Interview

Editor’s note: The Q & A below is an interview conducted by Fintrust Director of Marketing and Client Engagement Paige Siniard, with Allen Gillespie, CFA®, President, Managing Partner Investments.

February 2020

Q1 2020: Groundhog Day & Marvel Movies

Q: Allen, last quarter you said we were in a “Caddyshack Market.” Is that still the case?

Not anymore. As a result of the change in Federal Reserve Policy and the virus outbreak in China, markets have shifted. Let’s stay with our movie theme and say markets today are more like Groundhog Day and a Marvel superhero movie.

Q: Why Groundhog Day?

Due to the Federal Reserve’s 2018 interest rate increases and quantitative tightening (“QT”), sanity was returning to markets, but then this past fall the overnight lending rate market (“REPO”), which banks use to lend to each other, snapped and rates briefly shot up to over 10%. Retail investors barely noticed. Banking institutions, however, were suddenly very worried and unwilling to lend to each other overnight in a way that had not been seen since Lehman Brother’s bankruptcy. As a result, the Federal Reserve cut interest rates for a third time and relaunched Quantitative Easing (“QE”) to the tune of $80 billion a month.

Now, as we go into 2020 the markets feel like the movie Groundhog Day. Quantitative Easing (“QE”) was originally marketed by the Federal Reserve as a “crisis era” policy, but it has been more or less in continuous effect since the S&P 500 printed 666 in 2009. QE has become the crisis policy that never goes away.

Q: So, if QE was a crisis tool, then why did the Federal Reserve return to QE in the fourth quarter of 2019?

There are only a couple of logical reasons for this: either QE is now a permanent policy or we are still in a crisis.

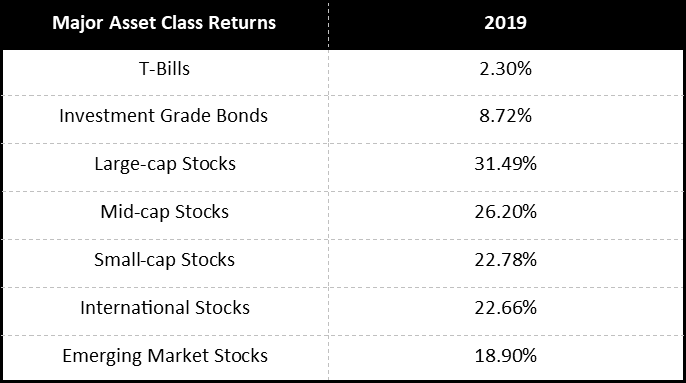

Source: Morningstar Direct, As of 12/31/2019

EXECUTIVE SUMMARY

FinTrust Investment Review Team:

Allen Gillespie, CFA®

Managing Partner Investments

Mercer Treadwell, CFA®

Senior Vice President, Investment Advisor

David Lewis, CFA®

Chief Financial Officer

Thomas Sheridan

Financial Analyst

Holland Church

Portfolio Administrator

- Monetary Policy: Accommodative. The Federal Reserve cut interest rates 3 times in 2019 and launched QE4.

- Fiscal Policy: Accommodative. The stock market begins to discount the economic impacts of elections and policy changes in first quarter of the election year.

- 2019-nCoV a Chinese 9/11? 9/11 was an event which significantly changed the U.S. economy and behavior and created new industries like homeland security, so its effects extended far beyond the immediate impacts. While many are focused on the current news, China’s reaction to the virus would appear to illustrate a significant change in thinking regarding biowarfare, healthcare, protection and international travel.

- Yield Curve Watch: It appeared more economically sensitive equities and inflation sensitive assets were attempting to trough until China went offline due to the 2019-nCoV outbreak. Economic inflection points can lead to increased market volatility, but markets now appear to be pricing in a second or more protracted economic dip.

Q: What are the effects of QE?

During QE periods, the central bank expands its balance sheet by purchasing bonds. This buying lowers interest rates, and increases the money supply on the books of banks. No banking institution wants the ‘hot potato’ of money that doesn’t yield anything, so they buy earning assets like stocks and bonds—in turn, stock market volatility has dropped, and returns are relatively high. Central bank QE policies force institutions with money to buy assets, regardless of valuations. This is all very mechanical, but it is not necessarily a great sign of financial health. For example, in 2019 the U.S. stock market was up over 30% as interest rates declined, but earnings were down year over year.

QE is a direct inflation of financial assets; it was originally designed to inflate mortgages for the benefit of banks. It all sounds great, but the problem is that below the surface there are large gaps between where private markets would trade and where government inflated markets do trade. This gap is the reason that an overnight lending market can suddenly panic and yield more than 10%.

