SUMMARY

- The Ukraine war is a key variable.

- Energy security and renewables will remain a market focus.

- India will become the most populous country with the largest workforce.

- The end of the Quantitative Easing Era means higher interest rates will persist.

- Circular business models will be a key driver of strategy.

- Portfolios need broad diversification and regular rebalancing to balance today’s risk and opportunities.

Portfolio Commentary

Written by Allen Gillespie, CFA®, Chief Investment Officer

The Economist World Ahead 2023

Each year, The Economist publishes its World Ahead issue which looks at key economic trends for the upcoming year. This year the magazine looked at the economic impact of the great-power rivalry taking place in geopolitics, demographic changes, and the business opportunities associated with rapid social changes and technology trends. The key themes include:

The War in the Ukraine

The war in Ukraine is quickly expanding. Given Russia and Ukraine’s importance to energy, grain, fertilizers, industrial metals, and gas markets, as an escalating conflict is likely to keep key commodity supply chains strained. Historically, major wars lead to inflation, and higher interest rates, create food shortages and displace people. The U.S. has now allocated over $100 billion to Ukraine’s war effort, while Russia will spend $84 billion on defense, up from an estimated budget of $61.7 billion. Strategically, NATO countries seek to send a message that a Chinese invasion of Taiwan will not be tolerated. Meanwhile, countries near potential hotspots like Japan (the world’s third-largest economy) are also increasing military spending. It appears war economics will continue in 2023, which leads to this year’s second theme.

Energy Security and Renewables

Given Russia’s importance to traditional energy markets, countries like Germany are rushing to rethink energy supply chains. In the short run, this is leading to a return to “dirtier” but more domestically available production from energy sources like wood burning and coal. Over more intermediate horizons, the higher energy prices will also encourage the continuation of trends toward conservation and increased use of renewable forms of energy like solar, wind, and hydrogen and a return of nuclear. China’s re-opening from its strict zero-Covid policies are estimated to add an additional 2% to global energy demands in 2023.

India

The United Nations projects that on April 14, 2023, India will surpass China as the world’s most populous country with an estimated 1.4 billion people. More importantly, however, is the fact that India’s population is also relatively young, so it will also have the world’s largest potential workforce. Recently, India has been marketing a Make In India campaign to global corporations like Apple, which recently announced that it would be moving a significant portion of its manufacturing to India. If India is to surpass China as the world’s key manufacturing hub, it will need to improve both the nutrition and education of its people. The Economist projects India will be an opportunity from now through 2050.

India is also related to the prior mentioned theme of energy security and the war in Ukraine. India has curtailed rice exports and it has been one of the primary destinations for Russia oil which has improved its relative energy costs.

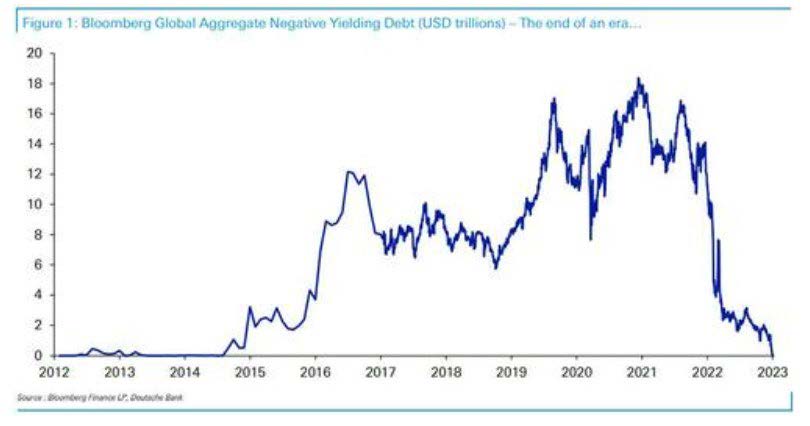

The End of the Quantitative Easing Era

Covid stimulus and the war in Ukraine have finally forced governments to exit the quantitative easing era. Japan was the first country to implement quantitative easing policies. As a result, Japan turned into the world’s largest creditor country over the last 30 years, as Japanese investors searched globally for higher interest rates and returns. The Bank of Japan recently began allowing interest rates to rise ever so slightly. If this trend continues, then global capital flows are in for a significant adjustment as Japanese investors repatriate money. At the margin, this adjustment away from quantitative easing has already collapsed the enormous $18 trillion dollar in negative interest rate debt bubble. The collapsing confidence in government debt markets might lead to increased demand for safe-haven instruments.

