First Quarter 2021

Q: Allen, as we exit 2020 and look forward to 2021, how would you summarize what you see happening in the markets?

I think January 6, 2021 created a massive, economically important temporal marker. I believe, in time, it will mark the day the US Dollar lost its status as the world’s reserve currency. This will mark the end to the deflationary cycle of the last 40 years.

Currency regime changes create both risks and opportunities, particularly for American investors because we are not used to having to think about currency questions. The last time Americans really had to think about currency markets was during the 1970s when Nixon ended the Bretton Woods Agreement. As a result, South American, Asian, and European investors tend to be better versed in the subject.

Q: The loss of currency reserve status, why do you think that?

The dollar would have likely lost its reserve status anyway, but it seems January 6 confirmed what global investors already knew—the dollar system has outlived its usefulness.

Here’s a little background: Approximately 70% of all US Dollars are used outside of our country. Meanwhile, US gross national product on a purchasing power basis only accounts for about 16% of global GDP.

Since the British pound lost its reserve status in 1928, we have been using various versions of the dollar system. Since that time, people have been happy using our currency because of our stability, military, and rule of law.

Now, honestly ask yourself these questions from the perspective of an outsider sitting on US Dollars after January 6: do you have more or less confidence in America’s political and legal system? So, are you more or less willing to hold a US Dollar after 2020? Will you seek to bring your money home? Or, will you move your money somewhere else or to something else that is more stable?

The answer to the dollar question will be the dominating trend of the next four years and beyond. Historically, when currency regimes change, they change permanently.

Q: What are the risks and opportunities associated with the loss of currency reserve status?

On the opportunity side, as I mentioned last year in some videos, anything that is not a George Washington will go up in price over time except for bonds. Devaluations start in the currency markets, and then they impact the other asset classes like bonds, stocks, and commodities.

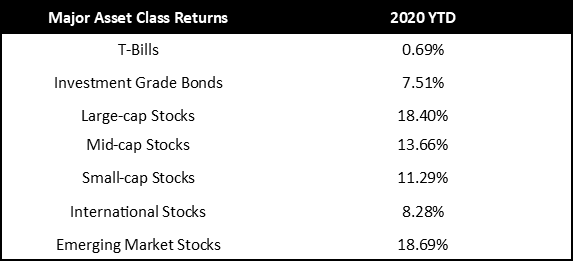

Source: Morningstar Direct, As of 12/31/2020

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

EXECUTIVE SUMMARY

Monetary Policy: Accommodative. The Federal Reserve has massively expanded its balance sheet and has started buying corporate bonds and ETFs directly.

Fiscal Policy: Accommodative. With Democrats controlling both the White House and Congress expectations are for additional rounds of stimulus.

The Curse of Tippecanoe: is the story about Presidential succession for reasons other than an election. Biden will be the oldest person to ever take the presidential oath.

Yield Curve Watch: Inflation expectations are breaking out above 2%, a full 100 basis points higher than the current 10-year yield.

“I believe, in time, January 6, 2021 will mark the day the US Dollar lost its status as the world’s reserve currency.”

Q: Let’s start then with the currency markets. What do you think about precious metals?

I just saw a statistic that silver went up over 6x during Jimmy Carter’s administration when the Democrats controlled both Congress and the Presidency. Silver also went up 4x in the brief time the Democrats controlled Congress under Obama. Importantly, both of these episodes happened while the US Dollar was still the reserve currency, so I do think the move in silver could be shockingly large.

In an ironic market twist, the Democratic Sweep might be great for gun totting silver stackers—they may even learn to like the guy because they will be filthy rich by the end of this Congress. A big move in silver would also create a huge boom in Mexico.

Turning to gold. The gold price has crossed the book value of the Dow Jones Industrial Average twice in the last 100 years (1932 and 1980). Today, book value on the Dow Jones sits close to $7000, so gold could still have a big move as well.

Q: What about gold and silver equities?

When inflationary moves really get going, governments tend to turn to confiscation through taxes, mandates, and other means, but then they create loopholes for industry. For example, Roosevelt’s Executive Order 6102 required citizens to remit their gold at the old pre-devaluation level of $20.67, but the gold industry could sell at the market price of $35. As a result, gold stocks did really, really well.

Therefore, gold and silver that is in the ground and can only be delivered in the future is a great place to have it. If the government wants it, it would have to dig it up for you. I do think the cryptocurrency move has reduced the demand for previous metals and mining shares, but I don’t think it is an either or situation. I think both cryptos and metals can increase in price, as I think they measure the inflation rate of different things. Gold does a good job of measuring inflation in the industrial economy, and cryptocurrencies better measure inflation in the digital and data economy.

Q: Cryptocurrencies have gone up a lot in 2020. What are your thoughts now? Is it a bubble?

I think the dollar and bond markets are the bubbles, so I am still very bullish. Globally, according to the Bloomberg terminal, there is over $18 trillion in negative yielding debt. That’s $18 trillion guaranteed to loose money. That’s a bubble.

