also encouraging investments into exciting new technologies like gene editing. Unfortunately, hyperinflations and technologies like gene editing create environments where there is a wide range of outcomes. For example, gene editing can be used to isolate certain diseases and personalize care, which is really exciting, but we also have to be realistic and realize that gene editing is being used in bioweapons programs. Meanwhile, hyperinflations create periods where traditional thinking about the value of money and prices do not apply.

I think most of us would agree that what we have experienced over the last 20+ months is outside of most of our expectations.

Q: What is the difference between hyperinflation and just old-fashioned inflation?

Inflation is the generalized rise in the price level. Inflation historically rises toward the end of a business cycle, or when a key commodity like oil, wheat, or labor gets in short supply. Inflation rising and falling is a normal part of a business cycle. Hyperinflations are different. In hyperinflations, prices are rising because there is collapsing confidence in a government and its currency—people literally will pay just about any price to get out of a currency position. Hyperinflation does not just rapidly devaluate money—it devalues a man’s stored labor—it devalues a man himself. Hyperinflations destroy entire value systems.

Q: Why do you think we could be in a hyperinflation?

Beyond the political environment, the risk for US investors is that the US accounts for 15.9% of global GDP but US dollars are used in 59% of world trade. A gradual convergence between these two numbers is manageable, but imagine what the world looks like if the dollar collapses back to its domestic share. Suddenly, there would be 4x as many dollars floating around in the US than we currently have or need. No one believes that will happen—yet if you look—you see it is already happening—all around the world.

For example, Ecuador just moved to a Bitcoin standard. Globally, there will be 21,000 Bitcoin ATMs installed this year. Paypal just enabled its 300+ million users to buy and use 4 different cryptocurrencies in its payments network which includes Venmo. Coinbase has 10 million more cryptocurrency accounts than Schwab has brokerage accounts. Russia and China have started trading oil in Yuan.

If the move away from the US dollar happens over 10 years, you are looking at 15% a year inflation. If it happens over a more manageable 30 years, it is still 4.7% inflation per year before any more deficit budgets. As global dollar usage declines, the Fed will face a hard choice of raising interest significantly or letting domestic prices potentially rise significantly.

“White squirrels remind us that rare things do occur in both life and in markets.”

Q&A with the Research Team

How is FinTrust helping investors protect wealth against such an inflation or hyperinflation?

Historically, anything that is not the currency performs ok as prices will increase as the value of money falls. Thus, we are encouraging clients to maintain their equity exposures. Secondly, in fixed income portfolios, we have allocations to strategies that are positively correlated to rising inflation. Third, we have started a cryptocurrency offering for clients who are interested or where that is appropriate, and we are expanding our research efforts in this area.

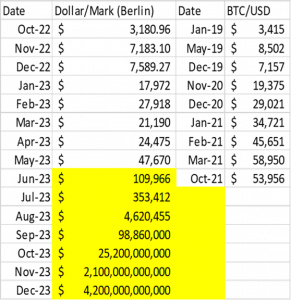

While I am a big believer in the value of cryptocurrency and blockchain processes, I am a little concerned with how tightly the US Dollar Bitcoin price is tracking to the German mark during the German hyperinflation. The German hyperinflation ended the Weimar Republic, but the American Revolution was also financed through the hyperinflation of Continental Dollar, which is where the phrase not worth a Continental originated.

Can you expand on gene editing technologies?

Technologies like gene editing, are really interesting and exciting for investors. The technology, however, also raises a tremendous number of moral and ethical issues that are worth openly discussing.

Senator Marco Rubio asked a really important question at a recent Senate Intelligence hearing —and I encourage everyone to go watch it—the question was this—Why do they want the DNA of Americans?

The discussion quickly turns to a conversation about genotypes and phenotypes and Wall Street’s financing of the Chinese economy. Now, some of this could be benign as the China 2025 Plan had targeted being a leader in biomedicine— and the United States should be competing for that industry as well—but as I mentioned, most technologies have a dual-use.

Q: Is this why you listened to a medical ethics podcast?

Absolutely. World War II gave us the Nuremberg trials, but Nazi Germany was not the only government engaged in horrific bio and chemical weapons testing on humans. Unfortunately, the Japanese, United States, Russia, and Great Britain all had testing programs. For example, in the United States, there were the Tuskegee experiments and the mustard gas tests on San Jose Island, and these tests had racial and ethnic components to them. I repeat Sen. Rubio’s question again then to see if you hear it differently—Why do they want the DNA of Americans?