Q: Earlier you said either “QE” is now a permanent policy, or we are still in crisis. Are we in a crisis?

Yes, I think we are in a hyperinflationary crisis. We haven’t experienced hyperinflation in the United States in over 200 years. The last U.S. hyperinflation was in the Continental Dollar after the Revolutionary War—this is where we got the phrase “not worth a Continental.” This is also why we have Article I, Section 10 of the Constitution which restricts a state’s ability to coin money.

Q: If we are in a hyperinflationary crisis, what should an investor do?

Hyperinflationary markets follow a different crisis pattern. In a typical crisis, financial assets like stocks and bonds trade down in price, but during hyperinflations they trade up in nominal prices. Then, typically, there is an abrupt adjustment period. After the adjustment there is a quick recovery as currency values change. This is all due to the fluctuations of the currencies, not the real values of companies. Extreme examples of this would be present-day Venezuela or Germany in the early 1920s.

During hyperinflations, equities prices rise because they directly reflect the change in the value of money. Bond prices are also stable, but there are huge losses to purchasing power. Hyperinflations can also come with terrible underlying business and social dynamics because hyperinflation really alters behavior and political mood. For example, the Venezuelan stock market, in nominal terms, has been among the best performing stock markets in the world, but you can’t buy toilet paper.

I think it is really important to note that hyperinflations usually end when the currency is replaced. In Venezuela, they are now using US Dollars, and you can now see the early signs of recovery. In Germany, they replaced the original Mark with the RentenMark and the hyperinflation stopped. I think it is telling that in the United States, Japan, and Europe, we are currently seeing gold, cryptocurrencies, and equities rapidly appreciating under QE.

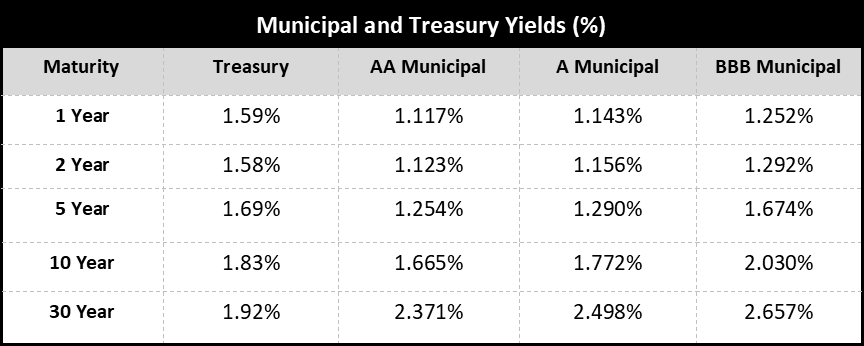

Source: Bloomberg as of 12/31/19

Q: Why is the Federal Reserve hyperinflating the money supply?

Initially, it was because during the 2008 financial crisis, major companies like General Electric and Goldman Sachs had to pay Warren Buffett 15% to borrow money. The Federal Reserve adopted QE to ease financing pressures. Now, what large entity cannot afford higher interest rates at today’s historically low levels? The answer is simple: global governments. Global governments are completely broke—we have reached a point that can only be captured in ‘Marvel’ terms. The Groundhog’s Day market (QE on repeat) has laid the groundwork for something that can only compare in size, scale, and seriousness to the Marvel Movies: Avengers Infinity Wars and End Game.

Q: Can you expand on your analogy?

Yes, we are pretty deep in metaphor now, but stay with me. These Marvel movies are big budget films which bring together an interesting mix of technologically advanced, futuristic, transhuman, and supernatural characters like Iron Man, Dr. Strange, The Hulk, Thor, Black Panther, and others to fight villains powerful enough to destroy the universe or eliminate half the population. Another characteristics of Marvel movies are the huge fight scenes, where cities are ripped apart as these otherworldly characters battle. When the Hulk gets thrown into a New York skyscraper, well, the skyscraper does not fare well. These movies can also feel a little chaotic when one doesn’t know all the characters and their backstories.

Q: How does this relate to financial markets?

Just consider this. Global interest rates are currently well below the levels that persisted during World War I and World War II. Why?

Well, at the highest level, we were initially fighting the first downturn in real estate prices since the Great Depression. This was a big battle. Now, the Trump administration is waging a huge economic and strategic military war against China. The administration is simultaneously waging cultural war against globalist views both in the US and in Europe. Trump has been very direct in his comments regarding interest rates and the economic war.

Globally, according to Bloomberg there are over $15 trillion in negative interest rate bonds, and Trump is saying the U.S. has the best credit in the world, so we should have the lowest rates. If central banks make U.S. rates negative, the amount of negative interest rate bonds and savings will balloon to over $50 trillion globally.

