What in the world is going on with the quantitative easing, government debt, banking and gold?

Everyone knows that the Federal Government has grown and that it has a debt of over $16 Trillion and that it is growing by just under $1 Trillion a year. Debt and deficits have to be financed by somebody, so fortunately for the U.S. Government, that somebody has been the banks.

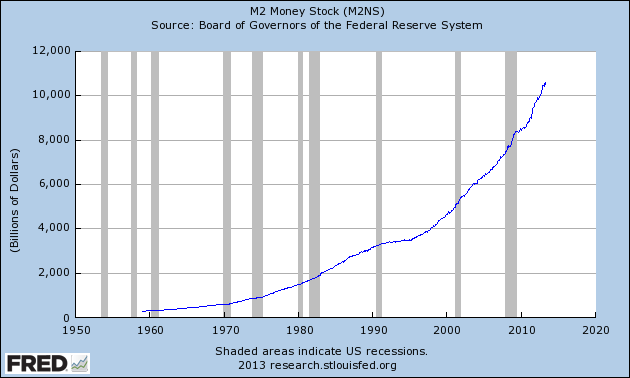

Banks are happy to buy these securities even at low interest rates because they can easily be flipped to the Federal Reserve because of its quantitative easing policy, whereby it buys $85 billion a month in securities to add to its $3.5 trillion in holdings.

The Federal Reserve purchases are intended to drive the amount of money to all-time highs.

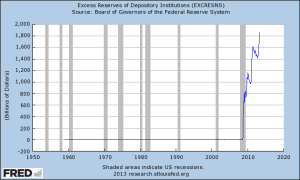

What are the banks doing with the cash they are receiving from the selling of assets to the Federal Reserve? Well, they are not loaning it because that would require risk and work in an entitlement society.

So, the cash is piling up at the Federal Reserve as Excess Reserves.

Why are banks just hoarding this money at the Federal Reserve? Well, because a lot of banks made bad loans, so people and businesses defaulted, impairing their own credit and bank balance sheets. As a result of that, many businesses today no longer are demanding credit due their near death experience during the recession.

And because this money is sitting, the velocity of money has crashed to 50 year lows.

And because every economics student is taught MV = PY where m = money and v = velocity, and p= price level and y = real GDP. If M is up, but V is down to a greater extend, well then p or inflation does this, as real growth is hard because someone actually has to produce something.

Gold has historically followed the direction of inflation, which one can see has been headed down since 2011, hence gold has crashed from $1950 to $1200 as the deflation meme gains traction.

Regional and community bank stocks, however, are now breaking out above their 2010 highs, as things are getting better as can be seen in the charts above.

As, or if, the Federal Reserve curtails its purchases of government securities then interest rates, as they have shown since May should rise. This is turn, should cause the trend in excess reserve accumulation by banks to reverse. If the trend of monetary hoarding reverses, then velocity is likely to turn up from its 50 year lows. Monetary velocity, unlike money itself, is a multiplier, consequently, the inflationary effects of a change in monetary velocity is more likely to lead to swift rather than gradual changes in inflation.

We think regional and community banks will be the beneficiaries of improved credit trends, higher interest rates, and merger and acquisition activity. We also think gold and gold mining stocks are reasonable hedges should the $3 trillion in excess reserves begin to acquire velocity, as we believe a transition from disinflation to high rates of inflation could be sudden.

Technical Risk to the Transition

The technical risk to the transition to higher interest rate levels can be seen in the last four cycles where interest rates rose significantly. The last interest rate cycle caused the real estate crash. The cycle before that caused the crash in the dot.com bubble. During the 1994 rise in interest rates, Orange County California imploded, but equities were a sideways affair, and the cycle before that was the 1987 stock market crash. Given the low level of interest rates and the unusual nature of the current environment, we believe there is both the opportunity for a mild 1994 transition and the risk of a 1987 transition, should interest rates follow the traditional pattern of two legs higher.

Inflation is a late cycle phenomenon, so where are we in the cycle. The National Bureau of Economic Research dates the peak of the last expansion at December 2007. The average peak to peak is 68.5 months, so cycle theorist will look for an economic peak this August/September when Congress debates the debt ceiling. The trough to peak measures of expansions average 58.4 and the last low was record in June 2009, which points to April 2014.

Velocity

Gold rallied from a 2009 low of $733 to a high of $1944 or 2.65x and that proved too much. Stocks began their bull market at a low of 666, so an equivalent move equals $1766.

Things are calm. The calmest of my career. It makes me think of the saying, “they don’t ring bells at the top.”

The signs are that the economy is picking up, but velocity may counter intuitively not be such a good thing in a world full of money.

Allen R. Gillespie, CFA is a partner with FinTrust Investment Advisors, in its Greenville, SC office. For more information, call 864-288-2849 or e-mail agillespie@fintrustadvisors.com.