In a world where interest rates are low and the stock market hovers near all-time highs, investors looking to deploy cash are stuck between a rock and a hard place. Many don’t feel comfortable buying stocks at these current levels, while the specter of rising interest rates makes investors nervous about additional fixed income exposure.

At FinTrust, our active, relative value research process seeks to identify assets classes, sectors, and strategies that may be undervalued, as well as those that may be expensive and ripe for correction. As an independent advisor, we also seek to leverage an extensive network of products and third-party research teams to identify ways in which to capitalize on the insights of our research process.

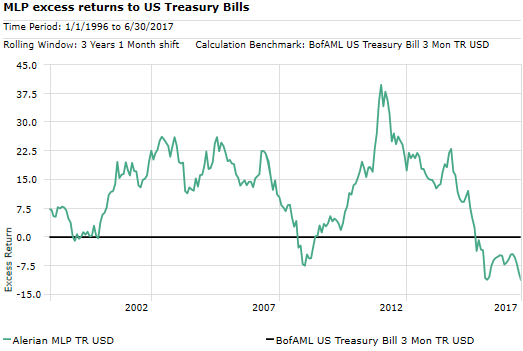

One area of the market that we currently find attractive is the midstream gas and oil master limited partnerships sector, or MLPs for short. When looking at rolling 3-year returns compared to US Treasury Bills, MLPs as a whole, are trading at levels not seen since the financial crisis. In fact, over the last three years, MLPs have underperformed T-bills, considered a risk-free benchmark. Economics 101 teaches us that any risk asset that does not provide a return over and above the risk-free rate over time, should not exist. It is clear that sentiment is very negative in space, but the timing of any change is unclear.

Source: Morningstar Direct

This chart’s hypothetical illustration uses historical monthly performance from January 1996 through June 30, 2017 on a rolling three-year basis from Morningstar Direct; MLP stocks are represented by the Alerian MLP Total Return Index and short-term investments are represented by U.S. 90-day t-bills. Chart is for illustrative purposes only and is not indicative of any investment. All indices are unmanaged. You cannot invest directly in an index. Past performance is no guarantee of future results. Investing involves risk, including the risk of loss.

Midstream MLPs connect upstream companies that extract resources, think exploration and drilling companies, to downstream companies that refine and process oil and gas, and then sell to consumers. Fees paid to MLPs are charged as volume is moved, stored or processed. The volume of traffic, not the price of what’s being transported, is the primary determinant of the amount of revenue generated. Thus, stock prices of midstream MLPs have historically not been highly correlated with oil or natural gas spot prices over long-term periods. This is because midstream revenues typically function like a toll road.

What we have seen since 2014 however, is that MLPs have traded lower in unison with oil prices. In our view, this is indicative of fear permeating the energy complex stemming from an abysmal 2015 where MLPs lost about a third of their value. We believe that the space has been overly punished, which could create significant opportunities going forward. In our opinion, current pricing is not likely reflective of the underlying fundamental value that these entities represent. Many MLPs continue to report sound financial results and growing cash flows.

Our research thesis looks towards a 3-5 year view. As of this writing, the benchmark Alerian MLP Total Return Index sports a current yield of 7.67%, whereas the 10-Year Treasury yields 2.2%. This yield differential could provide a buffer if prices fall further, and may compensate patient investors as they wait for conditions to improve. In fact, if prices just remained flat and an investor just earns the dividend return then our relative value chart will cycle up from its current lows.

There are a number of ways that investors can play this idea, both passively through index funds or ETFs or through an active manager. In addition to our research process focus on the high-level ideas, at FinTrust we also employ a rigorous criteria to identify best in class products to execute on our strategy so that clients can have peace of mind when it comes to their investments.

Sincerely,

Cliff Hodge, CFA

Portfolio Manager

FinTrust Investment Advisors

Important Disclosers This material was prepared by FinTrust Investment Advisors, LLC (“FinTrust”) and/or one of its affiliated entities, FinTrust Investment Advisory Services, LLC (“FTIAS”) and FinTrust Brokerage Services, LLC (“FTBS”) and is excluded from the definition of “research report” found in FINRA Rule 2241. This material is a market commentary and does not constitute research, and has not been prepared in accordance with regulatory requirements designed to promote the independence of investment research and is not intended to form the basis for any investment decision. This material has been prepared for informational purposes only and is not intended to be, and should not be considered, a solicitation or an offer to buy any security or instrument or to participate in any trading strategy to which it applies. The information provided herein does not constitute investment advice or take into account the individual financial circumstances or objectives of the individuals who may receive it. You should consult with your own accounting, legal or other advisors as to the adequacy of this information for your purposes. This document is not advertising or marketing any financial investment product, service or transaction. Past performance is no guarantee of future results. Diversification does not ensure a profit or guarantee against a loss in a declining market. As with any investment strategy, there is potential for profit as well as the possibility of loss. All investments involve risk and investment recommendations will not always be profitable. Because of its narrow focus, sector investing tends to be more volatile than investments that diversify across many sectors and companies. Sector investing is also subject to the additional risks associated with its particular industry. Any statements regarding market or other financial information are obtained from sources which FinTrust believes to be reliable, but it has not been independently verified by us and we do not warrant or guarantee the timeliness, accuracy, reliability or appropriateness of this information. All information is provided “as is” and FinTrust makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any information included herein. Views expressed are as of the date indicated, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the views and/or opinions provided in this publication are those of the author(s) alone and not necessarily those of FinTrust or its affiliates. FinTrust does not assume any duty to update any of the information contained herein. This document must not be forwarded or otherwise made available to any other person without the express written consent of FinTrust. Securities offered through FinTrust Brokerage Services, LLC, member FINRA/SIPC. Advisory services offered through FinTrust Investment Advisory Services, LLC, an SEC registered investment advisor