CORONAVIRUS, RISK MANAGEMENT, THE BUSINESS CYCLE AND ASSET ALLOCATION

February 24, 2020

WITH WORLD EQUITY MARKETS OFF STRONGLY TODAY, THE INVESTMENT TEAM HAS RECEIVED A LARGE NUMBER OF QUESTIONS THIS MORNING. SO, HERE IS THE DATA DUMP.

CORONAVIRUS HEADLINES

As previously mentioned, world governments are reacting strongly to the outbreak. Based on the statistics we have seen, there are many other diseases and causes of death that are more likely, but the reactions and drug treatments being employed suggest suspicions that the virus may not be completely natural.

ALLEN, YOU HAVE SAID AROUND THE OFFICE THAT THE CORONAVIRUS IS LIKE A CHINESE 9/11. CAN YOU ELABORATE ON THAT COMMENT?

I used to cover the defense sector, so I remember how homeland security, as an industry, was created after 9/11. We experience this change every time we go through an airport security screener. Based on the fact that nearly 100 million people have been quarantined around in the globe, I think there is going to be a permanent change in thinking. Now, I suspect, our airport and port screens will include our biology in order to test for fever and virus incubation periods. Our phone GPS data will be used to map outbreaks our travel patterns past the point of entry. In short, the surveillance state is coming out of the shadows. China has already used its facial recognition systems to stop people breaking quarantine.

WILL THE VIRUS TIP THE WORLD INTO RECESSION AS SUPPLY CHAINS ARE DISRUPTED?

Since May of 2019, the bond market has been pricing in a recession to begin in the first quarter of 2020. Obviously, the virus will be cited as the cause, but markets have been in the process of discounting a recession since late 2018 when the yield curves first inverted. Longer-term, however, I do think it will force companies to examine and re-think their supply chains.

HOW DO BONDS AND EQUITIES PERFORM AROUND RECESSIONS?

Historically, markets discount future events, so the typical pattern would be for equities to top just prior to a recession and bottom during the recession, once investors can see an upturn in the earnings picture. Meanwhile, the yield curve typically inverts prior to a recession then regains its slope during a recession. In short, the typical pattern generally suggests that during a recession one should find relatively high bond prices and relatively low equity prices until one can see the finish line. Since World War II, most recessions have lasted 16-21 months.

WHAT ARE MARKETS REFLECTING NOW?

Clearly, bond prices are high because interest rates have never been this low, but the yield curve has inverted for a second time, so we can’t see the finish line yet. Equities have been sending a mixed picture. International, small and midcap stock indices reached their highs in January 2018 and bottomed at the end of 2018, but they have yet to make new highs. Meanwhile, the large cap stocks of the S&P 500 have continued to rally to new highs as bond yields have declined. We think this is because people still need income, so they have been buying large capitalization stocks with dividends and buybacks as

bond substitutes.

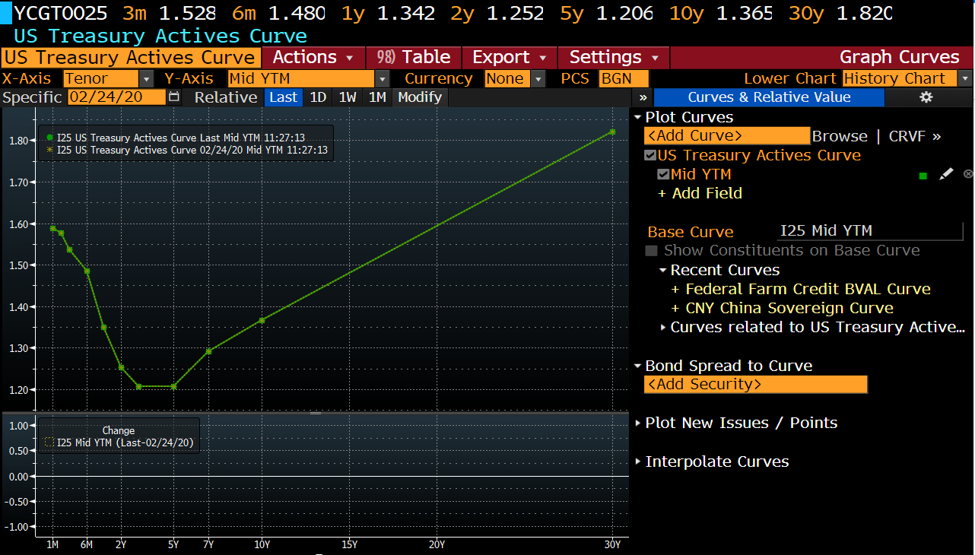

Source: Bloomberg

In the chart of the yield curve above, one can see the steep drop-in interest rates from now until about the 2-year horizon, then an inflection where rates head back up.

IF MARKETS ARE REFLECTING A RECESSION, SHOULD INVESTORS CHANGE THEIR ALLOCATIONS?

I always remind people, knowing your time horizon is probably the most important factor in investing. Most investors are better off riding through the business cycle than trying to time it, however, I never think it is a bad idea to revisit risk assumptions and risk tolerance levels.

For example, when we do long-term planning for a client, a typical volatility assumption for equities might be 20%. Well, this morning equity volatility is 23 as measured by the VIX index, which is a little higher than the modelled assumption. What this means for an investor is that his portfolio is behaving like he has more equity volatility than he originally thought.

Now, the higher volatility may be a short-term thing, or it could reflect that equity markets are experiencing more uncertainty. Obviously, one cannot change what the market is doing, but one can change one’s exposure to it. For example, if one cuts their equity exposure by 5-10% they would be back in-line with their planning model’s assumption. I believe gradual and thoughtful changes are likely to serve an investor better than emotional and reactive changes. Our emotions tend to be binary in behavior, we are either greedy or afraid, happy or sad, but investors should think more in terms of probabilities which are rarely 0 or 100%.

IMPORTANT DISCLOSURES:

Securities offered through FinTrust Brokerage Services, LLC (Member FINRA/ SIPC) and Investment Advisory Services offered through FinTrust Capital Advisors, LLC. Insurance services offered through FinTrust Capital Benefit Group, LLC. This material does not constitute an offer to sell, solicitation of an offer to buy, recommendation to buy or representation as the suitability or appropriateness of any security, financial product or instrument.

This report is prepared for general circulation. This report is not produced based on any individual persons or entities investment objectives or financial situation and opinions expressed by the analyst are subject to change without notice. This report is not provided to any particular individual with a view toward their individual circumstances. Investors should consider this report as only a single factor in making an investment decision. Securities prices fluctuate and investors may receive back less than originally invested and are not guaranteed. Investing involves risk including loss of principal.

Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

*FinTrust Capital Advisors, LLC and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.