Cryptocurrency is a volatile space, but I think the lightbulb finally went off for people in 2020. My first client article on cyptocurrencies was in 2012 when bitcoin was at $74 dollars. Since then, the fundamental underpinnings have only improved. Paypal just rolled out cyptocurrency payment settlements to its 300 million users and Square has done the same. People are starting to learn about cryptocurrency. I plan on doing a lot more education on the topic.

Here is where the math stands today from a currency perspective. The US Bank Deposit market is roughly $14 trillion. At just 2% inflation, that $14 trillion loses $280 billion in purchasing power per year. The cryptocurrency market has roughly a $1 Trillion market capitalization. If cryptocurrencies just offset the Fed’s targeted inflation rate, the market would go up 28%. The starting market cap in 2020 was about $280 billion, so the inflation really made it skyrocket. If Bitcoin replaces gold’s $14 trillion market capitalization as a preferred non-fiat store of value, then over the next 20 years, it would go up 14% a year on average. I estimate the cryptocurrency markets will grow about 23% a year because that has been the historical growth rate for the internet over the last 20 years.

Q: How does your inflation thesis impact equities?

The equity of good companies at reasonable prices is always a great investment. Reasonable prices during a hyperinflation, however, can only be determined after adjusting for inflation. Equities, however, may be even better if those good companies are international or make their money overseas. With international equities, you get both the growth in equity plus the currency return. Domestically, the reflation trade tends to help small companies more than larger companies. The large companies rely too much on foreign labor which may be getting more expensive.

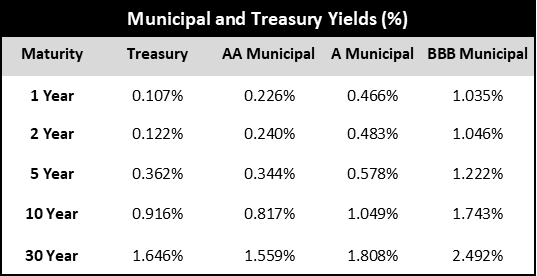

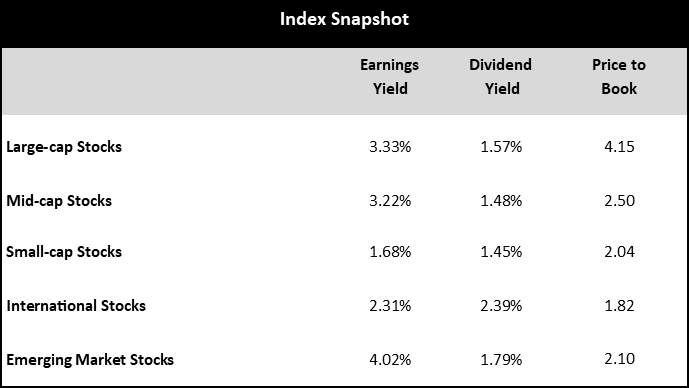

Source: Bloomberg as of 12/31/2020

Q&A with the Research Team

Q: It sounds like you are bullish on international equities.

I am very bullish on emerging markets. The demographics are better and emerging markets have been outperforming since about last June. Fundamentally, emerging market countries generate about 30% of global GDP but only make up about 12.5% of global market cap. Meanwhile, the US accounts for 16% of global GDP but 54% of global market cap. There are plenty of 10 year periods where US and emerging market returns diverge.

Q: What do you see coming from the new administration?

Biden is the oldest person to ever take the oath of office, so it is understandable that succession is on my mind. If we do see a Harris administration there is a chance she would be in office as long as FDR (Biden’s term plus two more).

Most of the economic proposal I have seen from the incoming administration will hamper growth but there are some positives. For example, the new administration wants to expand the SBA’s loan programs and give minority owned businesses a better opportunities. I do think the broad expansion of the SBA was a huge positive during the Covid downturn. Another positive: there will also be an infrastructure bill.

On the negative side, the administration wants a doubling of the minimum wage—numerous economic studies show minimum wage hikes cut employment and encourage automation. As the Congressional Budget Office report on the topic clearly states, by 2025 the $15 wage level would boost the wages of 17 million workers at the cost of 1.3 million jobs. In addition, many minimum wage jobs are in travel and leisure—which were the sectors hit the worst in 2020. The plan seems to be to raise wages while accepting higher unemployment and supporting people through Universal Basic Income concepts. Ultimately, these types of economic policies have a stagflationary (high inflation and high unemployment) characteristic.

The administration will support the United Nations’ 2030 Agenda which is all the about “Green New Deal.” Fundamentally, it will raise energy prices, which is a regressive form of taxation. Higher prices will create opportunities for investors, particularly in natural gas related businesses because gas is the transition fuel. I am highly skeptical due to my experience with Environmental, Social, and Governance (“ESG”) mandates.

I have studied ESG mandates extensively because I used to manage a 5-star fund when I lived in New York that only invested in alcohol, tobacco, aerospace and defense, and casino gaming companies. Here is what our research showed. Restrictions—like licensing for tobacco—do limit the activity, but the reductions in competition and supply increase the price more making the business better.