Thirty years ago, I actually had the opportunity to read parts of the Nuremberg trial transcripts. As a freshman at Washington & Lee, I got caught drinking adult beverages in the dorm. As a punishment, I had to go dust books in the federal repository section of the Leyburn Library. This section contained books of the trial transcripts, so I found myself doing more reading than dusting. Interestingly, Stanford University recently digitized all the Nuremberg records.

It concerns me that we live in a world where we could be moving towards hyper-personalized medicine and finance, and yet we seem to be moving toward more centralization, socialism, communism, and fascism.

Unfortunately, the internet itself seems to have followed a similar progression away from personal responsibility. Initially, it was the worldwide web, and you had to take responsibility for navigating to various websites. Then America Online became a convenient aggregator of content until Google, Facebook and Twitter replaced it. Then, the other day, people were calling their cable and telephone company internet providers to complain that the internet was down just because Facebook went offline for 6 hours. Think about that for a second—a handful of the 1.7 billion websites go offline, and people think the internet is down. That’s an unbelievable concentration of corporate power and a sad comment on free thinking.

Q: Any final thoughts on the markets?

I recently bought a solar power generator, and I am thinking about solar panels for the house. The Green New Deal policies which are popular with the political and ESG crowd seek to raise the cost of energy and carbon. They want to force substitution. Unfortunately, energy prices are a regressive tax, so it’s trickle-up economics. Until we have the necessary substitute infrastructure, I think that will continue to make the political environment volatile.

At some point, higher energy prices will begin to curtail consumer spending, so the world could get pushed back into a double-dip recession. Alternatively, the power will go out, and people will just be left in the cold. We saw that this year in both Germany and Texas. We are trying to estimate at what point energy prices become a problem, I think we might be getting close with oil at $80 and natural gas now above $6.

The upside to learning to work from home during Covid-19, and a knowledge-based economy, however, is that there are parts of the economy that are more resilient to higher energy costs than in the past—which is why I am encouraging people to go solar and reduce their reliance on centralizing systems.

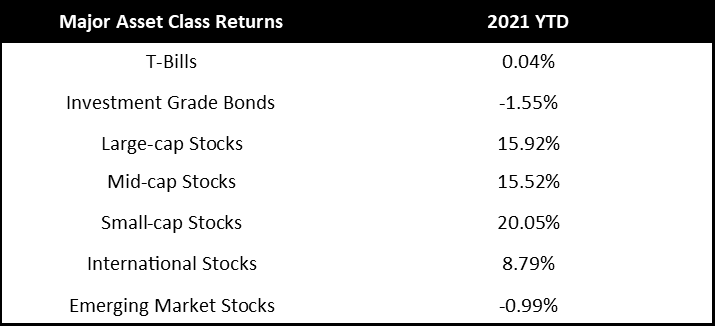

QUICK TAKE: MAJOR ASSET CLASSES

Cash and Cash Equivalents

Cash rates now sit near zero, but markets are beginning to project a future rise in short-term rates following the 2022 elections. As a result, we believe alternative currencies like gold and cryptocurrency offer positive carry against cash. Given some quantitative studies, we have seen we are particularly interested in gold and silver.

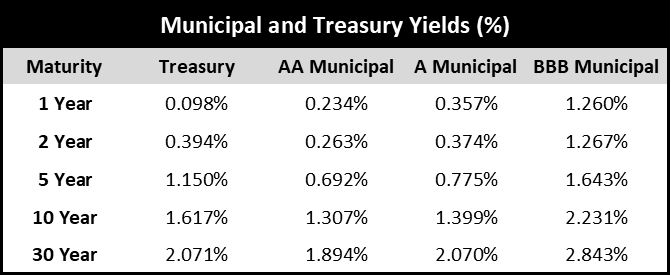

Investment Grade Fixed Income

During the second and third quarters, the yield curve flattened but maintained a positive slope. Investment-grade fixed income markets reflect an economic recovery and credit spreads remain tight. More recently, the yield curve has begun to take on a steeper shape. That 10-year treasury yield is once again equal to the 10-year realized inflation rate, but inflation readings have been coming in higher, and we continue to hear about additional price increases in the pipeline. Given the still historically low yield levels, we still believe investment-grade bonds will be a challenging asset class. We think investment-grade bonds still have a defensive role to play, but we would not expect capital appreciation from bonds going forward.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given that equity market-neutral strategies historically are positively correlated to higher interest rates, we continue to favor these types of strategies.