As a financial analyst, my largest concern is trying to help people understand the enormity of what we are witnessing in the global bond market. I am fully convinced that given the size and scale of what we are seeing, investors need to make generational changes in their approach to investing. I, however, sense a lot of inertia. It is hard to believe what is happening because it has never happened before.

Q: Can you expand on that last comment?

Well, the collapse of the bond market is forcing funds into equities independent of valuations. This is completely understandable, but there is a lot of risk if this is the wrong maneuver. Based on our research, on December 31, 2019 equities were 35% above their 25-year average valuation, but if $50 trillion is to yield nothing, then these valuations make complete sense because anything is better than nothing.

In part, today’s high equity valuations are justified by lower rates. And to an extent the high valuations are justified because we have allowed the huge otherworldly technology companies to grow into monopolies of Marvel proportions. The Wall Street Journal just reported the top 5 technology companies have acquired over 500 businesses in the last 10 years. There is only one Hulk, one Thor, etc..

I think everyone can easily see the impact and market power that technologically advanced companies like Amazon, Apple, Google, Facebook, Netflix, Twitter, and Microsoft are having in the markets and in the culture. The Iron Men companies are all around us.

Social media companies especially are creating a large battleground because of the use and collection of private, personal data, and their influence in media and politics.

For me, however, I think the issues regarding the control of private, personal data will reach a peak as our smart devices and our biology are integrated. Our trans-human future if you will. For decades, medicine has been helping us by placing increasingly sophisticated devices and medicines into our bodies. I can still remember when the first medicated heart stent came into existence. Now, we have “smart devices” that can be integrated into our biology. This is great, but it does raise issues associated with device hacking, security, and control. This will create lots of large battles and changes.

Q: Any thoughts on the nCoV-19 virus in China?

Again, think Marvel Movie in terms of scale and impact. It strikes me that it could be the equivalent of a Chinese 9/11 type event or Japanese Fukushima. After these events, thinking and ways of life change. The concept of Homeland Security as an industry or federal agency did not exist at the time. Now, Homeland Security is among the largest federal agencies. We now have to pass through security screens at airports—I think the virus and what we are learning about its incubation period will extend these checks to include our biology. It will no longer be enough to screen just our physical person, as it is easy enough to contemplate a bio-carrier as more dangerous than a drug mule or terrorist.

The Chinese have quarantined over 50 million people. I doubt anyone, anywhere in the world is going to forget that. They have also used technology to track people and to help enforce the quarantine. The battle for freedom and control in an age of bio-crisis will have an enormous impact on our world.

QUICK TAKE: MAJOR ASSET CLASSES

It’s All About Historically Low Interest Rates

Global interest rates are at historic lows. We believe this reality leaves investors with four basic alternatives:

- Do I put more money into equities?

- How do I control cost for Core Asset Allocations?

- Are there tactical fixed income and equity strategies which offer different risk/reward trade-offs?

- Do I diversify into other markets?

Cash and Cash Equivalents

President Trump continues pushing the Federal Reserve to lower rates to zero to match Europe and Japan. If Trump’s argument wins, then we believe it would cause a blow-off (huge upside) move in equities, gold, and cryptocurrency, as it would force money out of bonds and cash.

Investment Grade Fixed Income

The bond market had started to regain its shape until the virus outbreak in China. As a result, the bond market is starting to point toward a second dip in conditions. Interest rates continue to be very low by historical standards. As a result, we think investment grade bonds still have a defensive roll to play, but do not offer much in the long run.

Tactical Fixed Income

Historically, fixed income and equity arbitrage strategies earn a risk premium above cash yields. Over the last few years, when cash rates were very low, these strategies were not as attractive as some more traditional credit and interest rate carry strategies. Now, however, given the low level of long-term interest rates and the associated interest rate risk, we believe event, fixed income, and equity arbitrage related strategies offer a compelling risk return opportunity. We believe the return profile is reasonable, and the risk profile is better than traditional fixed income.

Core Equities

Last December, the Dow Theory gave a sell signal. After the third Federal Reserve interest rate cut in October, Dow Theory moved into a confirmed uptrend. We are modestly constructive on equities, but we would not overweight equities beyond investor risk determined allocations given that equities currently trade at a significant premium to historical valuations.

Tactical Equities

Due to the extreme conditions in core fixed income and equity markets, we think that tactical equity strategies may offer investors the best risk/reward trade-offs. Tactical equity strategies, like long/short equity, option based strategies and market neutral strategies have historically weathered bad bond markets and buffered bad equity market storms. We believe tactical equity strategies are becoming increasingly attractive on a relative value basis given low interest rates and historically high equity valuations.

