Broken Models & Interest Rates at Ground Zero

During World War I, an area developed between the trenches that quickly became known as No Man’s Land. It was truly a hell on earth, a barren field between warring sides, landscaped with barbed wire, seeded with mines, full of trenches and holes, overseen by snipers, and littered with broken bodies and machines. Despite life crippling wounds, my grandfather, Jesse Gillespie, lived to tell his story from this frightful experience.

A first hand account

Jesse was part of the first American wave of soldiers to arrive in Europe. As my grandfather would later recount, the boys in Washington rushed them off to Europe to get shot up about as quick as they got off the boat. He, like most of his unit, was reported dead on May 28, 1918 at the Battle of Cantigny. He later hung his death certificate on his office wall and had to give testimony as to being who he said he was following the war. The U.S. Army had lost track of him between the battle and his weeks in French hospitals, and thus the death certificate as he was assumed killed in action. He later served as Pickens County, SC Treasurer until the 1960s.

Jesse Gillespie survived No Man’s Land by inching his way back to safety over the course of three days despite his wounds. During this time, he never lifted his head, as his goal was to remain flat and avoid snipers. He would kick his way along the ground in small, methodical ways each night. He vividly remembered how thirsty he felt while in No Man’s Land, which led to a focused search for water while navigating the potholed landscape.

A Financial No Man’s Land?

As the Federal Reserve winds down its quantitative easing (QE) program after five years of war against a perceived deflationary threat, financial models are quickly being brought to a Financial No Man’s Land. Financial No Man’s Land is an area full of broken models, potholes, low lying interest rates, and an area where many investors vividly feel the thirst for yield.

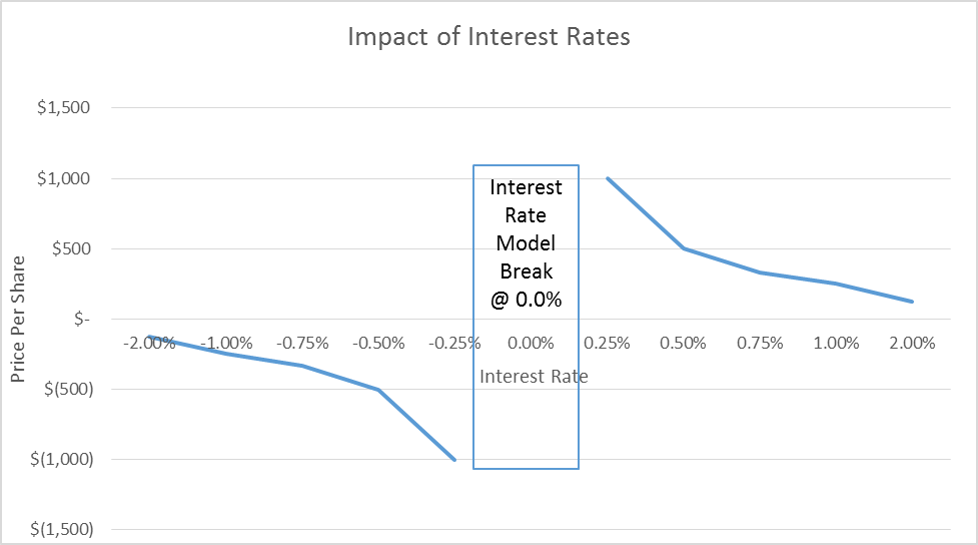

Let’s consider the impact a negative interest rate has on a stream of cash flows, in this case a perpetuity.

If Value = CF1/i

Where CF1 = cash flow in one year

i = discount rate

From this formula, one can see that a negative discount rate leads to negative values for a positive cash flow stream and positive values for negative cash flow stream, into perpetuity, a hell of a conclusion. In short, money and earnings today have negative value. A financial analyst’s no man’s land. This situation clearly lifts unprofitable enterprises, favors heavy borrowers who have low current cash flows (high yield) and high growth J-Curve type businesses that are investing dollars today for dollars in the future. If a negative interest rate policy were to persist into perpetuity, then the most valued enterprises would be those that constantly lose money into perpetuity or spend more than they earn, like governments. Man, however, cannot forever survive in No Man’s Land. Hence, there must be limits to QE, just as No Man’s Land of WWI did not last into perpetuity.

Now let’s consider a perpetuity discounted at a zero interest rate.

Now the financial analyst is really in No Man’s Land. The analyst’s models can handle a negative interest rate or a positive interest but not a zero rate, regardless of whether his cash flow is positive or negative. He is uncertain. Does he charge forward or crawl back to safety?

Finally, let’s consider a cash flow discounted by a small but slightly positive interest rate.

Well, now the financial analyst has survived No Man’s Land and is euphoric just to be alive, as his discount model calculates to a nearly infinite value for a positive cash flow stream and a negative value for negative cash flow streams.

These scenarios are pictured below.

Obviously, for most investments there is a stream of cash flows discounted by a yield curve. Let’s, therefore, consider the impact of negative interest rates on the front end of a stream of cash flows and a positive interest rate on the long end of a stream of cash flows, such that i1 < 0 and i2 > 0.