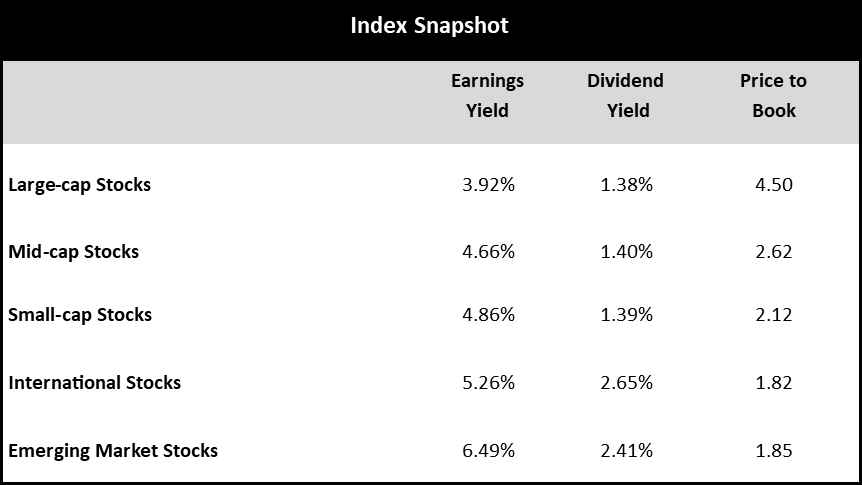

Core Equities

Since our last report, equity prices have appreciated in the large-capitalization bond proxies, while the number of advancing stocks to declining stocks has turned materially negative. After adjusting for recessionary recovery, we believe equities are slightly overvalued relative to historical valuations, and we are beginning to grow concerned about rising energy prices. Given high levels of volatility, we would not overweight equities beyond investor risk determined allocations. Given our inflation outlook, we are also more constructive on small-cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies, have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low-interest rates and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds.

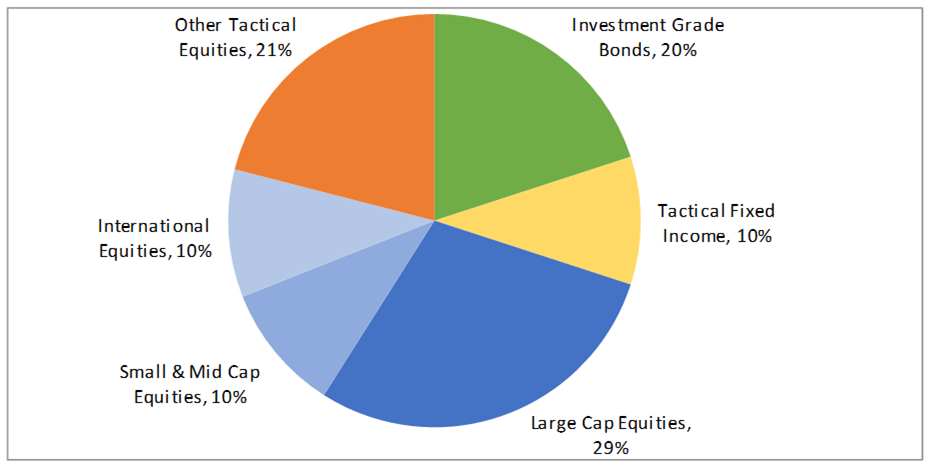

FINTRUST ALLOCATIONS (70/30 RISK PROFILE) WITH TACTICAL

About FinTrust Capital Advisors, LLC

FinTrust Capital Advisors, LLC, established in November 2007, is a registered investment advisor with the Securities and Exchange Commission (“SEC”) pursuant to the Investment Advisers Act of 1940 and is a 100% owned subsidiary of United Community Bank, Inc.

We are a full-service financial service firm with over 35 professionals throughout the southeast. Headquartered in Greenville, South Carolina, FinTrust has additional offices in Anderson (SC), Athens (GA), and Macon (GA). The Company has approximately $2.1 billion total assets under advisement across our advisory, retirement plan, and brokerage business. In a combined basis with United Community Bank, Inc., FinTrust Private has $4.4 billion in assets under advisement.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.