For example, the number of smokers as a percent of the population has declined from 42% to 13% over about the last 50 years. Despite this, Philip Morris was able to raise prices faster (the inflation rate of a pack of smokes if you will) to the point that the company earned a 19% return on equity despite the restrictions. As a result, the company accounted for over 10% of all stock market returns for the 50 year period of

our study while also being the largest tax payer at the same time—economically it was an incredible business.

One of my good friends, Professor Bruce Yandle of Clemson University, wrote a funny economics book on the effect called Bootleggers and Baptist: How Laws Get Made. It was a study of blue laws. The basic premise is watch out when bootleggers and Baptist get together to make law. The moralist feel good while the bootleggers run off with the money.

I think the Green New Deal and ESG mandates will create similar Bootleggers and Baptist effects in the energy sector. This is really important for the follow reason: since World War II, until Covid-19, every US recession had been preceded by rising energy prices. This happened because we were a net importer of energy. People forget that oil went to $150 just before the Global Financial Crisis in 2008. Following that recession, we had a huge fracking boom and the US became a net exporter of energy. All of this resulted in a more resilient economy until Covid. The Green New Deal will make energy more expensive and harder to produce, so we will be reintroducing cyclicality back into our economy.

Lastly, government shutdowns create risks for investors that cannot be priced into legal markets. Economically speaking, shutdown policies raise the cost of capital for small businesses which are the largest job creators in our economy. If the costs of operating become too high, market participants move underground, go dark, and flee to better locations. We are already seeing this effect in state to state migration patterns.

Q: Any final thoughts as we enter 2021?

In 1919, John Maynard Keynes wrote The Economic Consequences of the Peace following the World War I Paris Peace Conference. He believed the Allied Power’s desire for reparations and revenge would ultimately harm everyone. He was correct. Within four years, the German inflation had gone critical, culminating in the 1923 hyperinflationary disaster. The Germans never forgot what happened.

My title references this work because it is a good reminder that it pays to be humble and magnanimous in both life and politics. I am not sure, however, if today’s politicians and central bankers agree.

As we enter 2021, I think the hyperinflation will begin to accelerate because of the Economic Consequences of the Capitol Breach. This will create both risks and opportunities and we will be positioning portfolios accordingly.

QUICK TAKE MAJOR ASSET CLASSES

Cash and Cash Equivalents

Cash rates now sit near zero, and future’s markets are projecting negative short-term interest rates in the Unites States. As a result, we believe alternative currencies like gold and cryptocurrency offer positive carry against cash. Given some quantitative studies we have seen we are particularly interested in silver.

Investment Grade Fixed Income

Investment grade credit spreads widened materially during the 1st quarter, but then they narrowed to more normal recessionary levels after the Federal Reserve began buying corporate bonds and bond exchange traded funds. While attractive on a spread basis, the low level of interest rates, generally makes investment grade bonds a challenging asset class. We think investment grade bonds still have a defensive roll to play, but we would not expect capital appreciation from bonds going forward.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Given that equity market neutral strategies historically are positively correlated to higher interest rates, we continue to favor these types of strategies.

Core Equities

Since our last report, equity prices have appreciated materially while earnings have declined. As a result, even after adjusting for recessionary recovery, we believe equities are slightly overvalued relative to historical valuations. As a result, we are modestly constructive on equities, but we believe individual security selection rather than asset allocation will be increasingly important going forward. Given the high levels of volatility, we would not overweight equities beyond investor risk determined allocations. Given our inflation outlook, we are also more constructive on small cap and international equities.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward tradeoffs. Tactical equity strategies, like long/short equity and option-based strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low interest rates and the likely structural changes to the economy.

Other Markets

Other markets like gold, cryptocurrency, and real estate may offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. We are concerned that recent events will accelerate trends towards online purchasing and remote work, which will increasingly pressure certain real estate sectors. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

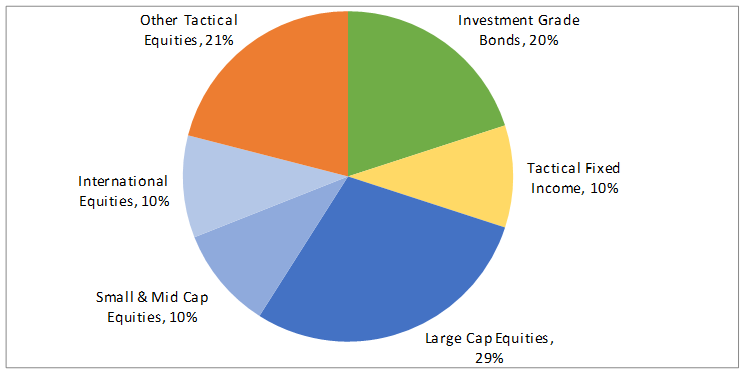

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 12/31/2020. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.