Circular Business Models

Government regulations and the push toward various 2030 initiatives seek to force businesses into “circular” v. “linear” business models. Circular business models seek to repair, reuse, and recycle all the materials of a supply chain, whereas “linear” models are characterized by larger waste streams. One of the industries that will be most impacted by the move toward “circular” business models will be the fashion and apparel markets. Given the relatively low cost of clothing, the cost of separating fibers becomes relatively expensive. As a result, the fashion industry will be making more “single” fiber clothing as this removes the need to separate fibers at the recycling point. In addition, most major fashion brands will be launching repair and reuse brands and services in 2023. The Economist estimates that circular business models will account for 23% of the global fashion industry by 2030, which translates into a $700 billion opportunity. We will be discussing this key trend with every millennial we know to find the next generation’s favorite brands.

Technology Trends

Key technology trends highlighted by The Economist include the expectation that the Federal Drug Administration will approve several psychedelic-related therapies for post-traumatic stress syndrome and alcoholism. Meanwhile, Apple will join Meta (the old Facebook) in the metaverse as it launches its first VR headsets. Meanwhile, technology supply chains will be closely watching Apple’s expansion in India and the geopolitical risk associated with Taiwan, given its importance to semiconductor manufacturing.

Portfolio Outlook and Actions

Historically, a split Congress is a stock market positive. In addition, higher interest rates are positive for future returns for fixed-income asset classes. If a mild recession does occur in the U.S., it is important to remember that equities typically bottom during the recession. Recessions also create opportunity in fixed-income credit markets.

In the equity markets, the options market at the beginning of the year had priced in a very range-bound outlook for 2023. As a result, we believe disciplined rebalancing will be a key to investor success this year. Given the key trends associated with emerging markets like India and today’s very real geopolitical risk, we also believe a well-diversified and global portfolio will be a key to long-term investor success.

Thank you for the trust you have placed in us, particularly during this difficult market environment. As always, if you have further questions, please do not hesitate to contact your FinTrust investment advisor.

Sincerely,

Your FinTrust Investment Team

Key Index Performance (As of 12/31/22)

| Index | QTD | YTD |

| S&P 500 (Large Capitalization Equity) | 7.56 | -18.11 |

| S&P 400 (Midcap Equity) | 10.78 | -13.06 |

| S&P 600 (Small Cap Equity | 9.19 | -16.10 |

| S&P 500 Growth Stocks | -1.45 | -29.41 |

| S&P 500 Value Stocks | 13.59 | -5.22 |

| S&P GSCI (Commodities) | 3.44 | 25.99 |

| S&P U.S. Aggregate Bond Index | 1.90 | -11.81 |

| Balanced Weighting (60/40) | 5.30 | -15.59 |

| S&P 500 Sectors | QTD | YTD |

| Energy | 22.81 | 65.72 |

| Utilities | 8.64 | 1.57 |

| Consumer Staples | 12.62 | -0.62 |

| Health Care | 12.80 | -1.95 |

| Industrials | 19.22 | -5.48 |

| Materials | 15.05 | -12.27 |

| Financials | 13.61 | -10.53 |

| Real Estate | 3.82 | -26.13 |

| Information Technology | 4.74 | -28.19 |

| Communication Services | -1.38 | -39.89 |

| Consumer Discretionary | -10.18 | -37.03 |

*Source: S&P Dow Jones Indices

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.