SUMMARY

- Back to Basics – Inflation, Bills, Bonds, and Stocks

- Silicon Valley Bank, Currency Risk, War, and Other Client Concerns

- The need for diversification

Portfolio Commentary

Written by Allen Gillespie, CFA®, Chief Investment Officer

Back to Basics – Stocks, Bonds, Bills, and Inflation

Inflation has been defined in the economics literature as a general rise in the price level caused by “too much money chasing too few goods.” While this is an accurate statement, it is also incomplete. The statement fails to define what constitutes “goods,” and it fails to examine inflation’s causal factors. The “goods” people care about when talking about inflation are things like gas, shelter, and food. In contrast, you will never hear people complain about the inflation of financial assets, namely stocks, bonds, and investment real estate, when they rise above reasonable values.

Today, people are concerned about inflation because it has finally shown up at the grocery store, in fuel prices, and in the cost of housing. U.S. consumer price inflation has been higher than 5% every month since June 2021. The reality, however, is that we have had an inflation problem for nearly two decades. Low interest rates following the internet bubble’s collapse in 2000-2003 led to inflation in the housing market.

The housing market bubble, in turn, popped in 2008 when Chinese and U.S. strategic petroleum reserve purchases drove oil prices to $150 a barrel and collapsed consumer incomes. Following the 2008 downturn, the global central banks again created a bubble, but this time in the global bond markets, as they sought to support depressed home prices and bank balance sheets through historically low interest rates and quantitative easing programs.

The era of low interest rates finally ended during the Covid recession, which was the worst recession since the Great Depression. Despite its severity, the massive government stimulus also made the Covid recession one of the quickest ever recorded. However, the covid shutdowns, supply chain disruptions, stimulus, war, and green energy policies have now combined to cause a “classic goods inflation.” This goods inflation popped the bond market bubble in 2022, and markets must now return to the basics.

Treasury Bills & Notes

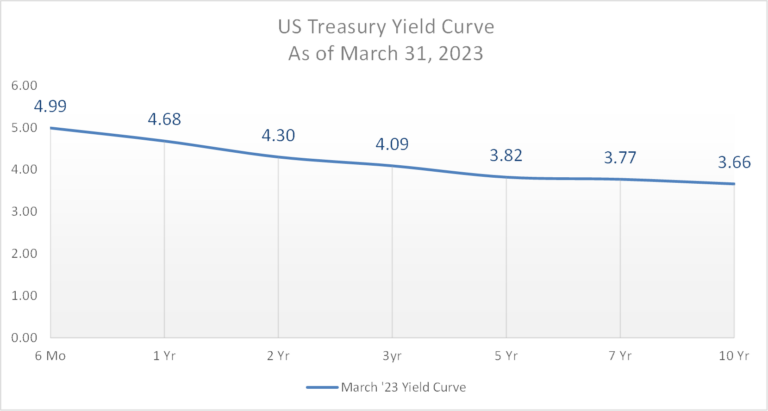

The U.S. treasury curve is currently inverted, meaning that short-term interest rates are higher than longer-term interest rates. Historically, this condition is associated with approaching recessions.

For example, 6-month T-bills hit 4.99% during March, while 10-year notes yielded 3.66%, indicating an expectation for lower interest rates in the future. While investors are excited to receive once again a yield on their cash and cash equivalent holdings, these rates are barely equal to or below the 5% reading for the consumer price index in March. Historically, T-bill yields and inflation roughly match each other, as there should be no long-term excess returns associated with holding the “riskless” asset.

For example, 6-month T-bills hit 4.99% during March, while 10-year notes yielded 3.66%, indicating an expectation for lower interest rates in the future. While investors are excited to receive once again a yield on their cash and cash equivalent holdings, these rates are barely equal to or below the 5% reading for the consumer price index in March. Historically, T-bill yields and inflation roughly match each other, as there should be no long-term excess returns associated with holding the “riskless” asset.

Corporate Bonds

At the end of March, Moody’s reported that BAA bonds (the low end of investment grade securities) yielded 5.71%. Therefore, corporate bonds now offer spreads above treasuries and potentially a slight return above inflation. However, the issue with corporate bonds is that they carry credit risk, so one must decide whether today’s spread is adequate compensation for both the inflation and credit risk associated with corporate bonds. Credit risks will tend to increase and manifest if the economy experiences a recession. Historically, corporate bonds have offered about 1.92% more than 10-year treasuries, which ended the month at 3.66%, so corporate spreads have returned to long-term historical averages.

Stocks

At the end of March, the earnings yield on the S&P 500 index of large company stocks registered 4.56%, according to Gurufocus.com, so the initial earnings yield is slightly less than both inflation and T-bills. Given the risks to earnings during a recession, many investors are questioning whether equities are still appropriate for their portfolios since they can make 5% on T-bills and CDs. The issue, of course, is that CD yields are only good for the term offered (i.e., 1 year) while earnings, even with a recession, have historically doubled every 7-10 years. As a result, we estimate equities are offering investors returns of 6.5-8.5% per year over a 7-10-year period.