Value = CF1/i1 + CF2/i2

Where:

CF1 = cashflows in period one

CF2 = cashflows in period two

I1 = interest rate in period one

I2 = interest rate in period two

Given this scenario of negative interest rates followed by positive interest rates, one sees the value in either zero or negative cash flows in period one and positive cash flows in period two. Thus, one can see that QE leads to a conclusion that would favor businesses that are investing/losing money today while promising high cash returns later. In short, QE promotes the ultimate junk and growth stock rally.

The Fed’s Charge Across No Man’s Land

The Fed is currently tapering its QE policy, which effectively means that its negative interest rates are quickly approaching the zero bound where financial models do not work. Notice how the value of a cash flow flips from a negative value to a nearly infinitely positive value on plus side of the zero bound. Also notice that the value becomes the most negative, then the most positive when approaching the zero bound. What is most interesting is how after crossing the zero bound to the positive side, lower values reside whether interest rates go up or go back down. In short, there is no safe place once the Fed Charges Across No Man’s Land for fixed income investors with a single steady stream of cash flow. An equity with increasing cash flow might be able to outrun the impact, and a bond investor might be able to roll down.

How to Survive – Conclusion

The Fed has maintained a negative interest rate policy via QE for the better part of five years and is due to change the sign on interest rates from a negative to zero and maybe to a positive this quarter or at the start of the 4th quarter. We anticipate that this will have large ramifications, however, not as uniformly as market participants expect.

QE has unquestionably but reasonably encouraged speculation on firms with negative current earnings and cash flows and large future potential positive cash flows. In addition, bond investors have rightfully refinanced high risk credits. Consistent growers have appreciated but have been penalized by negative interest rates for having positive cash flows. In short, quality has underperformed in both fixed income and equities during QE.

First, as the Fed approaches the zero bound, there are large negatives on positive cash flows. After these negative, there then is the uncertainty associated with zero interest rates, before once again reaching the stability of positive interest rates. Once crossed, however, there is likely to be a switch to quality. For high cash burn, high growth companies, we believe it will negatively impact values, maybe with crash like dynamics. For high cash flow moderately growing enterprises, the result of charging through No Man’s Land might be volatile and negative before becoming extremely positive until higher positive interest rates quickly impact values. For bonds, we believe the end of QE will mark the long awaited peak, as once on the positive side of zero, either direction in rates will lead to a decline in value. In short, there is no going back for bonds as both more QE or higher interest rates mean lower prices beyond the zero bound.

I think the way to survive the charge across the Fed’s Financial No Man’s Land is the same for investors as it was for my grandfather – stay flat and liquid as best you can, realizing you might get wounded, but at least you’re are not dead. If you can survive there are decades of positives ahead.

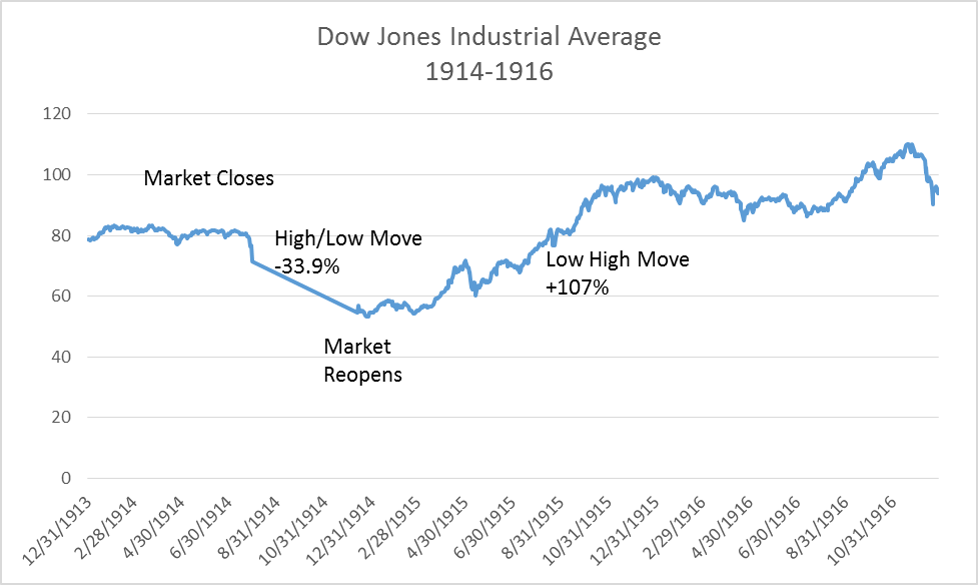

Keep your head down, stay liquid, and roll. It is the key to surviving No Man’s Land. For the curious, below is a chart of the Dow Jones Industrial Average 1914-1916 at the outbreak of WWI. Look familiar?

Source: djaverages.com

Allen R. Gillespie, CFA is a partner with FinTrust Investment Advisors in its Greenville, SC office. For more information, call 864-288-2849 or e-mail agillespie@fintrustadvisors.com.