Other Markets

Other markets like gold, cryptocurrency, and real estate do offer diversification benefits to traditional portfolios, but some suffer from the same valuation issues as stocks and bonds. In addition, outside markets have their own risks, rewards, and implementation issues, but they may have a role depending on investor specific considerations.

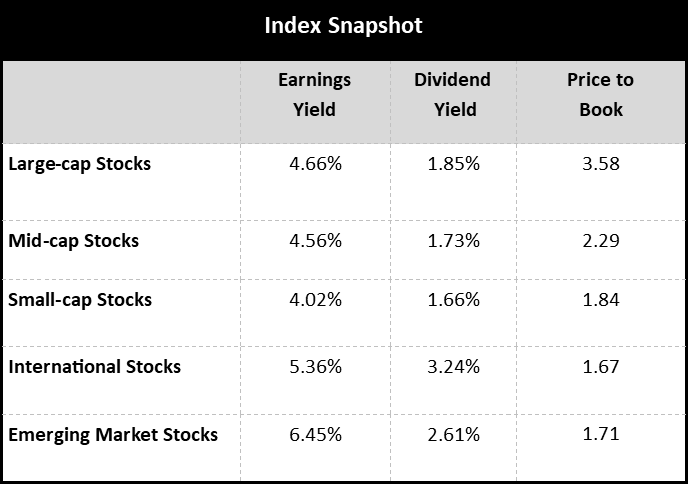

Source: Bloomberg as of 12/31/19

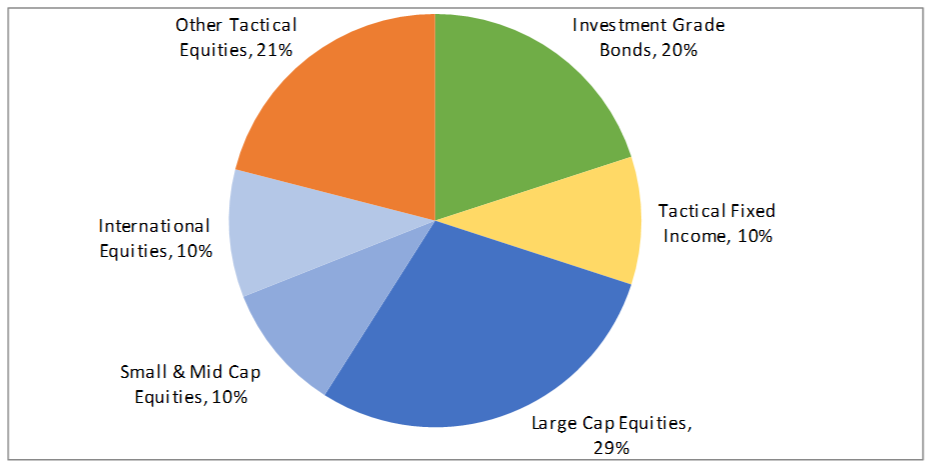

FinTrust Allocations (70/30 Risk Profile) with Tactical

Positioning as of 12/31/2019. This model displays FinTrust’s Funds & ETF Model with Tactical target portfolio guidelines. Each client situation is unique and may be subject to special circumstances, including but not limit to greater or less risk tolerance, classes, concentrations of assets not managed by FinTrust, investment limitations imposed under applicable governing documents, and other limitations that may require adjustments to the suggested allocations. Model asset allocation guidelines may be adjusted from time to time on the basis of the foregoing and other factors.

About FinTrust Capital Advisors, LLC

Privately owned and independent, FinTrust Capital Advisors is a Southeastern based financial services firm that serves both personal wealth clients and corporate and institutional clients. Fintrust offers strategic financial planning, investment management, fiduciary and retirement plan consulting, research, capital markets, and other services concerning financial well-being. The FinTrust team of experienced professionals provides solutions to meet both individual and corporate client objectives.

Important Disclaimer

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument, unless explicitly stated as such. Past performance is not necessarily indicative of future returns. This information should not be construed as legal, regulatory, tax, or accounting advice. This material is provided for your general information. It does not take into account particular investment objectives, financial situations, or needs of individual clients. This material has been prepared based on information that FinTrust Capital Advisors believes to be reliable, but FinTrust makes no representation or warranty with respect to the accuracy or completeness of such information. Investors should carefully consider the investment objectives, risks, charges, and expenses for each fund or portfolio before investing. Views expressed are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indexes in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

Fintrust Brokerage Services | www.Fintrustadvisors.com | 124 Verdae Blvd, Ste. #504, Greenville, SC 29607 | 864-288-2849 | Equity Research