Back to Basics – Time Horizon Is Key

All the math above leads to the following conclusions:

- Most asset markets today look fairly priced relative to inflation and risks for the first time in decades, but there is a real risk of recession.

- As detailed in early portfolio commentaries, equities historically bottomed out during recessions.

- While inflation and the initial yields for bills, bonds, and stocks look similar around the 5% level, the performance will be very different over different time horizons.

Back to Basics – Silicon Valley Bank, Currency Risk, War, and Other Client Concerns

Silicon Valley Bank

Silicon Valley Bank’s bankruptcy was a classic case of the mismanagement of interest rate risks, which is a risk faced by all banks. At the same time, interest rate risk can be managed. Now that CD rates are higher than treasury rates, we believe the situation will gradually improve across the banking sector. If there are additional problems in the banking system, we believe they will come from the credit risks associated with commercial real estate in major metro markets like New York, San Francisco, and Chicago. These markets have lost large numbers of both employers and employees to remote work and more tax-friendly states.

Currency Risk

Inflation is a form of currency risk. It is the risk your currency will lose purchasing power, but in the U.S., we rarely define inflation as a currency problem. However, the unique problem for U.S. investors is that the U.S. dollar has been the basis for global trade since World War II. As a result, we have printed many more dollars than we use domestically. In return for those dollars, we have received a lot of “stuff” from places like China without having to do the work. The good news/bad news about this situation is that these dollars might begin to return to the U.S., which will create higher inflation. The excess dollar demand, however, will also drive “work” as America will be forced to once again produce goods and services in return for these returning dollars – “reshoring” is the term the economics profession is using for this trend. This risk lies in the speed of the transitions because if all the dollars returned tomorrow, there would be 4x more dollars floating around than we need – so there would definitely be “too much money chasing too few goods.” By our calculations, even if it takes 30 years, the decline in the dollar as the reserve currency would result in 3% inflation for the next 30 years.

As a result, with inflation around 5% and interest rates around 5%, the Federal Reserve is unlikely to raise them higher, we believe international stocks, commodities, precious metals, and alternative currencies may have a role in diversified portfolios as a way to hedge both inflation and currency risks for some investors.

War, Politics & Other Client Concerns

The Need for Diversification

“Through chances various, through all vicissitudes, we make our way…” – Aeneid

War and politics create uncertainty and investor discomfort, but they also create opportunities for better or for worse. For example, in 2001, there was no homeland security industry, but today the Department of Homeland Security controls a $175 billion annual budget which is distributed through 17 sub-departments.

In our opinion, the key to investing with uncertainty is asking if what you believe is already reflected in the price, flexibility, diversification, and a willingness to adjust as new information is learned.

Portfolio Outlook and Actions

Historically, a split Congress is a stock market positive. In addition, higher interest rates are positive for future returns for fixed-income asset classes. If a mild recession does occur in the U.S., it is important to remember that equities typically bottom during a recession. Recessions also create opportunities in fixed-income credit markets. In addition, with currency and political concerns, other stores of value may have a place in investor portfolios.

At the beginning of the year, the options market for stocks had priced in a very range-bound outlook for 2023. As a result, we believe disciplined rebalancing is another key to investor success.

Thank you for the trust you have placed in us, particularly during this difficult market environment. As always, if you have further questions, please do not hesitate to contact your FinTrust investment advisor.

Sincerely,

Your FinTrust Investment Team

Key Index Performance (As of 3/31/23)

| Index | QTD | YTD | 12M |

|---|---|---|---|

| S&P 500 (Large Capitalization Equity) | 7.50 | 7.50 | -7.73 |

| S&P 400 (Midcap Equity) | 3.81 | 3.81 | -5.12 |

| S&P 600 (Small Cap Equity) | 2.57 | 2.57 | -8.82 |

| S&P 500 Growth Stocks | 9.63 | 9.63 | -15.33 |

| S&P 500 Value Stocks | 5.17 | 5.17 | -0.16 |

| S&P GSCI (Commodities) | -4.94 | -4.94 | -10.04 |

| S&P U.S. Aggregate Bond Index | 2.48 | 2.48 | -4.43 |

| Balanced Weighting (60/40) | 5.30 | 5.49 | -6.41 |

| S&P 500 Sectors | QTD | YTD | 12M |

|---|---|---|---|

| Energy | -4.37 | -4.37 | 13.15 |

| Utilities | -3.24 | -3.24 | -6.21 |

| Consumer Staples | 0.72 | 0.72 | 1.30 |

| Health Care | -4.31 | -4.31 | -3.70 |

| Industrials | 3.47 | 3.47 | 0.17 |

| Materials | 4.29 | 4.29 | -6.28 |

| Financials | -5.56 | -5.56 | -14.24 |

| Real Estate | 1.95 | 1.95 | -19.69 |

| Information Technology | 21.65 | 21.65 | -3.78 |

| Communication Services | 21.27 | 21.27 | -14.81 |

| Consumer Discretionary | -10.18 | -37.03 | -18.28 |

Source: S&P Dow Jones Indices

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.